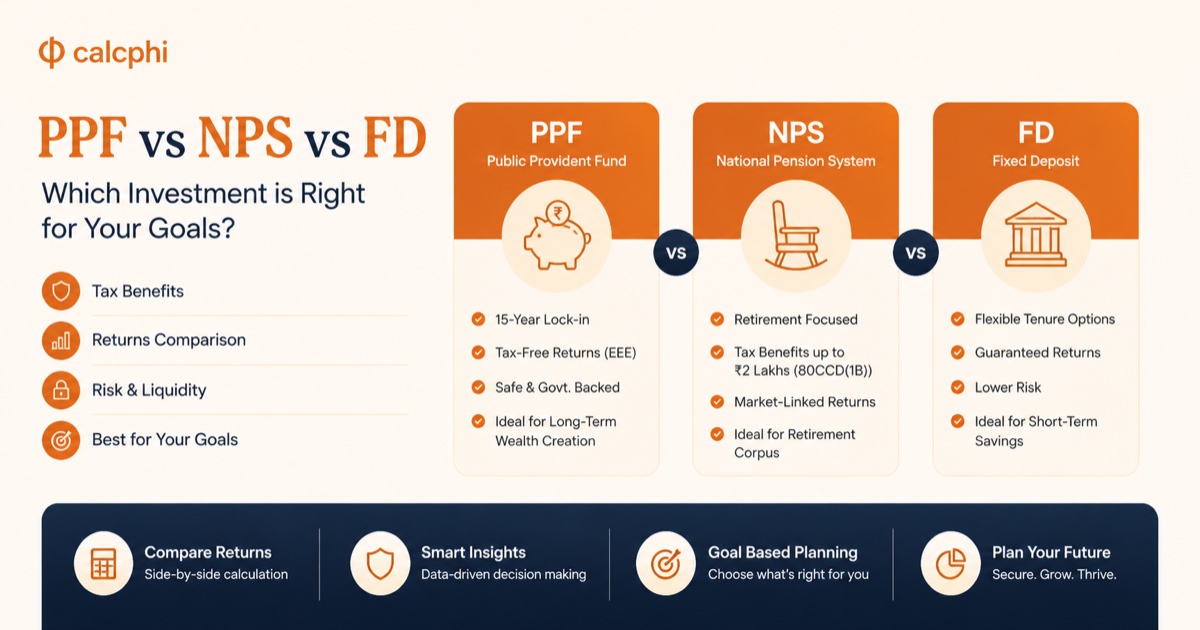

PPF vs NPS vs FD: Where to Park Your Long-Term Money in 2026?

When it comes to safe, government-backed savings in India, three options dominate the conversation: the Public Provident Fund (PPF), the National Pension System (NPS), and Fixed Deposits (FDs). All three are considered reliable. All three earn you a reasonable return. But if you are parking money for 15 to 25 years, the differences between them — in taxation, liquidity, inflation protection, and total wealth creation — can add up to several lakhs.

This guide breaks down every dimension that matters, with real numbers, tax calculations, and a clear recommendation for different investor profiles.

Quick Comparison: PPF vs NPS vs FD at a Glance

| Feature | PPF | NPS (Tier I) | Fixed Deposit |

|---|---|---|---|

| Current return | 7.1% (guaranteed) | 8–11% (market-linked) | 6.5–7.5% (bank rate) |

| Return type | Fixed, govt-set quarterly | Variable — equity/debt mix | Fixed for full tenure |

| Tax on contribution | 80C up to ₹1.5L | 80C + 80CCD(1B) ₹50K extra | 80C for 5-yr tax-saver FD only |

| Tax on returns | Fully tax-free (EEE) | 60% tax-free; annuity taxed | Fully taxable at slab rate |

| Lock-in period | 15 years (extendable) | Until age 60 (mandatory) | 7 days to 10 years |

| Liquidity | Partial after Year 7 | Very restricted until 60 | Premature exit with penalty |

| Risk level | Zero — sovereign guarantee | Low–medium (market exposure) | Zero (₹5L DICGC insured) |

| Min investment | ₹500 per year | ₹500 per month (Tier I) | ₹1,000 (most banks) |

| Max investment | ₹1,50,000 per year | No upper limit | No upper limit |

What Is PPF and Who Should Use It?

PPF, or the Public Provident Fund, is a government-savings scheme backed by the Ministry of Finance. The interest rate is currently 7.1% per annum for Q1 FY 2026-27, compounded annually. The entire scheme works on an EEE (Exempt-Exempt-Exempt) tax model — contributions qualify for Section 80C deduction, the interest earned is tax-free, and the maturity amount is completely exempt from tax.

The minimum lock-in is 15 years, which makes PPF a genuinely long-term instrument. Partial withdrawals are allowed from Year 7 onwards, and you can take a loan against your PPF balance between Years 3 and 6. Full premature closure is allowed only in exceptional cases like life-threatening illness or a child's higher education, and only after five years.

PPF is ideal for investors in the 20% to 30% tax bracket who want a risk-free, inflation-beating instrument with tax-free returns. For high earners, the post-tax return on PPF at 7.1% comfortably beats a taxable FD at 7.5% — since at 30% tax the effective FD return drops to roughly 5.25%.

→ Model your PPF maturity value with year-by-year breakdowns →

What Is NPS and Who Should Use It?

NPS, or the National Pension System, is a market-linked retirement savings scheme regulated by PFRDA. Unlike PPF, NPS invests your money in a mix of equities, corporate bonds, and government securities — which is why returns are not guaranteed but have historically ranged between 8% and 11% depending on asset allocation.

The key tax advantage of NPS is its additional deduction of ₹50,000 under Section 80CCD(1B), over and above the ₹1,50,000 limit under Section 80C. A salaried professional in the 30% bracket can save an additional ₹15,600 in tax every year just by contributing to NPS — a benefit no other government-savings instrument offers.

The major drawback is illiquidity. Tier I NPS accounts are locked until age 60, with limited exceptions. At retirement, you must use at least 40% of the corpus to purchase an annuity, and only 60% can be withdrawn as a lump sum. The 60% lump-sum withdrawal is tax-free, but the annuity payments are taxed as regular income. NPS also offers a Tier II account with no lock-in, but Tier II contributions do not enjoy the same tax benefits as Tier I.

→ Calculate your NPS corpus and estimated monthly pension →

What Is a Fixed Deposit and When Does It Make Sense?

A Fixed Deposit is offered by banks and NBFCs and allows you to park a lump sum at a fixed interest rate for a chosen tenure. There is no investment limit, the returns are guaranteed, and up to ₹5 lakh per depositor per bank is insured under DICGC.

The biggest drawback of FDs for long-term wealth building is tax. The interest income is added to your total income every year and taxed at your applicable slab rate. If your annual FD interest exceeds ₹40,000 (₹50,000 for senior citizens), the bank deducts TDS at 10%. For anyone in the 30% bracket, this means the effective post-tax return on a 7.0% FD is around 4.9%.

There is one exception: the five-year tax-saver FD, which qualifies for Section 80C deduction. However, this has a five-year lock-in, and the interest is still taxed. It is only useful if you have not exhausted your 80C limit through other instruments.

Where FDs genuinely shine is in the short to medium term — one to five years — and for investors in the 0% or 5% tax bracket. Senior citizens get an additional 0.25% to 0.50% on FD rates and also have access to the Senior Citizen Savings Scheme (SCSS) at 8.2% per annum.

→ FD maturity and interest calculator →

The Real Numbers: Returns Over 20 Years

We model ₹1,50,000 invested every year for 20 years — the maximum allowed in PPF, and a consistent benchmark across all three options. For NPS, we use a conservative 10% blended annual return based on a 60:40 equity-debt allocation. For FD, we assume 7% with annual compounding and reinvestment at the same rate.

| Option | Total Invested | Maturity Value (Pre-Tax) | Gains |

|---|---|---|---|

| PPF @ 7.1% | ₹30,00,000 | ₹66,58,000 | ₹36,58,000 |

| NPS @ 10% (assumed) | ₹30,00,000 | ₹94,37,000 | ₹64,37,000 |

| FD @ 7.0% | ₹30,00,000 | ₹63,47,000 | ₹33,47,000 |

These are pre-tax figures. When you apply the tax treatment, the story changes significantly. NPS at 10% still wins on absolute wealth — but only 60% of the ₹94.37 lakh is available as a tax-free lump sum (approximately ₹56.6 lakh). The remaining 40% must be annuitised, and the monthly pension received is taxed at your slab rate in retirement.

PPF at ₹66.58 lakh is entirely tax-free — every rupee of it. The FD at ₹63.47 lakh pre-tax becomes significantly less on a post-tax basis if you have been paying 30% tax on the interest each year.

Post-Tax Return Comparison

| Option | Pre-Tax Return | Effective Post-Tax Return |

|---|---|---|

| PPF | 7.1% | 7.1% — fully EEE exempt |

| NPS (blended) | ~10% | ~8.2–8.5% — 60% corpus tax-free; annuity taxed |

| FD (30% bracket) | 7.0% | ~4.9% — fully taxable each year |

For investors in the 30% bracket, PPF effectively beats FD on a post-tax basis despite having a similar pre-tax rate. And because PPF returns are EEE, they are unaffected by changes in your income level in future years — unlike FD interest, which is taxed at whatever your current slab rate happens to be.

Liquidity and Flexibility: Which Option Gives You Access When You Need It?

PPF Liquidity Rules

You cannot touch your PPF balance in the first three years. From Year 4 to Year 6, you can take a loan against your PPF balance at 1% above the prevailing PPF rate. From Year 7 onwards, you can make one partial withdrawal per year — up to 50% of the balance at the end of Year 4, or 50% of the balance at the end of the previous year, whichever is lower.

NPS Liquidity Rules

NPS Tier I is the most restrictive. You cannot withdraw before age 60 except in PFRDA-approved circumstances — and even then, you can only withdraw up to 25% of your own contributions after three years of membership. At age 60, you must annuitise at least 40% of the corpus. If you exit before 60, you must annuitise at least 80%, keeping only 20% as a lump sum.

FD Liquidity Rules

FDs offer the most flexibility. You can break a fixed deposit at any time — though banks typically charge a penalty of 0.5% to 1% on the applicable rate for premature withdrawal. This makes FDs the right choice for your emergency fund or any money you might need in the next three to five years.

Tax Benefit Deep Dive: How Much Can You Actually Save?

Tax savings for a salaried employee earning ₹15 lakh per year under the old tax regime:

| Investment | Deduction Available | Tax Saved |

|---|---|---|

| PPF — ₹1,50,000 | ₹1,50,000 under 80C | ₹46,800 |

| NPS Tier I — ₹50,000 | ₹50,000 under 80CCD(1B) | ₹15,600 |

| 5-Yr Tax Saver FD | Shared with 80C — no extra benefit | ₹0 additional |

| PPF + NPS combined | ₹2,00,000 total | ₹62,400 per year |

The NPS 80CCD(1B) deduction of ₹50,000 is over and above the 80C limit of ₹1,50,000 — making it unique. If you max out PPF and also contribute ₹50,000 to NPS, you get deductions on ₹2,00,000 of income every year. At the 30% bracket with 4% cess, that is ₹62,400 in annual tax savings.

→ Calculate your exact tax saving under both regimes →

Inflation Protection: Which Instrument Preserves Your Purchasing Power?

At an average inflation rate of 5.5% in India over the past decade, real return matters — not the nominal rate.

- PPF at 7.1% gives a real return of approximately 1.6% above inflation — modest but positive, and entirely risk-free.

- NPS with equity exposure at 10% gives a real return of roughly 4.5% — meaningfully better for long-term wealth building.

- FD at 7.0% gives a real return of about 1.5% before tax. Once you factor in 30% tax, the real post-tax return on FD for a high earner is essentially zero or even slightly negative in high-inflation years.

This is the fundamental problem with using FDs for long-term wealth. They do not lose money in nominal terms — but they may well erode your purchasing power in real terms once tax and inflation are accounted for. For money you need to keep safe for 15 to 25 years, PPF is the minimum viable option, and NPS is the stronger wealth-building vehicle for investors comfortable with controlled equity exposure.

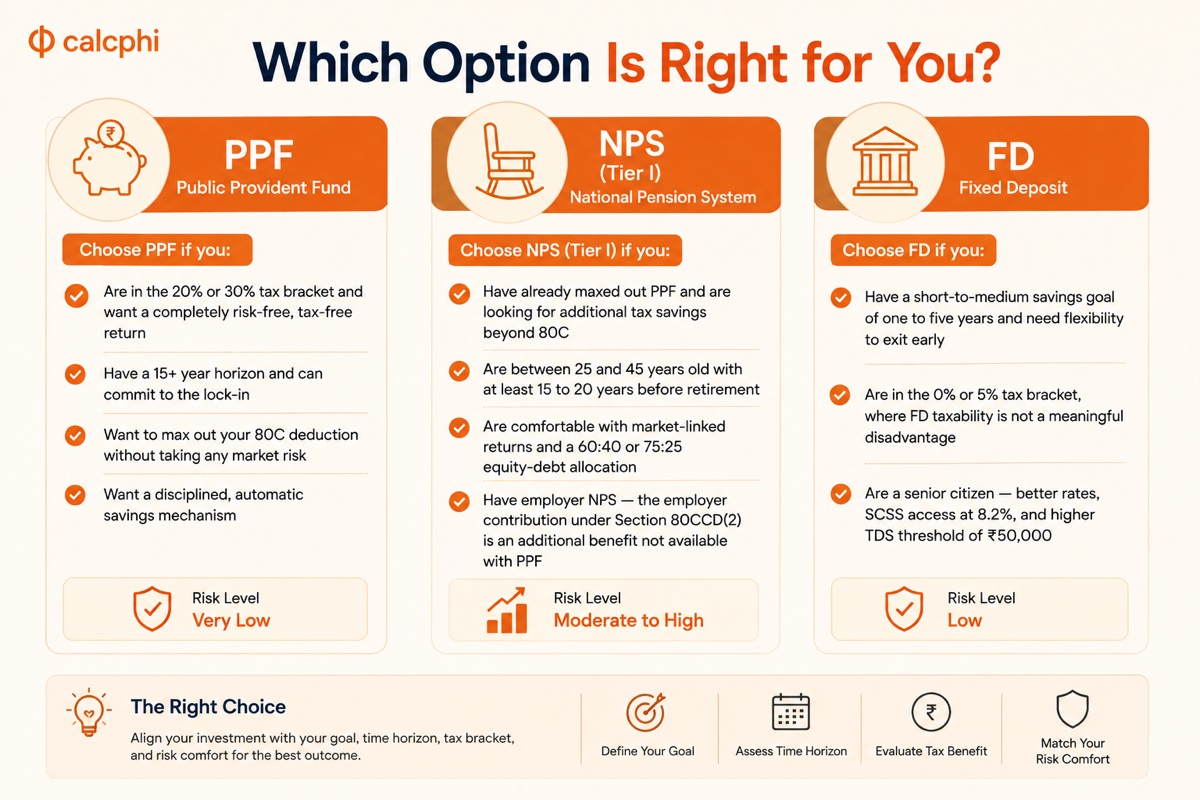

Which Option Is Right for You?

Choose PPF if you:

- Are in the 20% or 30% tax bracket and want a completely risk-free, tax-free return

- Have a 15+ year horizon and can commit to the lock-in

- Want to max out your 80C deduction without taking any market risk

- Want a disciplined, automatic savings mechanism

Choose NPS (Tier I) if you:

- Have already maxed out PPF and are looking for additional tax savings beyond 80C

- Are between 25 and 45 years old with at least 15 to 20 years before retirement

- Are comfortable with market-linked returns and a 60:40 or 75:25 equity-debt allocation

- Have employer NPS — the employer contribution under Section 80CCD(2) is an additional benefit not available with PPF

Choose FD if you:

- Have a short-to-medium savings goal of one to five years and need flexibility to exit early

- Are in the 0% or 5% tax bracket, where FD taxability is not a meaningful disadvantage

- Are a senior citizen — better rates, SCSS access at 8.2%, and higher TDS threshold of ₹50,000

The Smart Combination: PPF + NPS + FD Together

For a salaried professional aged 30 to 45 in the 30% tax bracket, the most effective long-term savings strategy is not to choose one instrument — it is to use all three for different purposes.

- PPF — ₹1,50,000/year: maxes out your 80C deduction, earns tax-free returns, and gives you some liquidity from Year 7.

- NPS Tier I — ₹50,000/year: gives you the additional 80CCD(1B) deduction and equity-driven growth for your retirement corpus.

- FD — 3 to 6 months of expenses: your emergency fund where you do not mind paying some tax because you may need this money at short notice.

This combination gives you ₹62,400 in annual tax savings, a diversified savings structure across zero-risk and market-linked instruments, and enough liquidity for genuine emergencies.

Frequently Asked Questions

Yes, for most investors in the 20% to 30% tax bracket, PPF is significantly better than FD for long-term savings. PPF returns are completely tax-free under the EEE model, while FD interest is taxed at your slab rate every year. At a 30% tax rate, a 7% FD has an effective post-tax return of around 4.9% — well below PPF's tax-free 7.1%. The only scenario where FD wins over PPF for the long term is if you are in the nil or 5% tax bracket.

Yes, and this is the recommended strategy for most salaried professionals. PPF contributions count towards your Section 80C limit (up to ₹1,50,000), while NPS Tier I contributions of up to ₹50,000 qualify for an additional deduction under Section 80CCD(1B) — completely separate from the 80C limit. Combining both gives you deductions on ₹2,00,000 of annual income and ₹62,400 in annual tax savings at the 30% bracket.

If an NPS subscriber dies before age 60, the entire corpus is paid out to the nominated beneficiary or legal heir as a lump sum — with no mandatory annuity requirement. The family is not forced to purchase a pension plan. This lump sum payment is exempt from tax in the hands of the nominee, making NPS a reasonable part of an estate-planning strategy.

No, FD interest is taxable for senior citizens — it is added to their total income and taxed at their slab rate. However, senior citizens enjoy a higher TDS exemption threshold of ₹50,000 per year before the bank starts deducting TDS. Section 80TTB also allows senior citizens to deduct up to ₹50,000 of interest income from savings accounts and FDs.

The PPF interest rate for Q1 FY 2026-27 (April to June 2026) is 7.1% per annum, compounded annually. The rate is reviewed and set by the Government of India every quarter based on the yields of comparable government securities. It has been stable at 7.1% since April 2020.

If you have opted for the new tax regime, you cannot claim deductions under Section 80C or 80CCD(1B), which eliminates the primary tax advantage of NPS Tier I and PPF. However, if your employer makes contributions to your NPS Tier I account, Section 80CCD(2) deductions are available even under the new regime. For self-funded contributions with no employer component, the new regime makes NPS and PPF less tax-efficient.

Disclaimer: CalcPhi's PPF, NPS, FD, and income tax calculators are designed for educational and estimation purposes only. The figures, projections, and comparisons in this article are illustrative and based on publicly available rates as of AY 2026-27. They do not constitute financial advice, tax advice, or investment recommendations. Tax laws and interest rates change regularly — always verify current rates on official government portals. Please consult a SEBI-registered investment advisor or a qualified Chartered Accountant for personalised financial guidance.