Section 80D: How to Maximise Your Health Insurance Tax Deduction in 2026

Most salaried Indians claim just ₹25,000 under Section 80D and stop there. They buy a basic health insurance plan, enter the premium in their ITR, and move on. What they miss is the second deduction — the one for parents — which can add another ₹25,000 to ₹50,000 in deductions depending on their parents' age. At the 30% tax bracket, that missed deduction costs you over ₹15,000 every single year.

Section 80D is one of the few tax deductions in India that rewards you for doing something genuinely useful: protecting your family's health. Understanding how to claim it fully — and correctly — can mean saving anywhere from ₹7,800 to ₹31,200 a year in tax, depending on your income and family situation. This guide covers every limit, every category, every exception, and every real-world scenario you need to know for FY 2025-26 (AY 2026-27).

What Is Section 80D and Who Can Claim It?

Section 80D of the Income Tax Act, 1961 allows individuals and Hindu Undivided Families (HUFs) to claim a deduction on the premiums paid for health insurance policies. The deduction applies to premiums paid for yourself, your spouse, your dependent children, and your parents.

The key word here is "individual." Companies and firms cannot claim 80D. If you are a salaried employee, a freelancer, a business owner taxed as an individual, or a self-employed professional, you are eligible. HUFs can also claim this deduction for their members.

One critical point: Section 80D is available only if you opt for the old tax regime. Under the new tax regime (which became the default from FY 2024-25), you cannot claim this deduction at all. If you have senior citizen parents and are paying significant health insurance premiums, this is one of the most important factors to weigh when comparing regimes. Use CalcPhi's New vs Old Tax Regime Calculator to see exactly which regime saves you more after factoring in 80D.

Section 80D Deduction Limits for FY 2025-26

The deduction limits are split into two buckets: one for your own family (self, spouse, and dependent children) and one for your parents. These two buckets are completely separate and can be claimed simultaneously.

| Who Is Insured | Their Age | Maximum Deduction |

|---|---|---|

| Self, spouse, dependent children | Below 60 | ₹25,000 |

| Self, spouse, dependent children | 60 or above (senior citizen) | ₹50,000 |

| Parents | Below 60 | ₹25,000 |

| Parents | 60 or above (senior citizen) | ₹50,000 |

| Maximum combined deduction | ₹1,00,000 |

The maximum of ₹1,00,000 is achievable only when the policyholder themselves is a senior citizen AND their parents are also senior citizens above 60. For most people in their 30s and 40s with elderly parents, the realistic maximum is ₹75,000 — ₹25,000 for self and ₹50,000 for senior citizen parents.

Within each bucket, there is also a sub-limit of ₹5,000 for preventive health check-up expenses (explained in detail below).

The Four Scenarios That Determine Your Actual Deduction

Understanding the limits in a table is one thing. Knowing how much you can actually claim — based on your real situation — is what matters.

Scenario 1: You Are Below 60, Parents Are Also Below 60

You pay ₹18,000 as your health insurance premium and ₹20,000 for your parents' policy.

- Self + family deduction: ₹18,000 (actual premium, within ₹25,000 cap)

- Parents' deduction: ₹20,000 (actual premium, within ₹25,000 cap)

- Total deduction: ₹38,000

Tax saved at 20% slab (+ 4% cess): ₹7,904. Tax saved at 30% slab (+ 4% cess): ₹11,856.

Scenario 2: You Are Below 60, Parents Are Senior Citizens (60+)

This is the most common situation for people aged 30–45. You pay ₹22,000 for your own family floater and ₹40,000 for your parents' senior citizen health plan.

- Self + family deduction: ₹22,000 (within ₹25,000 cap)

- Parents' deduction: ₹40,000 (within ₹50,000 cap for senior citizens)

- Total deduction: ₹62,000

Tax saved at 30% slab (+ 4% cess): ₹19,344. That is nearly ₹20,000 back in your pocket just from keeping both policies active.

Scenario 3: You Are a Senior Citizen (60+) and Your Parents Are Also 60+

- Self + family deduction: up to ₹50,000

- Parents' deduction: up to ₹50,000

- Maximum total deduction: ₹1,00,000

Tax saved at 30% slab (+ 4% cess): ₹31,200.

Scenario 4: Your Parents Have No Insurance But Are Senior Citizens

Even if your parents are not covered under any health policy, you can still claim up to ₹5,000 for their preventive health check-up expenses — carved out from within the ₹50,000 senior citizen limit. However, if they have no insurance and no check-up expenses, there is no deduction to claim for the parents' bucket.

Want to calculate your exact 80D savings in seconds? Use CalcPhi's free Section 80D Calculator — enter your premium, your parents' age and premium, and it shows you the precise deduction and tax saved.

The ₹5,000 Preventive Health Check-Up Deduction

Within the main deduction limit, ₹5,000 can be claimed specifically for preventive health check-up expenses. This sub-limit applies to the entire family — yourself, spouse, children, and parents — and is carved out from within the ₹25,000 or ₹50,000 cap, not over and above it.

The unique advantage of this sub-limit is that it can be paid in cash. All other health insurance premium payments under 80D must be made through non-cash modes — bank transfer, cheque, UPI, debit card, or credit card. Cash premium payments are explicitly disqualified. But for preventive check-up expenses specifically, the Income Tax Act allows cash payment, making it accessible even for those who may not have digital payment records.

To claim this, keep receipts from any annual health check-up, blood tests, health screening packages, or diagnostic tests you underwent during the financial year. You do not need to be insured to claim this — it is available independently.

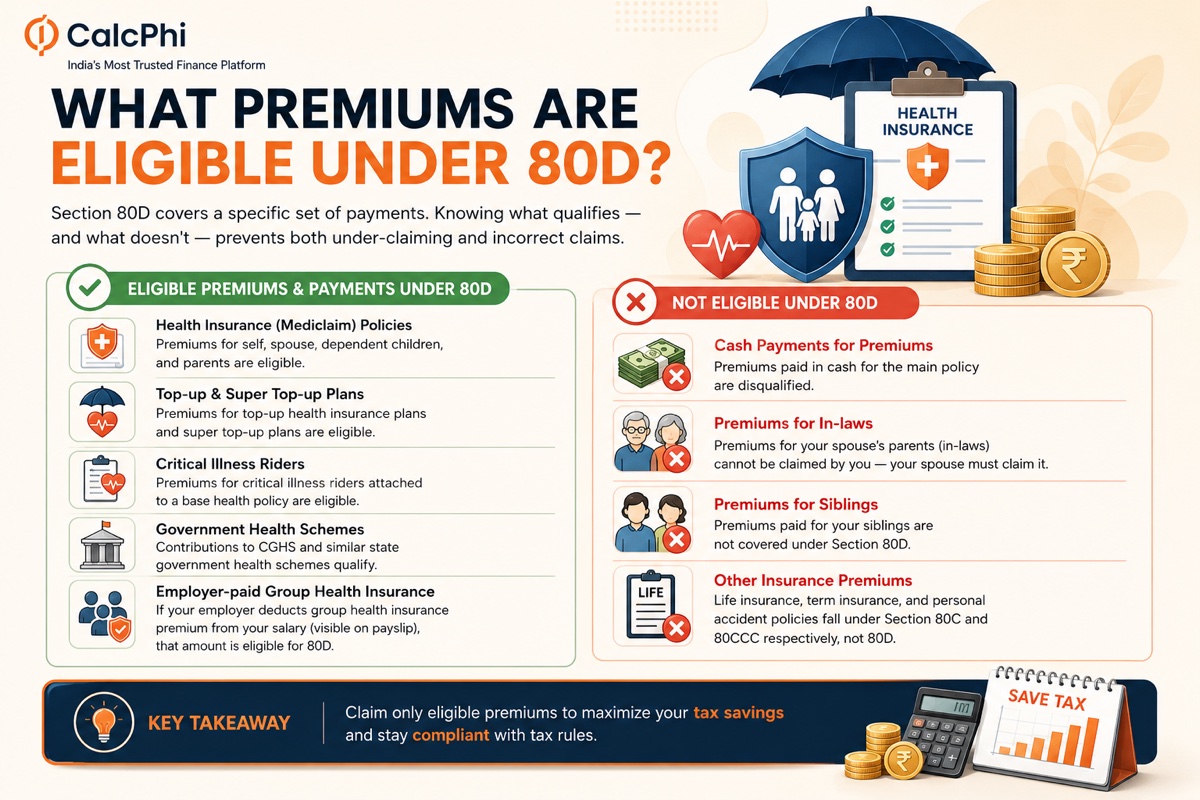

What Premiums Are Eligible Under 80D?

Section 80D covers a specific set of payments. Knowing what qualifies — and what doesn't — prevents both under-claiming and incorrect claims.

Eligible premiums and payments: Health insurance (mediclaim) policies for self, spouse, dependent children, and parents are the core of 80D. Top-up health insurance plans, super top-up plans, and critical illness riders attached to a base health policy are all eligible. Contributions to the Central Government Health Scheme (CGHS) and similar state government health schemes also qualify. If your employer deducts group health insurance premium from your salary (visible on your payslip), that amount is eligible for 80D — many employees miss this.

Not eligible under 80D: Premiums paid in cash for the main policy are disqualified. Premiums for in-laws (your spouse's parents) cannot be claimed by you — your spouse must claim it. Premiums for siblings are not covered. Life insurance premiums, term insurance premiums, and personal accident policies fall under Section 80C and 80CCC respectively, not 80D.

Multi-Year Policies: How to Claim Deductions

Health insurers in India increasingly offer multi-year policies — two-year or three-year plans — often at a discount. If you pay a lump sum premium for a multi-year policy, the deduction must be spread proportionately across the policy years.

For example, if you pay ₹60,000 for a three-year health policy in FY 2025-26, you cannot claim the full ₹60,000 this year. You claim ₹20,000 per year over three years (subject to the annual cap of ₹25,000 or ₹50,000). This proportionate rule was clarified by the CBDT and applies regardless of when the premium is paid. Keep this in mind when buying multi-year plans — the tax benefit is the same in total, just spread out differently year by year.

80D and the Old vs New Tax Regime Decision

The single most important context for Section 80D in 2026 is the tax regime choice. The new tax regime — now the default — removes most deductions including 80D, 80C, and HRA. In exchange, it offers lower slab rates. Whether you come out ahead depends entirely on your deduction profile.

Here is a simplified comparison for someone earning ₹12 lakh per year:

| Item | Old Regime | New Regime |

|---|---|---|

| Gross salary | ₹12,00,000 | ₹12,00,000 |

| Standard deduction | ₹75,000 | ₹75,000 |

| Section 80C | ₹1,50,000 | Not available |

| Section 80D (self + senior citizen parents) | ₹75,000 | Not available |

| Taxable income | ₹9,00,000 | ₹11,25,000 |

| Tax payable (approx., incl. cess) | ~₹93,600 | ~₹1,05,300 |

| Old regime saves | ~₹11,700 annually | |

If your parents are younger and the parent premium is only ₹25,000, run the numbers again — the crossover point shifts. Use CalcPhi's Income Tax Calculator to compute your tax under both regimes with your actual income and deductions, and then check the New vs Old Tax Regime Calculator for a side-by-side comparison that factors in 80D automatically.

How to Claim 80D While Filing Your ITR

Claiming 80D is straightforward when you have the right documents in hand. The premium payment receipts from your insurer are the primary document. For digital payments, a bank statement or UPI confirmation is sufficient. If your employer deducts group health insurance from your salary, your Form 16 Part B or salary slip will show the amount — quote that figure in your ITR.

In your ITR (most salaried employees file ITR-1 or ITR-2), Section 80D appears under Chapter VI-A deductions. You will be asked to enter: the premium paid for self and family, the premium paid for parents, and the preventive check-up amount separately. Ensure you also indicate whether your parents are senior citizens (60+), as this determines the applicable cap.

You do not need to submit these receipts with your ITR — they are self-declared. However, you must retain them for at least six years in case of a scrutiny notice from the Income Tax Department.

Seven Practical Tips to Maximise Your 80D Deduction

Buy a separate policy for your parents, not a family floater. Adding senior citizen parents to a family floater dramatically increases the premium for all members. A standalone senior citizen plan for parents often costs less overall and keeps your own policy renewal simpler.

Pay all premiums through non-cash modes. UPI, net banking, cheque, or debit/credit card — all qualify. Cash payments for the main premium are explicitly ineligible, so even if the insurer accepts cash, avoid it to protect your deduction.

Check whether your employer's group health insurance premium is in your payslip. Many employees overlook this. If your employer deducts even ₹8,000–₹12,000 annually for a group policy, that amount contributes toward your ₹25,000 80D limit.

Don't forget preventive check-up receipts. Even if you only spent ₹2,000 on an annual health check-up at a diagnostic centre, keep the receipt. It reduces your taxable income and can be paid in cash.

Review your parents' policy sum insured. Medical inflation in India runs at 12–15% annually. A ₹3 lakh policy bought five years ago may not cover even a single hospitalisation today. Increasing the sum insured increases the premium — which also increases your 80D deduction, provided it stays within the ₹25,000 or ₹50,000 cap.

Consider a top-up or super top-up policy for yourself. These are inexpensive (often ₹5,000–₹8,000 annually for a ₹20 lakh deductible-based top-up) and the premium is eligible for 80D. Combined with a base plan, this helps you claim closer to the full ₹25,000 limit.

If you are approaching the parent premium cap, be aware of the ceiling. If your parent policy premium is ₹52,000 for the year, you can only claim ₹50,000. There is no flexibility on the cap, but being aware prevents surprise under-deductions.

To estimate your ideal coverage before buying, try CalcPhi's Health Insurance Calculator — it recommends the right sum insured for your family size, age, and city tier.

How 80D Interacts With Section 80C

Section 80D and Section 80C are entirely separate deductions. Claiming 80D does not reduce your 80C limit, and vice versa. The ₹1,50,000 limit under 80C (for PPF, ELSS, EPF, LIC, etc.) is independent of the ₹25,000–₹1,00,000 available under 80D.

This means a taxpayer in the 30% bracket with a senior citizen parent can potentially claim:

- ₹1,50,000 under 80C (ELSS, PPF, LIC, EPF)

- ₹75,000 under 80D (₹25,000 self + ₹50,000 senior citizen parents)

- ₹75,000 standard deduction (salaried)

- Total deductions: ₹3,00,000

At ₹12 lakh gross salary, that brings taxable income to ₹9 lakh, with a substantial tax saving over the new regime. Use CalcPhi's Section 80C Calculator to see how much of the ₹1.5 lakh 80C limit you are already filling — and where the gaps are.

Frequently Asked Questions

-

Can I claim 80D if my parents are not financially dependent on me?

Yes. Unlike some deductions that require dependency, Section 80D allows you to claim the parents' bucket as long as you are paying the premium — regardless of whether your parents are financially dependent on you. The only conditions are that you pay the premium (not them) and that it is paid through non-cash modes.

-

What happens if both me and my sibling contribute to our parents' health insurance premium?

Only the person who actually pays the premium can claim the deduction. If you split the premium with your sibling, only the person paying can claim their respective portion. If the premium is paid from a joint account or only one person pays, the deduction goes to the payer. There is no provision to split the deduction between siblings.

-

Can I claim 80D for health insurance premium paid by credit card?

Yes. Credit card payments are non-cash modes and are explicitly eligible for the 80D deduction. Debit cards, UPI, NEFT, IMPS, cheques, and demand drafts all qualify. The payment must be traceable — which a credit card statement provides.

-

Is the premium for a group health insurance policy offered by my employer eligible for 80D?

Yes, but only the portion of the premium that is actually deducted from your salary. If your employer pays the full premium as a benefit without any salary deduction, you cannot claim it (it was never your payment). If a portion is deducted from your salary — even partially — that amount is your payment and eligible for 80D. Check your payslip under deductions.

-

What if my health insurance premium exceeds the 80D cap?

You can only claim up to the applicable cap — ₹25,000 or ₹50,000 per bucket. Any premium above the cap is not deductible under 80D and cannot be carried forward or claimed under any other section. This does happen with senior citizen policies where premiums can reach ₹60,000–₹80,000 annually — the excess is simply not deductible.

-

Can an NRI claim Section 80D?

Yes. Non-Resident Indians (NRIs) who file taxes in India can claim Section 80D for health insurance premiums paid for themselves, their spouse, children, and parents — provided the premium is paid from a bank account in India and the policy is with an IRDAI-approved insurer. NRIs on the new tax regime cannot claim it, same as resident Indians.

Calculate your Section 80D deduction and compare tax regimes:

Section 80D Calculator → New vs Old Regime → Income Tax Calculator → Section 80C Calculator →