Retire at 50 in India: The Exact Corpus You Need and How to Build It

Most people treat early retirement as a fantasy rather than a financial target. The truth is, retiring at 50 is a solvable maths problem — not a lottery ticket. Once you know your monthly expenses, the rate at which prices rise, how long you expect to live, and what your investments will earn, you can calculate a precise number. This guide does exactly that, with figures grounded in Indian inflation data, Indian market return history, and the specific quirks of Indian retirement accounts like EPF and NPS that most generic FIRE calculators miss entirely.

Why "Retire at 50" Is Harder Than It Sounds in India

Retiring at 50 in India means funding roughly 35 to 40 years of life without a salary. That alone makes it one of the most capital-intensive financial goals you can set. Compare that to retiring at 60, where you need to fund 25 to 30 years — a meaningfully shorter horizon that requires far less corpus.

But the challenge goes beyond the timeline. India's average consumer price inflation has run at 5.5% to 6.5% over the last decade, according to RBI data. At 6% inflation, ₹1 lakh of monthly expenses today becomes ₹1.79 lakh per month in 10 years. By year 20, it's ₹3.2 lakh per month. Your corpus must not just survive these 35 years — it must comfortably outpace them.

There is also a structural problem unique to India that international FIRE guides never mention: your largest retirement accounts are locked until 58 to 60. EPF cannot be fully withdrawn until age 58. NPS Tier 1 is locked until 60. If you stop working at 50, you face an 8 to 10 year gap where you cannot touch these funds. You need what planners call a bridge corpus — a separate pool of freely accessible wealth that carries you from 50 to 58 before your locked accounts open up. This bridge corpus is entirely separate from your long-term retirement fund and must be planned for independently.

The Right Withdrawal Rate for India: Why 4% Doesn't Work Here

The famous 4% withdrawal rule was developed by financial planner William Bengen based on US market data going back to 1926. The rule says that if you withdraw 4% of your corpus in year one, then adjust that amount for inflation each year, a well-diversified portfolio has historically lasted at least 30 years without running out.

In India, this rule needs adjustment for two reasons. First, Indian inflation is structurally higher than US inflation — typically 5.5% to 7% versus 2% to 3% in developed markets. Second, Indian equity markets, while delivering strong long-term returns, are more volatile than US markets, especially in the 10 to 15 years following retirement when a large market drawdown could permanently damage your corpus.

A 3% to 3.5% withdrawal rate is more appropriate for Indian retirees. This pushes your required corpus multiplier from 25× annual expenses (the standard FIRE formula) to 28× to 33× annual expenses. It is a more conservative target, but it accounts for the reality of Indian inflation and the longer retirement horizon when retiring at 50.

Calculating Your Target Corpus: Three Real Scenarios

The figures below show how much corpus you need at age 50, depending on your current monthly expenses. These assume your current expenses inflate at 6% per year until retirement, a 3.3% withdrawal rate in retirement (roughly a 30× multiplier), and that your invested corpus earns 10% annually during retirement — a reasonable assumption for a 60:40 equity-to-debt portfolio. The person is assumed to be 35 years old today, retiring at 50.

| Monthly Expenses Today | Monthly Expenses at Age 50 | Annual Expenses at 50 | Corpus Required |

|---|---|---|---|

| ₹60,000/month | ~₹1.44 lakh/month | ~₹17.3 lakh | ₹5.18 crore |

| ₹1,00,000/month | ~₹2.40 lakh/month | ~₹28.8 lakh | ₹8.64 crore |

| ₹2,00,000/month | ~₹4.80 lakh/month | ~₹57.6 lakh | ₹17.28 crore |

These are not scare numbers — they are targets. And the earlier you start, the more achievable they become. Want to run these numbers with your exact expense level and age? Use CalcPhi's Early Retirement Calculator to get your personalised corpus figure in under a minute.

The Bridge Corpus Problem: The Gap Between 50 and 58

Here is the part most early retirement calculators skip. When you retire at 50, your EPF balance is locked until 58. Your NPS Tier 1 account cannot be accessed until 60. Together, these accounts may hold a significant portion of your wealth — yet you cannot touch them for 8 to 10 years.

You need a bridge corpus to cover this period independently. The bridge corpus is not part of your long-term retirement fund. It is a separate lump sum — ideally held in liquid mutual funds, short-duration debt funds, and fixed deposits — that pays your monthly expenses from age 50 to 58 without touching your main retirement corpus.

For someone spending ₹1.5 lakh per month at age 50, a bridge covering 8 years with 6% inflation means needing roughly ₹1.79 crore in accessible funds at retirement. This is money you must accumulate separately from your SIPs that are building the long-term corpus.

This is why retiring at 50 in India often requires a higher total wealth target than the simple corpus formula suggests. Your actual wealth goal at 50 = long-term retirement corpus + bridge corpus. Plan for both.

How Much to Save Each Month to Hit Your Target

If you are 30 today and targeting a corpus of ₹5.18 crore by age 50, you have 20 years. Assuming your investments earn 12% CAGR (consistent with long-term Nifty 50 returns including reinvested dividends), the required monthly SIP is approximately ₹47,500.

That number drops significantly if you already have savings. If you have ₹10 lakh already invested, your required monthly SIP to reach ₹5.18 crore at 12% CAGR drops to roughly ₹42,000. If you have ₹25 lakh already invested, it drops to about ₹34,000.

| Target Corpus | No Existing Savings | ₹10L Already Invested | ₹25L Already Invested |

|---|---|---|---|

| ₹5.18 crore (₹60K/mo expenses) | ~₹47,500/mo | ~₹42,000/mo | ~₹34,000/mo |

| ₹8.64 crore (₹1L/mo expenses) | ~₹79,000/mo | ~₹73,500/mo | ~₹65,500/mo |

| ₹17.28 crore (₹2L/mo expenses) | ~₹1,58,500/mo | ~₹1,53,000/mo | ~₹1,45,000/mo |

A step-up SIP — where you increase your monthly investment by 10% to 15% every year — is far more effective than a flat SIP. Starting with ₹25,000 per month and stepping up 12% annually reaches a much higher corpus than a flat ₹40,000 per month over the same period, simply because you are deploying more rupees in the years closer to retirement, when compounding has already done much of the heavy lifting. Try CalcPhi's Step-Up SIP Calculator to see exactly how much more wealth a 10% annual step-up generates compared to a flat SIP over 20 years — the difference is often 40% to 60% more wealth.

Where to Invest: The Right Asset Mix for Building a Retirement Corpus

During the accumulation phase — the years between now and age 50 — your portfolio should be equity-heavy. For someone with 15 to 20 years until retirement, an allocation of 80% equity and 20% debt is appropriate. The equity portion should be in diversified index funds or large-cap mutual funds via SIP, not in individual stocks or sector bets.

As you approach 50, begin shifting gradually. At age 45, reduce equity to 70%. At age 48, bring it down to 65%. At retirement, a 60:40 equity-to-debt allocation is a reasonable entry point. Never shift to all-debt at retirement — with 35 years ahead of you, you still need equity for long-term growth to keep your corpus ahead of inflation.

For the government scheme portion of your portfolio, PPF offers 7.1% tax-free returns with a 15-year lock-in (extendable). Maxing out your ₹1.5 lakh annual PPF contribution every year builds a meaningful, completely tax-free corpus over 15 to 20 years. Use CalcPhi's PPF Calculator to project exactly how much your PPF account will be worth at 50.

NPS, while locked until 60, is still worth contributing to for the additional ₹50,000 deduction under Section 80CCD(1B). But do not rely on it as your primary vehicle if you plan to retire at 50, given the lock-in. It works better as a supplement that keeps growing tax-efficiently between age 50 and 60, then pays you an annuity alongside your self-managed corpus.

The Tax Angle in Retirement: What Most People Overlook

Retiring at 50 does not mean your money is tax-free. The way you structure withdrawals from your corpus will significantly affect how long it lasts.

Equity mutual fund SWPs — systematic withdrawal plans — are a tax-efficient way to generate monthly income in retirement. Long-term capital gains on equity funds above ₹1.25 lakh per year are taxed at 12.5%. For someone with a ₹5 crore corpus, annual withdrawals of ₹17–18 lakh might be partially taxable, but much of it is return of capital rather than gains, keeping the effective tax burden manageable.

FD interest, on the other hand, is fully taxable as income. Using FDs heavily in retirement can push you into the 20% or 30% tax slab unnecessarily. Structuring your withdrawals across equity SWPs, PPF maturity, and debt mutual funds gives you far better after-tax income.

Use CalcPhi's Income Tax Calculator to estimate what your tax liability looks like in retirement at different withdrawal levels — before you lock in a withdrawal strategy.

The Lifestyle Costs Nobody Plans For

Beyond the numbers, there are predictable but often unplanned costs that erode a retirement corpus faster than expected.

Healthcare is the biggest one. India has no universal health cover. A cardiac procedure, a cancer treatment, or even a week in a private hospital ICU can cost ₹10 lakh to ₹50 lakh out of pocket. A comprehensive health insurance policy with a ₹1 crore sum assured is essential and must be purchased before age 50, ideally by 45, when you can still get cover without exclusions and at manageable premiums. Premiums for a ₹1 crore family floater policy for a 45-year-old couple typically range from ₹45,000 to ₹75,000 per year from leading insurers like Star Health or HDFC ERGO.

Children's higher education is another cost that often overlaps with early retirement. If your child is 15 when you retire at 50, you have 3 to 5 years of college fees and potentially an MBA or postgrad still to fund. A four-year engineering degree at a good private college costs ₹8 lakh to ₹20 lakh today. This amount must be earmarked separately and not counted as part of your retirement corpus.

Finally, inflation on lifestyle expenses tends to exceed CPI. Travel, dining, good-quality private healthcare, and urban rent inflate faster than the headline rate. Building in a 7% lifestyle inflation assumption rather than the standard 6% gives you a more realistic picture.

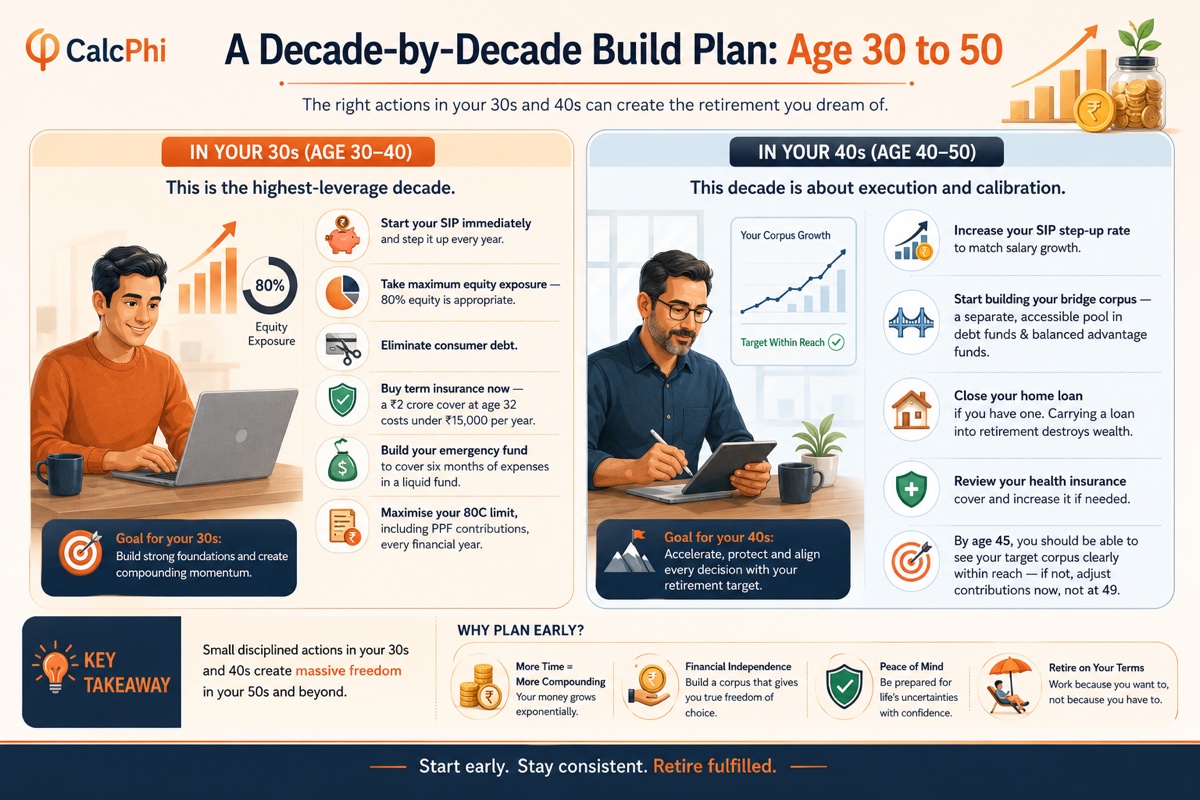

A Decade-by-Decade Build Plan: Age 30 to 50

In Your 30s (Age 30–40)

This is the highest-leverage decade. Start your SIP immediately and step it up every year. Take maximum equity exposure — 80% equity is appropriate. Eliminate consumer debt. Buy term insurance now — a ₹2 crore cover at age 32 costs under ₹15,000 per year. Build your emergency fund to cover six months of expenses in a liquid fund. Maximise your 80C limit, including PPF contributions, every financial year.

In Your 40s (Age 40–50)

This decade is about execution and calibration. Increase your SIP step-up rate to match salary growth. Start building your bridge corpus — this should be a separate, accessible investment account growing in debt funds and balanced advantage funds. Close your home loan if you have one, since carrying a loan into retirement is one of the fastest ways to destroy a retirement plan. Review your health insurance cover and increase it if needed. By age 45, you should be able to see your target corpus clearly within reach — if not, adjust contributions now, not at 49.

Frequently Asked Questions

-

Is ₹3 crore enough to retire at 50 in India?

At a 3.3% withdrawal rate, ₹3 crore generates ₹9.9 lakh per year or about ₹82,500 per month in today's purchasing power. For a modest lifestyle in a Tier 2 city with no major loans or dependents, ₹3 crore may be workable — but it leaves very little room for healthcare emergencies or lifestyle inflation over 35 years. For most people in metro cities, ₹3 crore is not a safe retirement corpus at age 50.

-

Can I retire at 50 if I have a home loan running?

It is strongly inadvisable. An active home loan EMI after retirement is a fixed, non-negotiable monthly outflow that burns through your corpus faster than any market downturn. Close all outstanding loans before retiring, even if it means delaying retirement by two to three years.

-

What is the bridge corpus and how much do I need?

The bridge corpus is the accessible money that funds your expenses from age 50 to 58, before your EPF and NPS accounts become available. To estimate yours: take your monthly expenses at age 50, grow them at 6% annually for 8 years, and calculate the total. A rough rule of thumb is 8 to 10 times your first-year annual retirement expenses, held in liquid or short-duration instruments.

-

Should I use NPS if I plan to retire at 50?

Yes, but only as a supplement — not your primary vehicle. NPS Tier 1 is locked until 60, so you cannot access it for 10 years after you stop working. However, contributing ₹50,000 per year gives you an additional income tax deduction under Section 80CCD(1B), which is valuable during your accumulation years. The NPS corpus that builds between age 50 and 60 also becomes a useful annuity income stream later.

-

How do I handle healthcare costs in retirement?

Buy a high-sum health insurance policy — ideally ₹1 crore or more — before age 50. Premiums are significantly lower at 45 than at 55, and you reduce the risk of exclusions for pre-existing conditions. Additionally, set aside a separate healthcare contingency fund of ₹20–30 lakh in a liquid instrument to cover treatments or procedures not covered by insurance.

-

What return rate should I assume for my retirement corpus?

During accumulation (pre-retirement), 12% CAGR is a reasonable long-term assumption for a diversified equity portfolio, based on the Nifty 50's historical performance over 20-year periods. During retirement, assume 10% gross returns on a 60:40 equity-debt portfolio, then subtract 6% inflation, leaving roughly 3.8% to 4% real returns — which is consistent with a sustainable 3.3% to 3.5% withdrawal rate.

Run your retirement numbers:

Early Retirement Calculator → Retirement Corpus Calculator → Step-Up SIP Calculator → PPF Calculator →Disclaimer:All figures in this article are for educational and estimation purposes only. Inflation, market returns, tax rates, and personal circumstances vary. Nothing in this article constitutes financial advice. Please consult a SEBI-registered financial advisor for guidance specific to your situation.