HUF Tax Benefits India 2026: How a Hindu Undivided Family Reduces Your Tax

An HUF is not a loophole — it is a distinct legal and taxable person under Section 2(31) of the Income Tax Act, 1961. It has its own PAN, files its own ITR, and is assessed separately from its members. For families with ancestral property, inherited investments, or a family business, this separation creates a second tax slab ladder — which can save ₹1–3 lakh per year depending on HUF income. For purely salaried families with no ancestral assets, the benefit is minimal. This article explains exactly how HUF taxation works for FY 2025-26 (AY 2026-27), what changed with Budget 2025's revised new regime slabs, and the one critical misconception about HUF and Section 87A that can lead to underpayment of tax. To see your own tax under both regimes, use CalcPhi's New vs Old Regime Calculator.

Key facts about HUF taxation (FY 2025-26)

- HUF is a separate taxable entity — it gets its own basic exemption, its own tax slabs, and files its own ITR.

- Under the new tax regime (default), HUF basic exemption is ₹4,00,000 (not ₹3L — slabs revised in Budget 2025).

- HUF does not get the Section 87A rebate — an individual earning ₹12L pays zero tax under the new regime; an HUF earning ₹12L pays ₹62,400.

- Salary income cannot be shifted to an HUF. Income splitting only works for genuine HUF income: ancestral property rent, inherited investments, gifts from non-member relatives.

- Daughters are full HUF coparceners since 2005 — the Supreme Court confirmed this retroactively in 2020 (Vineeta Sharma case).

- HUF cannot open a new PPF account — banned since May 2005. ELSS, LIC premiums for members, NSC, and 5-year FDs remain available under Section 80C (old regime only).

What Is an HUF and Who Can Form One?

A Hindu Undivided Family comprises all persons lineally descended from a common ancestor, along with their spouses and unmarried daughters. The entity exists as long as two or more coparceners are alive and undivided. Hindus, Sikhs, Jains, and Buddhists can form HUFs under Indian tax law — the Income Tax Act applies equally to all four communities.

The Karta is the head and manager of the HUF — traditionally the eldest male coparcener, though courts have upheld female Kartas after the 2005 Hindu Succession Amendment Act made daughters full coparceners by birth. A family with only daughters can form a valid HUF.

To set one up: draft an HUF deed on ₹100 stamp paper (get it notarised), apply for a HUF PAN via Form 49A on the Protean/NSDL portal (₹107, typically issued in 15–20 days), open an HUF bank account (SBI, HDFC, ICICI, and most major banks support these), and start directing genuine HUF income into the HUF's accounts. The HUF's corpus grows from there through reinvestment of its own income.

How HUF Income Splitting Actually Works

The tax benefit comes from the fact that HUF income is assessed at HUF slab rates, completely separate from your individual income. If your individual income is already in the 30% slab, any additional income you personally receive is also taxed at 30%. But if that same additional income legitimately belongs to the HUF, it enters its own tax table — starting from ₹0 — and sits in the nil or 5% slab if the HUF's total income is modest.

Income that can legitimately belong to an HUF:

- Ancestral property income — rent, interest, or capital gains from property inherited from ancestors. This is the cleanest HUF income — no clubbing provisions apply.

- Gifts from non-member relatives — gifts to the HUF from people who are not HUF members (the Karta's parents, siblings, grandparents) are not clubbed back to any individual. This is a legitimate way to build HUF corpus.

- Business income — a family business operated in the HUF's name, using HUF capital.

- Reinvested HUF income — returns on investments made from HUF corpus.

What cannot be shifted to HUF (Section 64 clubbing applies):

- Salary — inherently personal, can never be diverted.

- Income from your self-acquired property transferred without fair market value consideration — Section 64(2) clubs it straight back to you.

The Numbers: What HUF Saves on Rental Income

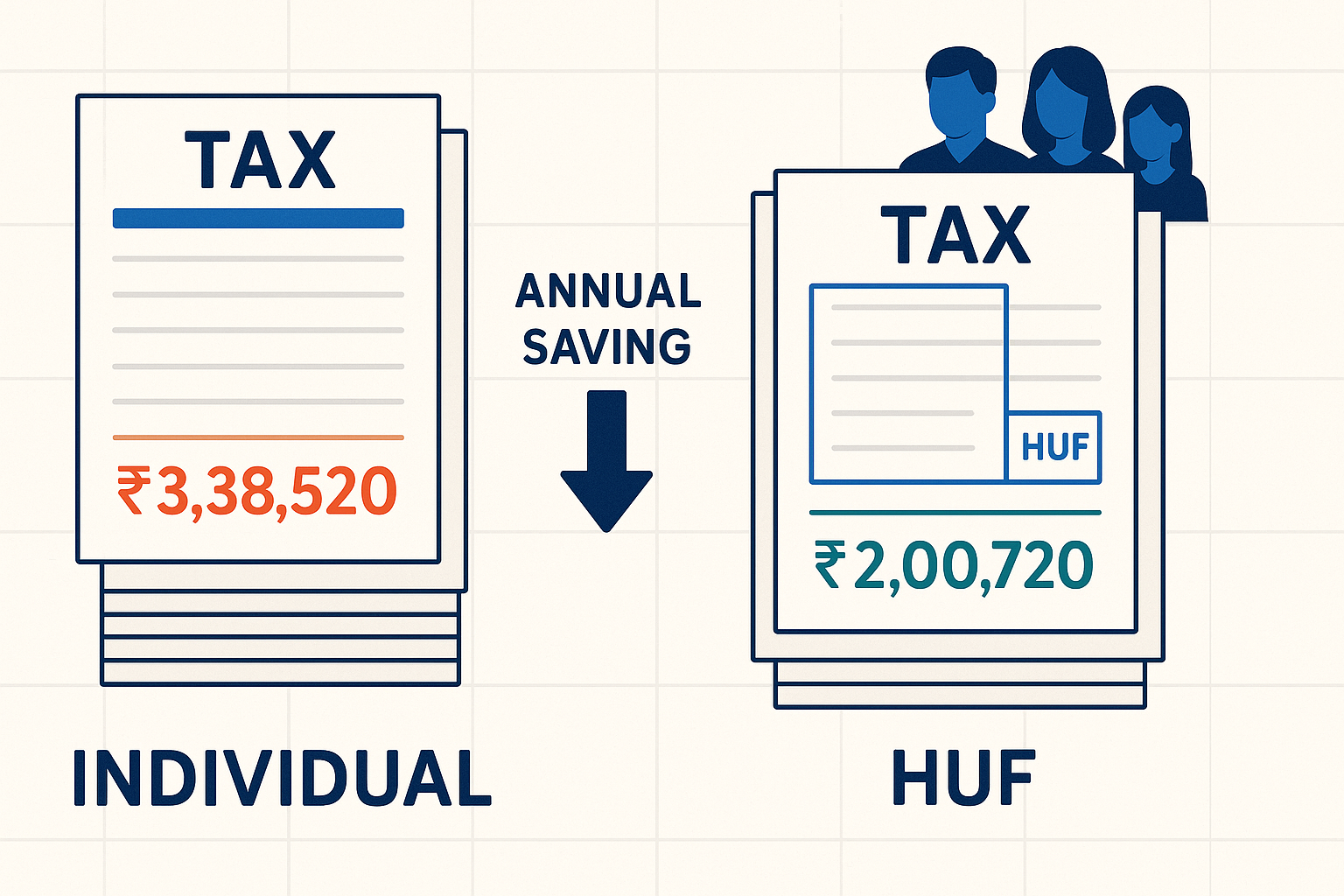

Consider Ramesh, 42, an IT professional in Bengaluru. His salary is ₹20 lakh/year. He also receives ₹8 lakh annual rent from a shop premises he inherited from his grandfather. That ancestral property income legitimately belongs to an HUF.

| Scenario | Individual tax | HUF tax | Total family tax |

|---|---|---|---|

| Without HUF (all income in Ramesh's hands) | ₹3,38,520 (on ₹24.85L taxable) | — | ₹3,38,520 |

| With HUF (rental income taxed in HUF) | ₹1,92,400 (on ₹19.25L salary) | ₹8,320 (on ₹5.6L net rental) | ₹2,00,720 |

| Annual tax saving with HUF | ₹1,37,800 | ||

Notes: Rental income of ₹8L less 30% standard deduction = ₹5.6L net. New regime slabs for FY 2025-26 as amended by Finance Act 2025. No surcharge (income under ₹50L). 4% health and education cess applied.

The saving comes from one mechanism: ₹5.6L of net rental income that would have been taxed at Ramesh's marginal rate of 20–25% in his individual hands is instead taxed at the HUF's starting rate of 0–5%. The HUF does not reduce Ramesh's salary tax — only the genuinely bifurcated income benefits.

HUF Deductions: Old Regime vs New Regime

The new tax regime is the default for HUFs from AY 2024-25 onward (Section 115BAC as amended by Finance Act 2023). Under the new regime, most deductions are gone. Under the old regime, a meaningful set remains.

| Deduction | New regime (default) | Old regime | Notes |

|---|---|---|---|

| Basic exemption | ₹4,00,000 | ₹2,50,000 | Budget 2025 revised new regime nil threshold to ₹4L |

| Section 87A rebate | Not available | Not available | HUF cannot claim — individuals only |

| Section 80C (ELSS, LIC, NSC, FD) | Not available | Up to ₹1,50,000 | PPF banned for HUF since May 2005 |

| Section 80D (health insurance) | Not available | Up to ₹25,000–₹50,000 | Premiums for HUF members |

| Section 24(b) home loan interest | Not available (self-occupied) | Up to ₹2,00,000 | For HUF-owned self-occupied property |

| Section 24(a) rental standard deduction | Available (30%) | Available (30%) | Available in both regimes on rental income |

| Capital gains exemptions (54, 54F, 54EC) | Available | Available | Same as individual rules |

| LTCG equity exemption (₹1.25L) | Available | Available | HUF gets its own ₹1.25L annual exemption, separate from members' |

When the old regime is better for an HUF: when the HUF can claim significant 80C (e.g., ₹1.5L in ELSS + LIC premiums for members), 80D, and home loan interest that collectively exceed the tax differential between the regimes. To opt for the old regime, file Form 10-IEA before the ITR due date. For a full breakdown of the regime choice for individuals (which parallels the HUF decision), see Old vs New Tax Regime: Complete Comparison. The 80C options available in the old regime are covered in detail in How to Maximise Section 80C.

One HUF Benefit the New Regime Preserves: The Dual LTCG Exemption

If the HUF holds equity mutual funds or listed shares in its own demat account, it gets a separate ₹1,25,000 annual LTCG exemption under Section 112A — completely independent of the exemptions available to individual members. A family where the individual + HUF both hold equity positions can together realise ₹2.5 lakh in LTCG per year tax-free. At 12.5% LTCG rate, this is a ₹31,250 annual tax saving — with no deductions lost and no old-regime requirement. This benefit works in the new regime.

Is HUF Right for You? A Decision Framework

HUF is worth forming if at least one of these applies:

- You receive rental income from ancestral property — that income is clean HUF income with no clubbing risk.

- Your family has received significant gifts from non-member relatives (e.g., parental gifts to the HUF) that can form a corpus generating investment income.

- The family holds shares or mutual funds in the HUF's name and wants the separate ₹1.25L LTCG exemption every year.

- You operate a family business where multiple coparceners contribute — a properly structured HUF business can split profits within the entity at lower effective rates.

HUF is not worth forming if:

- Your family is purely salaried with no ancestral property, no inherited assets, and no gifts from outside the family.

- The additional compliance cost (two ITRs, separate books of accounts, HUF bank account management) is not offset by the tax saving.

- You are considering transferring your self-acquired flat to HUF — Section 64(2) will club the rental income back to you anyway.

For families where HUF does apply, run the actual numbers before deciding old vs new regime for the HUF — CalcPhi's New vs Old Regime Calculator can help, and for projecting investment returns within the HUF corpus, the SIP Calculator shows compounding over time.

Compare your family's tax under old and new regimes — as both individual and HUF — with specific numbers:

New vs Old Regime Calculator →Frequently Asked Questions

-

Can a HUF save tax if I am salaried with no ancestral property?

Minimally. Salary cannot be diverted to an HUF under any circumstances — it is inherently personal income. Without ancestral property, inherited assets, or genuine gifts from non-member relatives, an HUF has no independent income source to shift. In such cases, the HUF adds compliance costs (separate PAN, separate ITR filing) without meaningful tax savings. HUF works best for families with rental income from ancestral property or inherited investments.

-

Does an HUF get the ₹12 lakh zero-tax benefit like individuals under the new regime?

No. The ₹12 lakh zero-tax threshold for individuals relies on Section 87A rebate (₹60,000 for FY 2025-26). HUF is not eligible for Section 87A — the rebate is available only to resident individuals. An HUF earning ₹12 lakh under the new tax regime pays ₹62,400 in tax (including 4% cess). This is one of the few areas where an individual tax profile is better than an HUF's, and it is frequently misstated in older articles.

-

Can daughters form or be part of an HUF?

Yes. The Hindu Succession (Amendment) Act 2005 made daughters full coparceners by birth, equal to sons. The Supreme Court confirmed in Vineeta Sharma v. Rakesh Sharma (2020) that this applies even to daughters born before 2005. Daughters can demand partition, alienate their share, and courts have upheld female Kartas where the daughter is the senior-most coparcener. A family with only daughters can form a valid HUF.

-

Can I transfer my flat to my HUF to save tax on rental income?

If it is ancestral property — yes, rental income is legitimately HUF income and there is no clubbing. If it is your self-acquired flat (purchased from your own savings), transferring it to the HUF without fair market value payment triggers Section 64(2) clubbing — the rental income continues to be taxed in your individual hands, defeating the purpose. The only clean route is to sell the property at fair market value to the HUF (which creates capital gains implications) or not transfer at all.

-

Which ITR form does an HUF file?

ITR-2 if the HUF has income from house property, capital gains, or other sources — but no business or profession income. ITR-3 if the HUF carries on a business or profession. ITR-4 (Sugam) if the HUF opts for presumptive taxation under Section 44AD and income is under ₹50 lakh. HUFs cannot file ITR-1 (Sahaj), which is exclusively for individual resident taxpayers.

-

Can an HUF invest in PPF to claim Section 80C deduction?

No. A Ministry of Finance notification dated 13 May 2005 prohibited HUFs from opening new PPF accounts. HUF PPF accounts opened before that date are grandfathered and can continue to maturity, but no new HUF PPF accounts are permitted. For 80C (old regime only), an HUF can invest in ELSS mutual funds, life insurance premiums for members, NSC, 5-year tax-saving FDs, and principal repayment on HUF housing loans. Sukanya Samriddhi Yojana (daughters only) and EPF (salary-based) are also not available to HUFs.

Disclaimer: The information in this article is for educational and informational purposes only. Tax rules cited are based on Income Tax Act, 1961 provisions and Finance Act 2025 amendments applicable for FY 2025-26 (AY 2026-27) and may change in future budgets or through CBDT circulars. The tax calculations shown are illustrative — actual liability depends on individual circumstances, income sources, deductions claimed, and applicable surcharge. Nothing in this article constitutes personalised tax or financial advice. Please consult a SEBI-registered investment advisor or a qualified Chartered Accountant before making tax or investment decisions. HUF formation involves legal documentation — consult a CA or legal professional before proceeding.