Understanding Your Payslip: Every Line Item Decoded for Indian Employees

Your payslip arrives every month, but how many of us actually read it beyond the final take-home number? If you have ever stared at your salary slip wondering why your in-hand amount is so much less than your CTC, you are not alone. Most Indian employees receive a payslip with 10 to 15 line items and understand perhaps three of them. This guide decodes every single component — what it means, how it is calculated, and how it directly affects both your take-home pay and your tax liability.

What Is a Payslip and Why Does It Matter?

A payslip, also called a salary slip, is a formal document issued by your employer every month that details your earnings and deductions for that pay period. It is not just a record of what you were paid — it is a legally significant document. Banks ask for it when you apply for a home or personal loan, landlords request it as proof of income, and the Income Tax Department expects it to reconcile with the figures in your Form 16 at the end of the year.

More practically, your payslip determines how much TDS (Tax Deducted at Source) your employer cuts every month. TDS is income tax deducted in advance, directly from your salary, before the money reaches your bank account. If your payslip structure is inefficient, you may be paying more tax than necessary.

The Two Sides of Every Payslip: Earnings and Deductions

Every payslip is divided into two halves. On one side are your earnings — all the components that together form your gross salary. On the other side are your deductions — amounts subtracted from that gross figure. What remains after deductions is your net salary, commonly called your take-home or in-hand salary. Understanding both sides is essential because some earnings are partially or fully exempt from tax, and some deductions actually reduce your taxable income — saving you money.

Decoding the Earnings Side

Basic Salary

This is the foundation of your entire salary structure. Basic salary is typically 40% to 50% of your CTC (Cost to Company), though this varies by employer. It is fully taxable — there are no exemptions on basic salary. Everything else on your payslip is either calculated as a percentage of basic or added on top of it.

Your basic salary also determines several other components. Your EPF contribution is calculated on basic salary (plus DA). Your gratuity is calculated using basic salary. Your leave encashment is paid out at basic salary rate. So even though basic might look like just one line item, it quietly sets the floor for your entire compensation structure. Use CalcPhi's Gratuity Calculator to see exactly how your basic salary translates into your gratuity entitlement after years of service.

Dearness Allowance (DA)

DA is a cost-of-living adjustment primarily paid by government employers and public sector undertakings (PSUs). Most private sector companies in India do not pay DA, or if they do, it is a nominal amount. For government employees, DA is revised twice a year (in January and July) and is fully taxable. If you work for a private company and see no DA on your payslip, that is completely normal.

House Rent Allowance (HRA)

HRA is one of the most valuable tax-saving components on your payslip. Your employer pays you HRA as part of your salary — it appears as an earning. But if you live in a rented home and actually pay rent, a significant portion of that HRA is exempt from tax.

The exemption is calculated using a three-part formula, and you get whichever result is lowest: the actual HRA received; 50% of (basic + DA) for metro cities like Mumbai, Delhi, Chennai, and Kolkata or 40% for non-metro cities; and the actual rent paid minus 10% of basic salary. Use CalcPhi's HRA Calculator to find your exact exemption in seconds — just enter your salary figures and monthly rent.

If you live in your own home or do not pay rent, your entire HRA is taxable. If you are working from your hometown and paying rent to a family member, that arrangement needs to be carefully documented to withstand scrutiny.

Special Allowance

This is often the largest component after basic salary on private sector payslips. Special allowance is essentially a top-up that employers use to fill the gap between your basic + other allowances and your total CTC. It is entirely taxable — there is no exemption available on special allowance. When companies restructure salaries, they often adjust this component.

Leave Travel Allowance (LTA)

LTA is a component paid by your employer to cover the cost of domestic travel during leave. Only the actual travel cost (for the shortest air, rail, or road route) is exempt from tax, and only twice in a four-year block. The exemption covers economy airfare or first-class rail fare for you and your family. You must actually travel within India and submit bills to your employer to claim the exemption. LTA exemption is only available under the old tax regime.

Medical Allowance and Other Special Allowances

Many employers include a medical allowance, conveyance allowance, or telephone/internet allowance as separate line items. Medical reimbursement (up to ₹15,000/year when supported by bills) used to be tax-exempt but is now folded into the standard deduction. Conveyance and telephone allowances in the new tax regime are also folded in. The standard deduction for salaried employees for AY 2026-27 is ₹75,000, which replaces these individual exemptions under the new tax regime.

Bonus and Performance Pay

If your payslip for a particular month includes a variable component — a quarterly incentive, annual bonus, or performance pay — it appears as a separate earning line. This amount is fully taxable in the month it is paid, and your employer will typically deduct a higher TDS in that month to account for the increased income. CalcPhi's Bonus After Tax Calculator shows your net bonus after TDS so there are no surprises.

Decoding the Deductions Side

EPF (Employee Provident Fund)

EPF is a mandatory retirement savings scheme governed by the Employees' Provident Fund Organisation (EPFO). If your employer has 20 or more employees, EPF is compulsory. You contribute 12% of your basic salary (plus DA) towards EPF every month. Your employer also contributes 12% of your basic — but only 3.67% of that goes to your EPF account. The remaining 8.33% of the employer's contribution goes to the Employee Pension Scheme (EPS), which funds your monthly pension after retirement.

Your EPF contribution is deductible under Section 80C of the Income Tax Act, up to the overall ₹1.5 lakh annual limit. The interest earned on EPF is currently 8.25% per annum and is tax-free (subject to annual contribution limits). Use CalcPhi's EPF Calculator to project your provident fund corpus at the time of retirement based on your current basic salary.

Want to know exactly how your take-home salary is built from your CTC? Use CalcPhi's free CTC to In-Hand Salary Calculator — enter your CTC and get a complete breakdown of earnings, deductions, and net pay in seconds. No sign-up needed.

TDS (Tax Deducted at Source)

TDS is the income tax your employer deducts from your salary each month and deposits directly with the government on your behalf. At the end of the year, this shows up in Form 26AS and is reflected in your Form 16. When you file your ITR (Income Tax Return), you claim credit for all the TDS already deducted.

The amount of TDS depends on your estimated annual taxable income and which tax regime you have opted for — the old regime (with deductions like 80C, HRA, etc.) or the new regime (lower tax rates, fewer deductions). If you have not informed your employer which regime to use, they will default to the new tax regime for AY 2026-27. Use CalcPhi's TDS on Salary Calculator to verify whether your employer is cutting the right amount each month.

Professional Tax (PT)

Professional Tax is a state-level tax on employment, and the rules vary considerably across India. Maharashtra charges up to ₹200 per month (₹2,400 per year) for employees earning above ₹10,000 per month. Karnataka charges ₹200 per month for those earning above ₹24,000 per month. States like Delhi, Haryana, and Rajasthan do not levy professional tax at all. Use CalcPhi's Professional Tax Calculator to check your state's exact slab.

Professional tax is deductible from your taxable income under both the old and new tax regimes. It is deducted by your employer and deposited with the state government.

Loan and Advance Deductions

If you have taken a salary advance or a loan from your employer, the monthly repayment instalment appears as a deduction. These are not tax-related — they simply reduce your take-home for the month and do not appear in your Form 16.

Insurance Premium Deductions

Some employers offer group health insurance or term life insurance as part of the CTC. If the premium is structured as a deduction from your payslip (rather than being paid entirely by the employer), it will appear here. Employer-paid group health insurance premiums are considered a taxable perquisite (perk) in some structures — check with your HR if you are unsure how it is treated in your company's payroll.

Reading Your Payslip: A Practical Example

Let us take a salaried employee with a CTC of ₹12 LPA to see how all of this comes together.

Suppose the salary structure is: Basic Salary ₹40,000, HRA ₹20,000, Special Allowance ₹35,000, LTA ₹5,000. The gross monthly salary is ₹1,00,000 (₹12 LPA).

Deductions would include: EPF (Employee) at 12% of ₹40,000 = ₹4,800; TDS approximately ₹4,000 to ₹7,000 depending on regime and declared investments; and Professional Tax ₹200 (Maharashtra example).

Total deductions of approximately ₹9,000 to ₹12,000 leave an in-hand salary of ₹88,000 to ₹91,000 per month. This is why people often say their in-hand is about 70% to 80% of their CTC — PF, tax, gratuity provisioning, and insurance premiums all add up quickly.

For a personalised breakdown, use the CalcPhi Income Tax Calculator to see your exact tax liability under both the old and new regimes for AY 2026-27, then choose whichever results in lower tax.

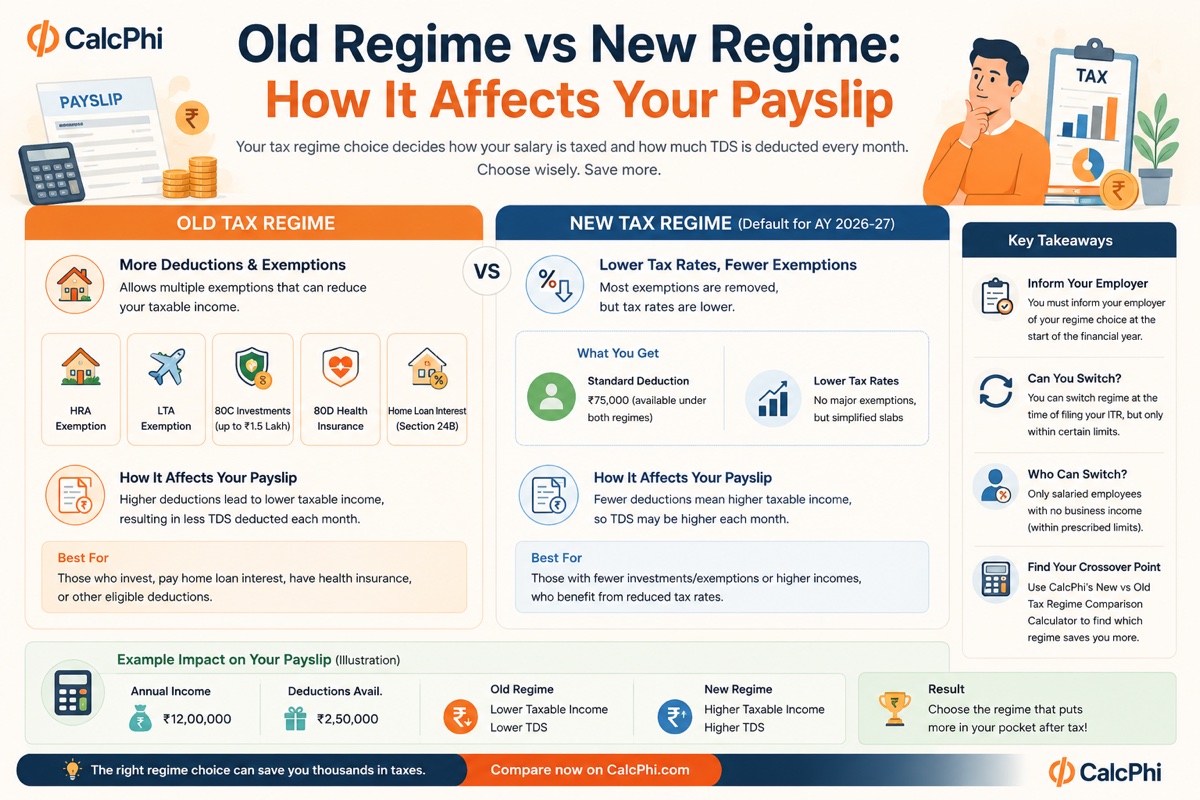

Old Regime vs New Regime: How It Affects Your Payslip

The tax regime you choose significantly changes how your payslip deductions work. Under the old regime, your employer can factor in HRA exemption, LTA, 80C investments (up to ₹1.5L), 80D health insurance premiums, and home loan interest (Section 24B) while calculating TDS. If you have these deductions, the old regime often results in less TDS each month.

Under the new regime (now the default for AY 2026-27), most of these exemptions disappear, but the tax rates are lower. The standard deduction of ₹75,000 is available under both regimes. To find your crossover point — the income level at which one regime becomes better than the other — use CalcPhi's New vs Old Tax Regime Comparison Calculator.

You must inform your employer of your regime choice at the start of the financial year, as it determines how much TDS they deduct each month. You can switch regime at the time of filing your ITR, but only within certain limits for salaried employees with no business income.

Common Mistakes Employees Make When Reading Payslips

Many employees do not inform their employer about their HRA rent details, resulting in the full HRA being taxed when a portion could have been exempt. Others forget to submit investment proofs (for 80C, 80D, and home loan) to HR by the deadline — usually January or February — leading to a surge in TDS in the last quarter of the year. Some employees also confuse the employer's EPF contribution (which is not part of their take-home) with their own contribution when calculating savings.

If your payslip has a component labelled "Employer's PF" or "Employer's ESI contribution" listed separately, those are costs to the company and may not appear in your actual monthly deductions — they are included in your CTC figure but paid directly by the employer. Related reading: CTC vs In-Hand Salary: Why Your Offer Letter Is Lying to You and TDS on Salary and Form 16: How to Read Your Tax Certificate.

Frequently Asked Questions

Why is my in-hand salary so much less than my CTC?

CTC (Cost to Company) includes everything your employer spends on you — your basic salary, HRA, all allowances, employer's share of PF, gratuity provisioning, insurance premiums, and sometimes even office amenities. Only a portion of this reaches your bank account. The difference is made up of employee PF contributions, TDS, professional tax, and other deductions. A ₹12 LPA CTC typically translates to ₹85,000 to ₹92,000 in-hand per month.

Is HRA on my payslip automatically tax-free?

No. HRA appears as an earning and is technically taxable. It becomes partially exempt only if you actually live in a rented home and pay rent. The exempt amount is calculated using a specific formula involving your basic salary, the HRA received, and your actual rent. If you do not declare your rent to your employer, the full HRA is included in your taxable income.

What is the difference between TDS and income tax?

TDS is the mechanism — income tax deducted at source by your employer and deposited with the government on your behalf, month by month. Income tax is the overall liability calculated on your full year's income. At the time of ITR filing, if TDS was more than your actual tax liability, you get a refund. If it was less, you pay the balance.

Can I change my tax regime after my employer has already been deducting TDS under one regime?

Yes, you can switch regimes when filing your ITR. However, if you switch late in the year, the TDS your employer deducted under the original regime will still be credited — you just reconcile at filing. Salaried employees with no business income can switch regimes freely every year. Those with business income can only switch once.

What does "gross salary" on my payslip mean?

Gross salary is the total of all your earnings before any deductions. It is your basic salary plus HRA plus all allowances plus any bonus for that month. This is different from your CTC (which includes the employer's costs) and from your net or in-hand salary (which is after deductions).

Why does my TDS deduction change from month to month?

Your employer estimates your full-year tax liability at the start of the year and divides it across 12 months. If you receive a bonus, submit investment proofs late, or change your regime declaration mid-year, the employer recalculates and adjusts TDS for the remaining months — which can cause it to spike in January, February, and March.

Disclaimer: The information in this article is for educational and estimation purposes only. Tax laws, EPF rates, and salary structuring rules are subject to change. Nothing in this article constitutes personalised financial or tax advice. Please consult a qualified Chartered Accountant or SEBI-registered financial advisor for guidance specific to your situation.