CTC vs In-Hand Salary: Why Your Offer Letter Is Lying to You

You worked hard to crack the interview. You negotiated confidently. The recruiter finally said the magic words: "We'd like to offer you ₹15 LPA." You accepted, smiled, and started planning your life around that number.

Then your first salary hits the bank — ₹88,000. You do the math. ₹88,000 × 12 = ₹10.56 lakh. That's nearly ₹4.5 lakh less than what the offer letter said. Where did it go? The answer: no one stole it. The gap between your CTC and your actual take-home salary isn't a scam — it's a deeply misunderstood part of how Indian compensation works, and almost every salaried employee discovers it the hard way.

What Does CTC Actually Mean?

CTC stands for Cost to Company. It is the total annual amount your employer spends because of you — not the amount they pay you. The distinction matters enormously.

Your CTC includes everything: your monthly salary, components you may never directly spend (like employer's provident fund contributions), provisions for future payouts (like gratuity), insurance premiums the company pays on your behalf, and sometimes even the cost of office space or equipment in large corporations.

Think of it this way: if your company hires you and the total cost of keeping you on payroll is ₹15 lakh per year — including their share of your PF, the group health insurance, and the gratuity they're setting aside — that's your CTC. But you only receive the portion that hits your bank account, after your own deductions.

Breaking Down a ₹15 LPA CTC: What the Structure Looks Like

Every CTC has two major parts: gross salary (the cash components before your deductions) and non-cash components (benefits that the employer pays for but that don't appear in your bank account). Here's how a typical ₹15 LPA CTC is structured for a salaried employee in a metro city:

| Component | Monthly Amount | Annual Amount | Taxability |

|---|---|---|---|

| Basic Salary (40% of CTC) | ₹50,000 | ₹6,00,000 | Fully taxable |

| HRA (50% of Basic — metro) | ₹25,000 | ₹3,00,000 | Partially/fully exempt if rent paid |

| Special Allowance | ₹21,667 | ₹2,60,004 | Fully taxable |

| LTA (Leave Travel Allowance) | — | ₹20,000 | Tax-free on actual travel |

| Food/Meal Allowance | ₹2,200 | ₹26,400 | Tax-exempt up to ₹26,400/year |

| Gross Salary | ~₹98,867 | ~₹11,86,404 |

| Component | Annual Amount | Notes |

|---|---|---|

| Employer PF (12% of Basic) | ₹72,000 | Goes to your EPF — counted in CTC |

| Gratuity Provision (4.81% of Basic) | ₹28,860 | You get this after 5+ years of service |

| Group Health Insurance Premium | ₹15,000 | Employer pays; you don't receive cash |

| Total Non-Cash | ₹1,15,860 | |

| Total CTC | ~₹15,02,264 | Rounded to ₹15 LPA |

Your gross salary is about ₹11.86 lakh annually, but your CTC is ₹15 lakh because the employer adds ₹3.14 lakh in non-cash components on top of it.

The Deductions That Hit You Every Month

Even from your gross salary, several amounts get deducted before the money lands in your account. These are deductions from you — the employee — not extras paid by the employer.

| Deduction | Monthly Amount | Notes |

|---|---|---|

| Employee PF (12% of Basic) | ₹6,000 | Mandatory; goes to your EPF account |

| Professional Tax (Maharashtra) | ₹200 | State-specific; varies by state |

| TDS (Income Tax at Source) | ~₹4,500 | Estimated; depends on regime and investments |

| Total Deductions | ~₹10,700 | |

| In-Hand (Take-Home) | ~₹88,167 |

The CTC Gap at Different Salary Levels

The gap between CTC and take-home isn't uniform. At higher salaries, income tax takes a much larger chunk. Here's a quick comparison across common CTC bands for AY 2026-27, assuming the new tax regime (default from FY 2024-25):

| CTC (Annual) | Approx. Gross Monthly | Approx. Take-Home (Monthly) | Monthly Gap |

|---|---|---|---|

| ₹6 LPA | ₹50,000 | ₹44,000–₹46,000 | ~₹4,000–₹6,000 |

| ₹10 LPA | ₹83,333 | ₹68,000–₹72,000 | ~₹11,000–₹15,000 |

| ₹15 LPA | ₹1,25,000 | ₹86,000–₹92,000 | ~₹33,000–₹39,000 |

| ₹20 LPA | ₹1,66,667 | ₹1,10,000–₹1,18,000 | ~₹48,000–₹57,000 |

| ₹30 LPA | ₹2,50,000 | ₹1,55,000–₹1,70,000 | ~₹80,000–₹95,000 |

The gap widens significantly as income grows, mainly because income tax rates are progressive — the more you earn, the higher percentage you pay on each additional rupee. Want to calculate your exact take-home without guesswork? Use CalcPhi's free CTC to In-Hand Calculator — plug in your CTC and get a full monthly breakdown in seconds.

Understanding Each Deduction in Plain English

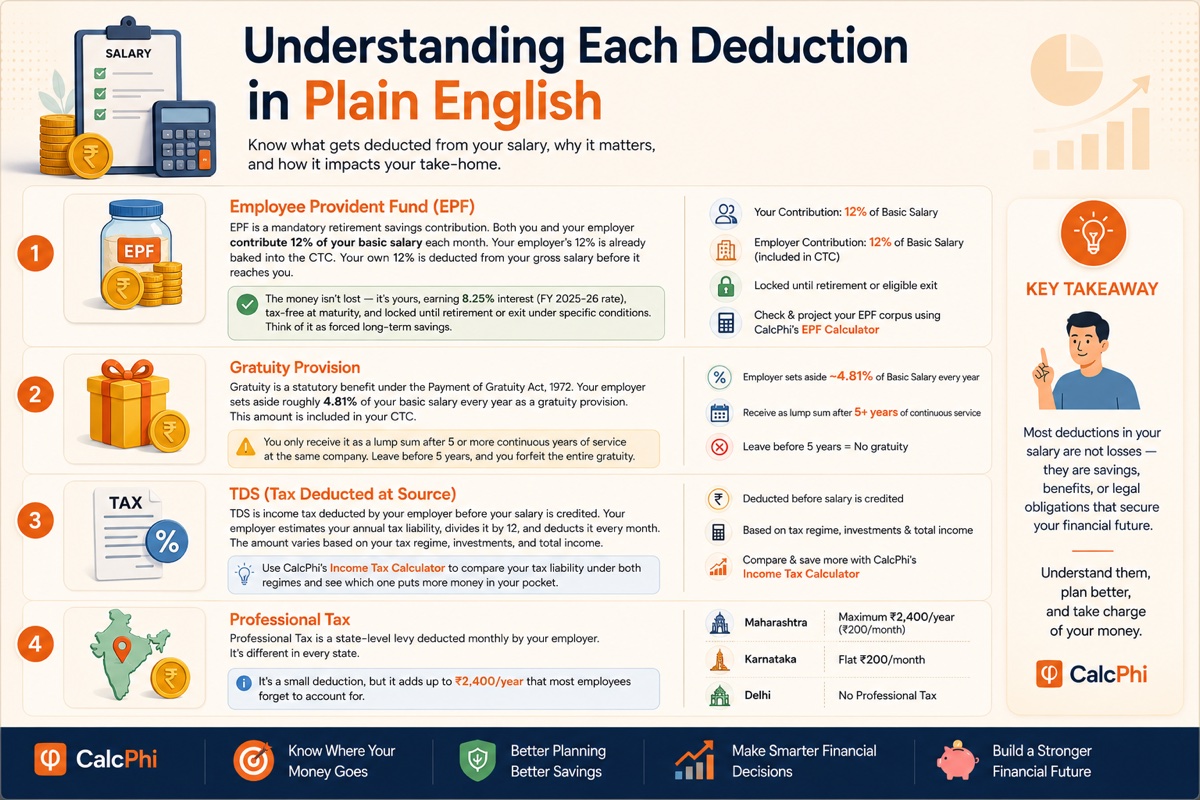

Employee Provident Fund (EPF)

EPF is a mandatory retirement savings contribution. Both you and your employer contribute 12% of your basic salary each month. Your employer's 12% is already baked into the CTC. Your own 12% is deducted from your gross salary before it reaches you. The money isn't lost — it's yours, sitting in your EPF account earning 8.25% interest (FY 2025-26 rate), and it's tax-free at maturity. But it's locked until you retire or leave employment under specific conditions. Think of it as forced long-term savings. Check and project your EPF corpus using CalcPhi's EPF Calculator.

Gratuity Provision

Gratuity is a statutory benefit under the Payment of Gratuity Act, 1972. Your employer sets aside roughly 4.81% of your basic salary every year as a gratuity provision. This amount is included in your CTC, but you only receive it as a lump sum after completing five or more continuous years of service at the same company. If you leave before five years, you forfeit the entire gratuity — which is why the provision shows up in your CTC but might never come to you at certain points in your career.

TDS (Tax Deducted at Source)

TDS is income tax deducted by your employer before your salary is credited. Your employer estimates your annual tax liability at the beginning of the year, divides it by 12, and deducts it every month. The amount varies depending on which tax regime you've opted for, what investments you've declared, and your total income. Use CalcPhi's Income Tax Calculator to compare your tax liability under both regimes and see which one puts more money in your pocket.

Professional Tax

Professional Tax is a state-level levy deducted monthly by your employer. It's different in every state. Maharashtra charges a maximum of ₹2,400/year (₹200/month). Karnataka charges a flat ₹200/month. Some states like Delhi don't have it at all. It's a small deduction, but it adds up to ₹2,400/year that most employees forget to account for.

Old vs New Tax Regime: Which One Reduces Your TDS More?

From FY 2024-25, the new tax regime is the default unless you explicitly opt for the old one. The choice significantly impacts your monthly TDS.

| Income Slab | Tax Rate |

|---|---|

| Up to ₹3 lakh | Nil |

| ₹3 lakh – ₹7 lakh | 5% |

| ₹7 lakh – ₹10 lakh | 10% |

| ₹10 lakh – ₹12 lakh | 15% |

| ₹12 lakh – ₹15 lakh | 20% |

| Above ₹15 lakh | 30% |

Under the new regime, a ₹75,000 standard deduction is available for salaried employees. No HRA, no 80C, no 80D. The slabs are simpler, and for many people with fewer investments, it results in lower overall tax.

The old tax regime allows deductions under 80C (up to ₹1.5 lakh), 80D (health insurance), HRA exemption, LTA, and more. If you're paying rent, investing in ELSS or PPF, and have a home loan, the old regime often wins. As a general rule: if your total deductions exceed ₹3.75 lakh (at the ₹15 LPA level), the old regime typically saves more tax. Use CalcPhi's New vs Old Tax Regime Calculator to compare both at your exact income level.

How to Increase Your In-Hand Without a Salary Hike

Your take-home salary is not fixed just because your CTC is fixed. There are legal ways to restructure your salary to reduce tax and increase what lands in your account.

Request a Salary Restructuring

Most employers allow you to restructure your CTC components within limits. The following changes can add ₹5,000–₹12,000/month to your take-home without any actual salary increase:

Food or Meal Allowance — Up to ₹26,400 per year (₹2,200/month) is completely tax-exempt. If this isn't already a line item in your salary structure, ask HR to carve it out of your special allowance.

Mobile and Internet Reimbursement — If your role involves using your personal phone or internet, you can claim up to ₹1,200–₹1,500/month as a reimbursement (against actual bills), which is non-taxable.

Employer NPS Contribution — This is the single most underused salary benefit in India. Under Section 80CCD(2), your employer can contribute up to 10% of your basic salary to your NPS account. This amount is deductible from your taxable income and does not count against your ₹1.5 lakh 80C limit. On a ₹15 LPA salary (₹50,000 basic), that's ₹5,000/month or ₹60,000/year in additional tax-free savings. Your taxable income drops, TDS falls, and your in-hand rises — all while building your retirement corpus. Use CalcPhi's NPS Calculator to see how employer contributions build your pension corpus over time.

Declare All Your Investments Early

One of the most common mistakes salaried employees make is submitting investment proofs in March when TDS has already been deducted heavily for 11 months. Submit your proofs — rent receipts for HRA, insurance premium receipts for 80D, ELSS statements for 80C — as early as January every year. Your employer will reduce TDS proportionately, improving your monthly take-home for the remaining months.

Use HRA Exemption Correctly

If you live in a metro city and pay rent, the HRA exemption can significantly reduce your taxable income under the old regime. The exemption is the minimum of: actual HRA received, 50% of basic salary (metro) or 40% (non-metro), and actual rent paid minus 10% of basic salary. CalcPhi's HRA Calculator does the three-way comparison instantly and tells you exactly how much is exempt.

The Gratuity Trap: Why Switching Jobs Before 5 Years Costs You

This is one of the most financially damaging decisions salaried employees make without realising it. When your offer letter says ₹15 LPA and includes ₹28,860 in annual gratuity provision, that money only becomes yours after you complete five continuous years at the same employer.

If you switch jobs at 3.5 years — which is extremely common in India's IT and services sectors — you walk away with zero gratuity. Over 3.5 years, that's roughly ₹1.01 lakh in provisioned money you forfeit. At higher salary levels, this can be significantly more.

The lesson isn't "never switch jobs." It's: if you're at 4 years and 6 months, wait six more months. The gratuity payout for a ₹15 LPA employee completing exactly 5 years is approximately ₹1.44 lakh — and it's tax-exempt up to ₹20 lakh under the Income Tax Act. Calculate exactly how much you'd receive using CalcPhi's Gratuity Calculator.

A Real Example: ₹10 LPA vs ₹12 LPA Offer — Which Is Actually Better?

Imagine you're comparing two offers. Company A offers ₹10 LPA. Company B offers ₹12 LPA. Company B looks like a clear winner — ₹2 lakh more. But let's look at the structure.

Company A's ₹10 LPA includes: higher basic (45% of CTC), food allowance, fuel reimbursement, employer NPS contribution, and a smaller special allowance. Company B's ₹12 LPA has: lower basic (35% of CTC), no food allowance, no NPS, and a massive special allowance.

The result? Company A's in-hand can be ₹64,000–₹66,000/month. Company B's in-hand might be ₹70,000–₹72,000/month. Company B still wins — but by only ₹6,000/month, not ₹16,667/month as the headline CTC difference implies. Always ask for the salary structure — not just the CTC number — before accepting any offer.

What to Check Before Signing an Offer Letter

Before you sign, ask your HR or recruiter for the following in writing:

- The full salary breakup — basic, HRA, special allowance, and all other components listed separately

- Whether employer PF, gratuity, and insurance are included inside the stated CTC or over and above it

- The applicable professional tax slab for your state

- Whether the company offers a salary restructuring option (food allowance, NPS, phone reimbursement)

- The income tax regime that will be applied by default, and how to switch if you prefer the other

These five questions take five minutes to ask and can save you years of confusion.

Frequently Asked Questions

-

Is the employer's PF contribution included in my CTC?

Yes, in most cases. Employers typically include their 12% PF contribution (on your basic salary) within the quoted CTC figure. This money goes into your EPF account and belongs to you — but it is only accessible at retirement or on specific withdrawal conditions under the EPF Act. It is real savings, just locked and long-term.

-

What is the difference between gross salary and net salary?

Gross salary is the total of all your salary components (basic, HRA, allowances) before any deductions. Net salary — or take-home, or in-hand salary — is what remains after all deductions: employee PF, professional tax, TDS, and any other deductions like loan EMIs through payroll. The difference between gross and net is your total monthly deduction load.

-

How is TDS on salary calculated?

Your employer estimates your total annual taxable income at the start of the financial year, applies the applicable tax slabs, and divides the resulting tax liability by 12 to deduct it monthly. If you declare investments (under 80C, 80D, HRA, etc.), your estimated taxable income reduces, and so does your monthly TDS. The final tax liability is reconciled when you file your ITR.

-

Can I reduce my TDS legally?

Yes. The most effective legal methods are: opting for the tax regime that suits your income and investment profile, declaring all eligible investments and exemptions to your employer at the start of the year, claiming HRA if you pay rent, maximising employer NPS contributions under 80CCD(2), and including tax-exempt components like food allowance and mobile reimbursement in your salary structure.

-

Why does my colleague with the same CTC get more in-hand?

Because salary structures differ. Two people with the same CTC can have very different takes-home depending on how their salary is split across components, which tax regime they are on, what deductions they have declared, and which state they work in (affecting professional tax). The CTC number is the same; everything else can vary.

-

When should I prefer the old tax regime over the new one?

The old tax regime generally works better when your total deductions and exemptions exceed the tax advantage offered by the new regime's lower slabs. As a rough guide for AY 2026-27: if you are investing ₹1.5 lakh under 80C, paying rent (HRA exemption), paying health insurance premiums (80D), and have a home loan interest deduction — and your total deductions exceed ₹3.5–4 lakh — the old regime often results in lower tax. Use CalcPhi's New vs Old Tax Regime Calculator to compare both options at your exact income level.

The Bottom Line

Your offer letter isn't lying to make you feel richer. The CTC framework is a real accounting convention — employers genuinely spend that money on you. But the gap between what they spend and what you receive is real, predictable, and in many cases, reducible.

The smartest thing you can do right now is understand your own salary structure, restructure it where you can, choose the right tax regime, and declare your investments early. Small changes in how your CTC is structured can mean an extra ₹5,000–₹10,000 in your account every month — without a single rupee more from your employer.

Start by calculating your exact take-home using CalcPhi's CTC to In-Hand Calculator. It breaks down every component, applies the right tax slabs for AY 2026-27, and shows you exactly what your offer letter should have said in the first place.

Calculate your actual take-home salary:

CTC to In-Hand Calculator → Income Tax Calculator → New vs Old Regime → HRA Calculator →