Old vs New Tax Regime FY 2026-27: Which One Actually Saves You More?

Every April, millions of salaried Indians face the same question at their HR portal: old regime or new regime? Picking the wrong one can cost anywhere from ₹10,000 to over ₹1.5 lakh in extra tax. The good news is that the math is not complicated once you know what to look for.

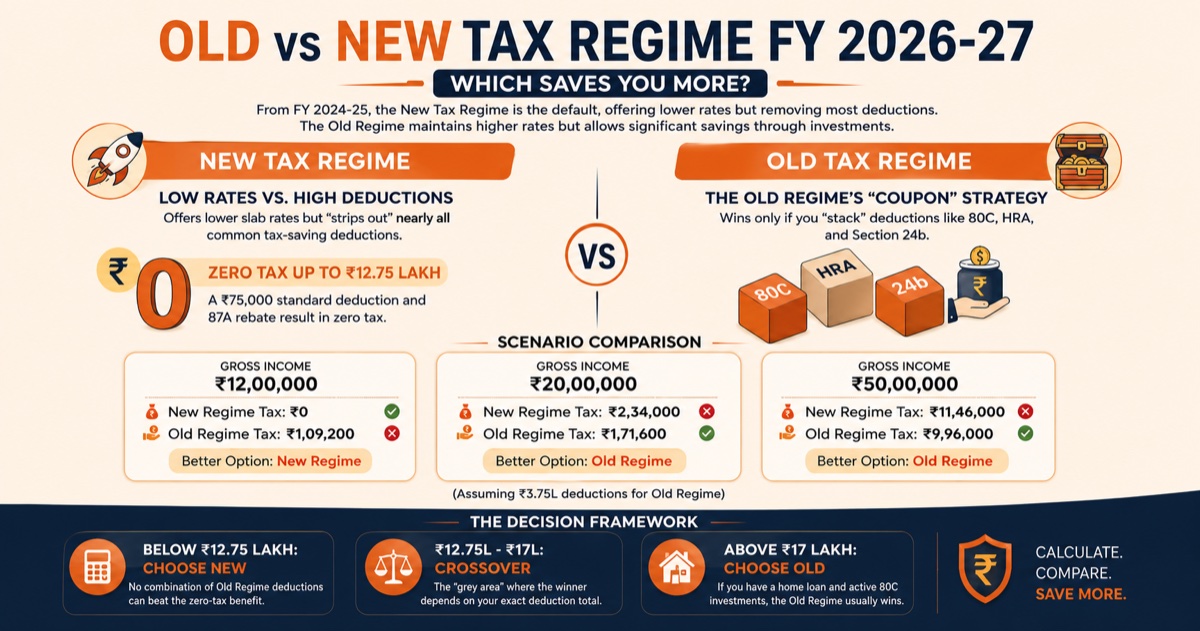

From FY 2024-25, the new tax regime became the default in India. If you do nothing, your employer deducts TDS under the new regime. Doing nothing is not always the right call. For a large number of salaried Indians — especially those with home loans, HRA, and active 80C investments — the old regime still comes out ahead.

What Is the Core Difference Between the Two Regimes?

Think of it this way. The new tax regime is like a flat-rate restaurant that charges you less per dish but won't apply any coupons. The old tax regime charges more per dish but lets you stack as many discounts as you have. Which works out cheaper depends entirely on how many deductions you have.

The new regime offers lower slab rates and a generous Section 87A rebate that takes your tax liability to zero if your income is ₹12 lakh or below. However, it strips out nearly all deductions — no Section 80C, no HRA exemption, no home loan interest under Section 24b, and no Section 80D. The old regime keeps all of these alive but taxes you at higher rates before those deductions are applied.

New Tax Regime Slabs for FY 2026-27 (AY 2027-28)

The new regime received a significant upgrade in Budget 2025. The nil-tax threshold was raised to ₹4 lakh, and the 87A rebate was extended to cover income up to ₹12 lakh.

| Income Slab | Tax Rate |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Zero tax for incomes up to ₹12 lakh: Under Section 87A, the new regime provides a rebate that cancels out all tax if your total income does not exceed ₹12,00,000. For salaried individuals, the standard deduction of ₹75,000 under the new regime means zero tax liability effectively extends to gross salary up to ₹12,75,000.

Old Tax Regime Slabs for FY 2026-27

The old regime has remained unchanged for several years. Its slab rates are higher, but it is accompanied by a long list of deductions and exemptions that can bring your taxable income down sharply.

| Income Slab | Tax Rate |

|---|---|

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Under the old regime, the Section 87A rebate applies if taxable income after all deductions falls below ₹5 lakh, resulting in zero tax. The standard deduction for salaried employees is ₹50,000.

Every Deduction the Old Regime Allows

Section 80C covers the most common deductions with a combined cap of ₹1,50,000 — EPF and VPF contributions, PPF investments, LIC premiums, ELSS mutual funds, and home loan principal repayment. Use the PPF Calculator to see how your contributions compound →

Section 80D covers health insurance premiums: up to ₹25,000 for yourself, spouse, and children, plus an additional ₹25,000 (or ₹50,000 for senior citizen parents) for your parents' health insurance — bringing the total possible 80D deduction to ₹75,000.

HRA exemption is one of the most valuable deductions for those in rented accommodation. The exempt amount is the minimum of: the actual HRA received, rent paid minus 10% of basic salary, or 50% of basic salary for metro cities (40% for non-metros). Use the HRA Calculator to find your exact exemption →

Section 24b allows you to deduct up to ₹2,00,000 in home loan interest paid on a self-occupied property.

Section 80CCD(1B) gives you an additional deduction of ₹50,000 for NPS contributions — over and above the ₹1.5 lakh 80C limit. Model your NPS corpus and tax saving →

Head-to-Head Tax Comparison at Every Income Level

The table below compares tax payable (including 4% health and education cess) under both regimes, assuming a realistic deduction package of ₹3.75 lakh under the old regime — comprising ₹50,000 standard deduction, ₹1,50,000 under 80C, ₹1,00,000 HRA exemption, ₹50,000 NPS 80CCD(1B), and ₹25,000 under 80D.

| Gross Income | New Regime Tax | Old Regime Tax | Better Option | Saving |

|---|---|---|---|---|

| ₹7,00,000 | ₹0 | ₹22,100 | New | ₹22,100 |

| ₹10,00,000 | ₹0 | ₹54,600 | New | ₹54,600 |

| ₹12,00,000 | ₹0 | ₹1,09,200 | New | ₹1,09,200 |

| ₹15,00,000 | ₹1,04,000 | ₹1,09,200 | New (barely) | ₹5,200 |

| ₹18,00,000 | ₹1,82,000 | ₹1,56,000 | Old | ₹26,000 |

| ₹20,00,000 | ₹2,34,000 | ₹1,71,600 | Old | ₹62,400 |

| ₹25,00,000 | ₹3,90,000 | ₹3,28,900 | Old | ₹61,100 |

| ₹35,00,000 | ₹7,02,000 | ₹5,85,000 | Old | ₹1,17,000 |

| ₹50,00,000 | ₹11,46,000 | ₹9,96,000 | Old | ₹1,50,000 |

The pattern is clear. Below ₹12.75 lakh, the new regime is almost always the winner — often by a very wide margin due to the 87A rebate. Between ₹15 lakh and ₹17 lakh, the margin is tight and depends on your exact deduction profile. Above ₹18 lakh, the old regime consistently wins if you have meaningful deductions.

The Crossover Point: Where Does the Old Regime Start Winning?

The crossover is not a fixed income number — it shifts based on your total deductions. If your actual deductions exceed the break-even threshold for your income, the old regime saves you money. If they fall short, the new regime is cheaper.

As a practical rule of thumb: if your gross income is ₹15 lakh, you need deductions above roughly ₹3.25 lakh for the old regime to win. At ₹20 lakh, the threshold rises to about ₹3.75 lakh. At ₹30 lakh, even ₹3 lakh in deductions makes the old regime superior, because the slab rate gap at higher incomes means even modest deductions shift the outcome decisively.

Most salaried employees with a home loan, active 80C investments, NPS contributions, and HRA can easily accumulate ₹4–5 lakh in combined deductions. At that level, the old regime wins from ₹16–17 lakh onwards.

Four Real Scenarios — Which Regime Wins?

Scenario 1: Priya, Software Engineer, ₹10 LPA, No Home Loan

Priya earns ₹10 lakh per year and lives in a company-leased apartment, so she has no HRA or home loan interest to claim. Her total deductions add up to just ₹2 lakh (standard deduction + PF). Under the new regime, she pays zero tax due to the 87A rebate. Under the old regime, her taxable income after deductions is ₹8 lakh and she pays around ₹75,400. The new regime saves her over ₹75,000 — a clear winner.

Scenario 2: Rahul, Product Manager, ₹18 LPA, Renting in Mumbai

Rahul pays ₹35,000/month rent in Mumbai and has built up ₹1.5 lakh in 80C investments, ₹50,000 in NPS, and ₹25,000 in health insurance. His HRA exemption works out to roughly ₹1.2 lakh. Total deductions: approximately ₹4.45 lakh. His old-regime tax bill is around ₹1.56 lakh versus ₹1.82 lakh under the new regime. The old regime saves him around ₹26,000.

Scenario 3: Anjali, Finance Manager, ₹25 LPA, Home Loan of ₹60 Lakh

Anjali has a home loan with annual interest of ₹1.8 lakh, full 80C at ₹1.5 lakh, NPS at ₹50,000, 80D at ₹25,000, and a standard deduction of ₹50,000. Her total deductions come to ₹4.55 lakh. Her old-regime tax is approximately ₹3.29 lakh versus ₹3.90 lakh under the new regime — a saving of over ₹61,000 by sticking with the old regime.

Scenario 4: Vikram, Senior Director, ₹50 LPA, Full Deductions

At this income level, the 30% slab applies to a large chunk of income under both regimes. Vikram's deductions of ₹4.5 lakh reduce his old-regime tax to about ₹9.96 lakh compared to ₹11.46 lakh under the new regime — a saving of ₹1.5 lakh annually simply by choosing the right regime. Model your own scenario with the Income Tax Calculator →

Deductions That Are Still Allowed Under the New Regime

The new regime is not entirely deduction-free. A few key benefits survive:

- Standard deduction of ₹75,000 applies to all salaried employees — ₹25,000 more than under the old regime.

- Employer NPS contribution under Section 80CCD(2) can still be claimed — this is your company's contribution to your NPS, not your own.

- Gratuity, leave encashment, and agniveer corpus fund exemptions remain intact.

How to Switch Regimes — and the Deadline You Cannot Miss

Salaried employees can switch between regimes every financial year by informing their employer at the start of the year. Your employer needs your declaration to calculate the correct TDS. If you miss this window, you are not stuck — you can still choose the correct regime when filing your ITR, and any excess or shortfall will be adjusted. However, it is far easier to get it right upfront so your monthly in-hand salary is not affected.

Self-employed individuals and business owners face a slightly different rule: once you opt out of the new regime, you can switch back only once in a lifetime. Salaried employees enjoy more flexibility and can switch freely each year.

A Simple Decision Framework

If your gross income is below ₹12.75 lakh: choose the new regime. The 87A rebate makes your tax zero, and no amount of deductions under the old regime can beat that.

If your income is between ₹12.75 lakh and ₹17 lakh: tally up all your actual deductions. Use the Income Tax Calculator to compare. The margin is close and your specific profile — rent paid, home loan status, NPS contributions — will tip the scale.

If your income is above ₹17 lakh and you actively invest in 80C instruments, pay rent, or service a home loan: the old regime will almost certainly save you more money. The saving grows larger as your income rises, because the 30% bracket makes every rupee of deduction worth ₹0.30 in tax saved (before cess).

Frequently Asked Questions

Yes, for practical purposes. The Section 87A rebate under the new regime reduces tax to zero for total income up to ₹12,00,000. For salaried employees, the ₹75,000 standard deduction means this zero-tax benefit effectively extends to gross salary of ₹12,75,000. No combination of old-regime deductions can produce a lower outcome than zero.

No. HRA exemption is not available under the new tax regime. If you pay significant rent and receive a substantial HRA component in your salary, this is one of the strongest reasons to evaluate whether the old regime saves you more. Use the HRA Calculator to quantify your exemption before deciding.

At ₹15 lakh gross salary, the new regime tax (including cess) is approximately ₹1,04,000. For the old regime to match this, your combined deductions need to exceed roughly ₹3.25 lakh. This is achievable with full 80C, standard deduction, and either HRA or home loan interest — but if you have few investments and no home loan, the new regime likely wins even at this income level.

Yes, salaried employees can switch regimes each financial year by informing their employer at the start of the year. If the declaration is missed, the switch can still be made at the time of filing the ITR, with excess or shortfall TDS adjusted accordingly. Business owners and self-employed individuals do not get this annual flexibility — once they opt out of the new regime, they can switch back only once in a lifetime.

No. Section 80C deductions — which cover EPF, PPF, ELSS, LIC, NSC, and home loan principal repayment — are not available under the new tax regime. The new regime trades away all major deductions for lower slab rates. If you have already maximised your 80C, factor this in carefully before choosing the new regime.

For most home loan borrowers earning above ₹15 lakh, the old regime is likely to be better. Section 24b allows a deduction of up to ₹2 lakh on home loan interest for a self-occupied property, which alone provides significant tax relief. Add 80C (which includes principal repayment), standard deduction, and any HRA or 80D claims, and the old regime usually produces a lower tax bill.

Disclaimer: This article is for educational and informational purposes only. All tax figures are based on Income Tax Act provisions for FY 2026-27 (AY 2027-28) as applicable to resident individuals below 60 years of age. CalcPhi calculators are estimation tools and do not constitute financial or tax advice. Please consult a qualified Chartered Accountant or SEBI-registered financial advisor for personalised guidance before making tax-related decisions.