APY vs NPS: Which Pension Scheme Is Right for You in 2026?

India has a retirement savings problem. Most Indians — especially those in the informal sector — reach their 60s without any structured pension income. The government tackled this through two flagship schemes under the Pension Fund Regulatory and Development Authority (PFRDA): the Atal Pension Yojana (APY) and the National Pension System (NPS). Both are legitimate, government-backed retirement tools. But they are built for very different people, and choosing the wrong one could mean leaving lakhs of rupees on the table.

This guide explains exactly how each scheme works, compares them side by side with real numbers, and helps you decide — clearly and confidently — which one belongs in your retirement plan in 2026.

What Is APY (Atal Pension Yojana)?

The Atal Pension Yojana was launched in 2015, primarily to bring India's vast informal workforce into the pension net — domestic workers, street vendors, small farmers, construction labourers, and anyone else who does not have access to an employer-sponsored provident fund.

APY is a defined benefit pension scheme, which means you know exactly what you will receive at retirement before you invest a single rupee. When you join, you choose a pension slab — ₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000 per month — and your contributions are set accordingly. When you turn 60, the government guarantees that monthly pension for the rest of your life. After your death, the same pension goes to your spouse. After the spouse's death, the total corpus is returned to your nominee. Use our APY Calculator to find out your exact monthly contribution for your chosen pension slab and joining age.

Key eligibility rules for APY:

- Age: 18 to 40 years at the time of joining

- Must hold a savings bank account (any bank)

- Must be an Indian citizen

- From October 2022: Must not be an income tax payer. If you file an ITR with taxable income, you are barred from enrolling. Existing accounts opened before this date can continue.

That last point is critical. It means APY is now exclusively for people earning below the basic exemption limit — effectively the informal and semi-formal economy.

What Is NPS (National Pension System)?

The National Pension System is a market-linked, defined contribution scheme regulated by the PFRDA. It was originally designed for central government employees (2004) and later opened to all Indian citizens in 2009. NPS gives you no guarantee on the pension amount — instead, your contributions are invested across equity, corporate bonds, government securities, and alternative assets. Your final corpus depends on your investment choices and market performance over time.

NPS operates through two account types. Tier 1 is the primary pension account — contributions are locked in until age 60, with limited partial withdrawals allowed for specific purposes. This is where all the tax benefits are available. Tier 2 is a voluntary savings account with no lock-in — you can withdraw money anytime, but there are no tax benefits (except for central government employees). Read our detailed guide on NPS Tier 1 vs Tier 2 to understand when and how to use each account.

At the age of 60, you can withdraw up to 60% of your NPS corpus as a lump sum — this withdrawal is fully tax-free. The remaining 40% must be used to purchase an annuity from a PFRDA-empanelled insurance company, which generates your monthly pension for life. Use our NPS Calculator to model exactly how much corpus you can build based on your current age, monthly contribution, and expected return rate.

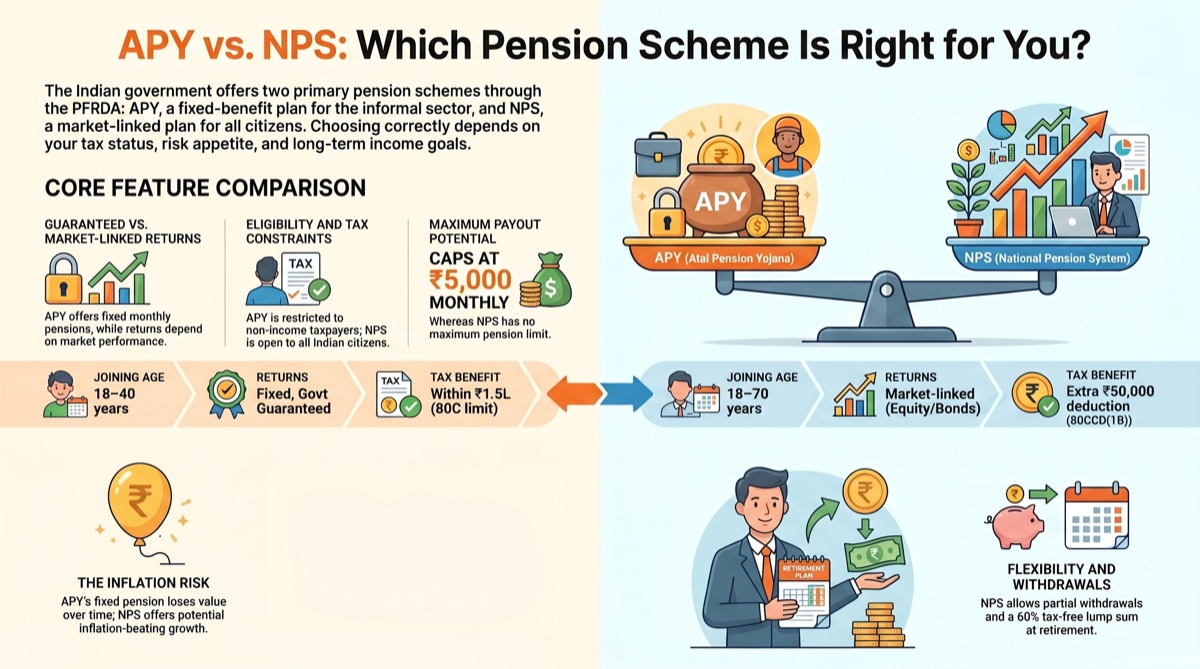

APY vs NPS: Full Feature Comparison

| Feature | APY | NPS |

|---|---|---|

| Who can join | 18–40 years, non-income-taxpayer | 18–70 years, any Indian citizen |

| Return type | Fixed, government-guaranteed | Market-linked (variable) |

| Pension amount | ₹1,000–₹5,000/month (chosen at joining) | Depends on corpus + annuity rate |

| Maximum possible pension | ₹5,000/month (₹60,000/year) | No cap — depends on investment |

| Minimum contribution | ₹42–₹1,454/month | ₹500/month (Tier 1) |

| Lock-in | Until age 60 | Until age 60 (partial withdrawals allowed) |

| Tax benefit | 80CCD(1) — within ₹1.5L 80C limit | 80CCD(1) + extra ₹50,000 under 80CCD(1B) |

| On death before 60 | Nominee receives return of corpus | Full corpus transferred to nominee |

| Inflation protection | None — fixed pension in nominal terms | Partial — depends on equity allocation |

| Premature exit | After 3 years, only on exceptional grounds | Allowed, with partial annuity requirement |

APY Contribution Table: What You Pay vs What You Get

The beauty of APY is its simplicity. Here is exactly how much you need to contribute monthly to receive ₹5,000 per month at age 60, depending on when you join:

| Joining Age | Monthly Contribution | Total Contributed | Monthly Pension | Break-Even Period |

|---|---|---|---|---|

| 18 | ₹210 | ₹1,00,800 | ₹5,000/month | ~20 months |

| 25 | ₹376 | ₹1,35,360 | ₹5,000/month | ~27 months |

| 30 | ₹577 | ₹1,38,480 | ₹5,000/month | ~28 months |

| 35 | ₹902 | ₹1,35,300 | ₹5,000/month | ~27 months |

| 40 | ₹1,454 | ₹1,04,688 | ₹5,000/month | ~21 months |

The break-even column is what makes APY genuinely appealing for eligible individuals. If you live even two years past 60, you have recovered your entire investment. Every year after that is pure gain — for both you and your spouse. Calculate your own APY contribution using the APY Calculator — enter your age and target pension to see the exact monthly debit amount.

NPS: How Much Corpus Can You Build?

NPS operates very differently — there is no fixed pension at the end. Instead, you build a corpus over decades and convert a portion of it into a monthly annuity. Here is a realistic projection for someone aged 30 who contributes ₹5,000 per month into NPS Tier 1 with a balanced allocation (50% equity, 30% corporate bonds, 20% government securities):

| Assumed Return | Corpus at 60 | Lump Sum (60%) | Annuity Corpus (40%) | Monthly Pension (6% annuity) |

|---|---|---|---|---|

| 10% CAGR | ₹1.13 crore | ₹67.5 lakh | ₹45 lakh | ₹22,500 |

| 12% CAGR | ₹1.76 crore | ₹1.06 crore | ₹70 lakh | ₹35,000 |

| 14% CAGR | ₹2.76 crore | ₹1.65 crore | ₹1.10 crore | ₹55,000 |

Even at a conservative 10% CAGR, NPS generates a monthly pension of ₹22,500 from ₹5,000/month contributions starting at age 30 — that is 4.5 times what APY's maximum ₹5,000/month pension offers. The catch, of course, is that these returns are not guaranteed. This is the fundamental risk-reward tradeoff between the two schemes. Run your own numbers with the NPS Calculator — adjust your contribution, start age, and return rate to see how your retirement corpus changes. For a side-by-side comparison of all three major government schemes, use the PPF vs EPF vs NPS Calculator.

Tax Benefits: Where NPS Has a Clear Edge

Tax efficiency is one of the most important — and most misunderstood — dimensions of this comparison.

APY tax benefits are available under Section 80CCD(1), but they fall within the overall ₹1.5 lakh ceiling of Section 80C. If you are already maxing out your PPF, ELSS, or LIC premium, your APY contribution gets no additional tax benefit. Furthermore, since APY is now restricted to non-income taxpayers, most subscribers will not benefit much from deductions anyway.

NPS tax benefits are considerably more generous for formal sector workers:

- Section 80CCD(1): Up to 10% of your salary (basic + DA) can be deducted, within the overall ₹1.5 lakh 80C limit.

- Section 80CCD(1B): An additional ₹50,000 over and above the 80C limit can be deducted exclusively for NPS contributions. No other investment instrument offers this exclusive extra deduction.

- Section 80CCD(2): If your employer contributes to your NPS (up to 14% of salary for central government employees, 10% for others), that entire employer contribution is deductible with no upper limit.

For someone in the 30% tax bracket contributing ₹50,000 to NPS under 80CCD(1B), the tax saving is ₹15,600 (including cess) every financial year. Over a 25-year career, this deduction alone, if reinvested, compounds into a substantial sum. Use our Income Tax Calculator to see exactly how much tax you save when you add NPS contributions, and compare the old vs new regime impact with our New vs Old Regime Calculator. Our Section 80C Calculator helps you optimise the full ₹1.5 lakh deduction bucket before adding the NPS 80CCD(1B) top-up.

The Inflation Problem With APY

APY promises you ₹5,000 per month when you turn 60. That sounds reassuring. But at India's average inflation rate of around 5–6% per year, ₹5,000 in 2026 will have the purchasing power of roughly ₹1,500 to ₹1,800 in 25 years. The pension amount never increases — you will receive the same ₹5,000 in 2051 as on day one, even though everything around you costs three times more.

NPS does not directly protect against inflation either, but its market-linked nature means that if equity markets grow faster than inflation over the long run — which they historically have — your corpus and eventual pension have a chance of keeping pace with rising prices. For serious long-term retirement planning, this inflation gap is a compelling reason why NPS is a better primary vehicle for most working Indians.

Who Should Choose APY?

Informal sector workers who earn below the income tax threshold. Domestic workers, small farmers, daily wage labourers, and small traders who want a guaranteed, fuss-free pension benefit enormously from APY. The contribution is small, the guarantee is real, and the complexity is zero.

Young people starting their first informal income. Joining APY at 18 with a ₹210 monthly contribution for ₹5,000/month pension is one of the most efficient guaranteed-return deals available anywhere in Indian finance. The implied internal rate of return, when you consider the lifetime pension plus spousal pension, is exceptional.

People who want a guaranteed pension floor alongside other investments. Even for someone with NPS or mutual funds, APY can serve as a guaranteed minimum income layer — if they are eligible.

Who Should Choose NPS?

Salaried employees in the formal sector. The employer matching under 80CCD(2), combined with the exclusive 80CCD(1B) deduction of ₹50,000, makes NPS extraordinarily tax-efficient. No other instrument offers this combination.

Self-employed professionals and business owners. NPS Tier 1 is open to self-employed individuals who can claim the full 80CCD(1B) deduction — a ₹50,000 reduction in taxable income with no equivalent elsewhere.

Anyone who cannot join APY. If you file income tax returns, APY is off the table. NPS is your primary regulated pension option.

Long-term wealth builders who can tolerate some market risk. The potential upside from NPS — where a ₹5,000/month contribution might build ₹1.5–₹2 crore over 30 years — is simply not available through the guaranteed APY structure.

Can You Hold Both APY and NPS?

Yes — if you are eligible for both (i.e., a non-income taxpayer), you can hold both simultaneously. The combination can actually make sense: APY provides your guaranteed pension floor, while NPS provides market-linked growth on top of it.

For most people reading this article, however, income tax eligibility has already ruled out APY. In that case, the decision is already made: NPS is your government-regulated pension vehicle.

A Practical Decision Framework

1. Do I pay income tax?

If yes — APY is not available to you. Choose NPS.

If no — Both are available. Consider APY for the guaranteed floor, NPS or PPF for growth.

2. What is my risk tolerance?

If you cannot sleep at night during a market downturn — APY (if eligible) gives you certainty. NPS still makes sense, but opt for a conservative allocation.

If you are comfortable with long-term market fluctuations — NPS with a higher equity allocation will likely produce significantly better outcomes.

3. How far am I from retirement?

If you are 30+ years away — NPS equity funds have historically smoothed out volatility over long periods. The power of compounding over 30 years makes market-linked returns transformative.

If you are 10–15 years away — A more conservative NPS allocation or a combination with PPF or SCSS makes sense. Use our Retirement Corpus Calculator to work out exactly how much you need to save to fund your desired retirement lifestyle, and our Early Retirement Calculator if you are aiming to retire before 60.

Frequently Asked Questions

Is APY better than NPS for someone earning ₹3 lakh per year?

If your annual income is below the basic exemption limit, you are not an income taxpayer and are eligible for APY. In this case, APY is an excellent option because it offers a lifetime guaranteed pension with very small contributions. You could additionally open a PPF account for long-term savings with no market risk. NPS is also available, but the tax benefits are less relevant at lower income levels.

What happens to my NPS corpus if I die before age 60?

If an NPS subscriber passes away before the age of 60, the entire accumulated corpus is paid out to the nominee. There is no requirement to purchase an annuity in this situation. The nominee receives the full corpus as a lump sum, which is a meaningful financial safety net for the family.

Can I withdraw money from NPS before retirement?

Yes, partial withdrawals from NPS Tier 1 are permitted after completing three years of subscription, for specific purposes including higher education of children, treatment of critical illness, home purchase or construction, and starting a business. The maximum withdrawal is 25% of your own contributions (excluding employer contributions). You can make up to three partial withdrawals throughout your working life.

Is the 60% NPS lump sum withdrawal really tax-free?

Yes. Under current tax rules, the lump sum withdrawal of up to 60% of your NPS corpus at retirement is fully exempt from income tax. Only the annuity income (the monthly pension) is taxable as per your applicable income tax slab in the year of receipt. This makes NPS one of the most tax-efficient long-term wealth-building instruments available to Indian investors.

What is the best NPS fund allocation for someone aged 35?

At 35, with approximately 25 years until retirement, most financial planners recommend an equity allocation of 50–75% through the Active Choice option in NPS. The NPS equity fund (Class E) invests in a diversified portfolio of large-cap stocks and has historically delivered 12–15% CAGR over rolling 10-year periods. As you approach 55, gradually shifting toward bonds and government securities reduces volatility in the final years before retirement.

How is the APY contribution auto-deducted?

APY contributions are automatically debited from your linked savings bank account on the first of every month (or the date you specify). You need to maintain a sufficient balance to avoid defaults. If the account has insufficient funds, a penalty is charged — ₹1 per month for every ₹100 of due contribution. Continued defaults for 24 months result in account closure.

Disclaimer: The information in this article is for educational and general awareness purposes only and does not constitute financial advice. APY and NPS rules, contribution amounts, and tax provisions are subject to change by PFRDA, RBI, and the Government of India. All figures are based on publicly available data as of May 2026. Please consult a SEBI-registered investment advisor or a Certified Financial Planner (CFP) for personalised retirement planning guidance tailored to your income, goals, and risk profile.