ITR Filing Guide for Salaried Employees: AY 2026-27

Filing your Income Tax Return (ITR) for AY 2026-27 is more taxpayer-friendly than ever — the new default tax regime makes zero tax effective up to ₹12.75 lakh gross salary, ITR-1 now covers two house properties and LTCG up to ₹1.25 lakh, and the e-filing portal pre-fills most of your data automatically. The deadline is 31 July 2026. This guide walks you through everything — ITR form selection, income tax slabs, eligible deductions, step-by-step filing, and common mistakes to avoid.

What is ITR Filing and Why is it Important?

An Income Tax Return (ITR) is a formal statement filed with the Income Tax Department declaring your income earned during a financial year, the taxes paid on it, and any refund due to you. For salaried employees, filing is not just a legal obligation under Section 139 of the Income Tax Act, 1961 — it also serves multiple practical purposes.

- Acts as legal proof of income for visa applications, loan approvals, and credit cards

- Enables you to claim refunds on excess Tax Deducted at Source (TDS)

- Allows carry-forward of losses (capital losses, business losses) to future years

- Helps avoid penalties under Section 234F and interest under Sections 234A, 234B, and 234C

- Builds a clean financial track record for future investments

If your gross total income exceeds the basic exemption limit — ₹4 lakh under the new tax regime or ₹2.5 lakh under the old tax regime for FY 2025-26 — filing your ITR is mandatory, regardless of whether your employer has already deducted TDS.

Key Updates for AY 2026-27 Every Salaried Employee Should Know

The CBDT notified the ITR forms for AY 2026-27 on 31 March 2026, well in advance of the filing season. Six changes are especially important for salaried taxpayers:

1. Two House Properties Now Allowed in ITR-1

Earlier, owning more than one house property pushed taxpayers into the more complex ITR-2. From AY 2026-27, salaried individuals can now report income from up to two house properties while still using the simpler ITR-1 (Sahaj) form.

2. LTCG up to ₹1.25 Lakh Allowed in ITR-1

Previously, any capital gains required filing ITR-2. Now, salaried taxpayers with Long-Term Capital Gains (LTCG) under Section 112A of up to ₹1,25,000 can continue to use ITR-1, provided there are no carry-forward losses.

3. Standard Deduction of ₹75,000 Continues

Salaried employees and pensioners opting for the new tax regime continue to enjoy the enhanced standard deduction of ₹75,000. Those choosing the old regime get ₹50,000.

4. Section 87A Rebate of up to ₹60,000

Under the new tax regime, taxable income up to ₹12 lakh attracts zero tax liability thanks to a rebate of up to ₹60,000 under Section 87A. Factoring in the ₹75,000 standard deduction, gross salary up to ₹12.75 lakh becomes effectively tax-free.

5. Drop-Down Menu for Deductions

To improve transparency and reduce false claims, deductions under Sections 80C to 80U must now be selected from a drop-down menu in the e-filing portal, with the exact clause/sub-section specified.

6. Aadhaar Number Mandatory

The 28-digit Aadhaar Enrolment ID is no longer accepted. Only a valid 12-digit Aadhaar number can be entered.

Income Tax Slabs for FY 2025-26 (AY 2026-27)

New Tax Regime (Default) — Section 115BAC

| Income Slab | Tax Rate |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Section 87A rebate: Up to ₹60,000 — making taxable income up to ₹12 lakh tax-free.

Old Tax Regime

| Income Slab | Tax Rate |

|---|---|

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 to ₹5,00,000 | 5% |

| ₹5,00,001 to ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Section 87A rebate: Up to ₹12,500 — making taxable income up to ₹5 lakh tax-free. A Health and Education Cess of 4% applies on income tax under both regimes. Use the Income Tax Calculator to see your exact liability under both regimes in seconds.

New vs Old Tax Regime: Which One Should You Choose?

The right choice depends entirely on the deductions and exemptions you can claim. For a deeper analysis, see our Old vs New Tax Regime comparison guide.

Choose the New Tax Regime if: you have minimal tax-saving investments; you do not pay rent (no HRA to claim); your gross salary is under ₹12.75 lakh and you'll likely pay zero tax; or you prefer simplicity and lower compliance.

Choose the Old Tax Regime if: your total deductions (Section 80C, 80D, HRA, home loan interest, etc.) exceed ₹3.5–₹4 lakh; you actively claim HRA and LTA; or you have a home loan with significant interest (up to ₹2 lakh deductible under Section 24(b)).

The income tax e-filing portal automatically calculates and suggests the better regime when you enter your details. Salaried taxpayers (without business income) can switch between regimes every year while filing.

Which ITR Form Should a Salaried Employee File for AY 2026-27?

Choosing the correct ITR form is critical — filing the wrong form results in a defective return notice under Section 139(9).

| ITR Form | Who Should Use It |

|---|---|

| ITR-1 (Sahaj) | Resident individual with total income up to ₹50 lakh: salary/pension + up to two house properties + other sources (interest, dividends) + LTCG under Section 112A up to ₹1.25 lakh. No carry-forward losses. |

| ITR-2 | Salary + capital gains (mutual funds, stocks, property) + more than two house properties + foreign income/assets + directors in a company + NRI/RNOR + ESOPs from eligible start-ups. |

| ITR-3 | Salary + business or professional income (freelance, F&O trading, consulting, partnership firm). |

| ITR-4 (Sugam) | Presumptive income under 44AD/44ADA/44AE — small business owners and freelancers below ₹50 lakh turnover. |

When in doubt, the e-filing portal often auto-suggests the right form based on the income heads you enter.

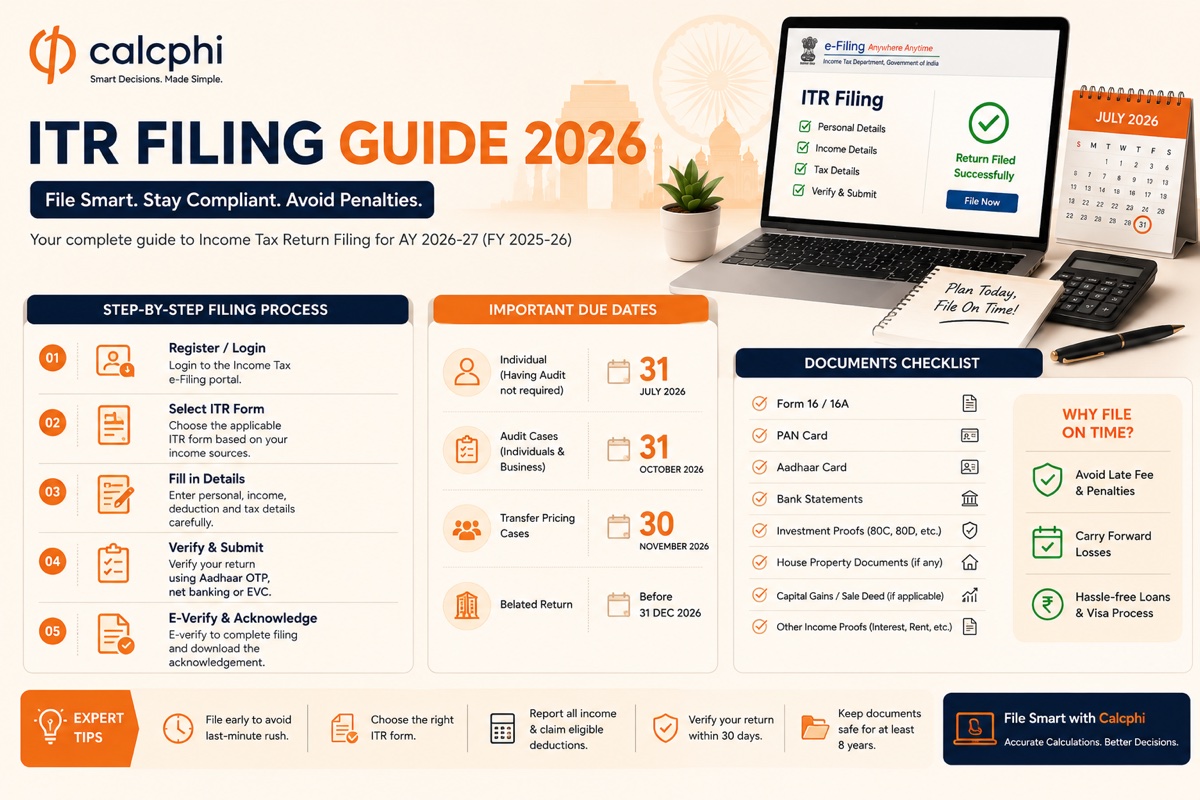

Documents Required for Filing ITR

- PAN Card and Aadhaar Card — both mandatory and must be linked

- Form 16 — issued by your employer summarising salary and TDS (available by 15 June)

- Form 16A / 16B / 16C — for TDS on non-salary income

- Form 26AS — consolidated tax credit statement; download from the portal

- Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) — for cross-verification of all reported income

- Bank account details including IFSC codes (for refund credit)

- Salary slips — for HRA and other allowance calculations

- Rent receipts and rental agreement — to claim HRA exemption

- Home loan interest certificate — for Section 24(b) deduction

- Proof of tax-saving investments — LIC premiums, ELSS, PPF, NPS, etc., for Section 80C

- Health insurance premium receipts — for Section 80D deduction

- Capital gains statement — from your broker or mutual fund platform

- Interest certificates — from banks and post offices for FDs and savings accounts

- Donation receipts — for Section 80G claims

Before filing, always reconcile your Form 16 with Form 26AS and AIS to ensure all incomes and TDS entries match.

Key Deductions for Salaried Employees (Old Regime)

If you opt for the old tax regime, here are the most valuable deductions to maximise your savings:

- Section 80C (up to ₹1.5 lakh): EPF, PPF, ELSS, life insurance premiums, principal repayment on home loan, tuition fees, NSC, 5-year tax-saving FD

- Section 80CCD(1B) (up to ₹50,000): Additional deduction for NPS contributions, over and above the 80C limit

- Section 80D: Health insurance premiums — up to ₹25,000 for self/family and an additional ₹25,000 (₹50,000 for senior citizen parents)

- Section 24(b): Up to ₹2 lakh deduction on home loan interest for self-occupied property

- HRA Exemption (Section 10(13A)): Least of — actual HRA received; 50% of salary (40% non-metro); rent paid minus 10% of salary. Use the HRA Calculator to find your exact exemption

- LTA: Tax-exempt for two journeys in a block of four years

- Section 80E: Full deduction on interest paid on education loans

- Section 80TTA / 80TTB: Up to ₹10,000 (₹50,000 for senior citizens) on savings account interest

- Section 80G: Deduction for eligible donations to charitable institutions

Under the new tax regime, most of these deductions are not available, with limited exceptions: standard deduction of ₹75,000, employer's NPS contribution under Section 80CCD(2) (up to 14% of basic salary), and certain transport allowances for specially-abled individuals.

Step-by-Step: How to File ITR-1 Online for AY 2026-27

- Visit incometax.gov.in and log in using your PAN as User ID. First-time users must register with PAN.

- Navigate to e-File → Income Tax Returns → File Income Tax Return.

- Select Assessment Year 2026-27 and mode of filing as Online. Click Start New Filing.

- Select your status as Individual and choose ITR-1 (or the applicable form).

- Pre-filled data from Form 26AS, AIS, and your employer's TDS return will appear automatically. Carefully verify personal details, salary income (compare with Form 16), house property income, other sources, and TDS entries.

- Choose your tax regime. The portal will compare both and suggest the better one.

- Enter eligible deductions from the drop-down menu (old regime). Verify your total income, tax liability, or refund amount.

- Pay any balance tax due using Challan ITNS 280, then submit your return.

- E-verify within 30 days using Aadhaar OTP, net banking, bank account EVC, demat EVC, or DSC. An unverified return is treated as not filed.

Important Due Dates for AY 2026-27

| Activity | Due Date |

|---|---|

| ITR filing for individuals (non-audit) — ITR-1 & ITR-2 | 31 July 2026 |

| ITR filing for non-audit ITR-3 & ITR-4 | 31 August 2026 |

| ITR filing for audit cases | 31 October 2026 |

| ITR filing for transfer pricing cases | 30 November 2026 |

| Belated and revised return | 31 December 2026 |

| Updated return (ITR-U) | Within 48 months from end of AY |

Filing after the due date attracts a late fee under Section 234F: ₹5,000 if filed after 31 July but before 31 December, or ₹1,000 if your total income is below ₹5 lakh. You also lose the right to carry forward most losses.

Common Mistakes to Avoid While Filing ITR

- Choosing the wrong ITR form — leads to a defective return notice under Section 139(9)

- Mismatched data between Form 16, Form 26AS, and AIS — always reconcile before filing

- Forgetting income from other sources — savings account interest, FD interest, and dividends are all taxable and visible in AIS

- Skipping foreign income or assets — even small foreign holdings must be disclosed under Schedule FA in ITR-2; non-disclosure attracts severe penalties under the Black Money Act

- Using ITR-1 with capital gains — ITR-1 doesn't have a capital gains schedule; any mutual fund redemptions mean you must use ITR-2

- Incorrect bank details — delays your refund; pre-validate your bank account on the portal before filing

- Not e-verifying within 30 days — an unverified return is treated as not filed

- Forgetting carry-forward losses — losses from previous years must be claimed every year to remain alive

What Happens After You File Your ITR?

Once your ITR is successfully submitted and e-verified, the Income Tax Department processes your return under Section 143(1). You will receive an intimation by email confirming one of three outcomes: no discrepancy (your ITR is accepted as is); a refund due (credited directly to your pre-validated bank account, usually within a few weeks); or a tax demand (you may need to pay additional tax or file a rectification). If your return is selected for scrutiny under Section 143(2), always respond to notices on time.

A Quick Look Ahead: The Income Tax Act, 2025

Although the Income Tax Act, 2025 comes into effect from 1 April 2026, your filing for AY 2026-27 (FY 2025-26) is still governed by the existing 1961 Act. The new Act will apply when you file for AY 2027-28 next year. It introduces a unified "Tax Year" concept, simplified language, and reduced redundancy — but core elements like slab rates, deductions, and rebates remain consistent for now.

Frequently Asked Questions

Is income up to ₹12 lakh really tax-free for salaried employees in FY 2025-26?

Yes. Under the new tax regime, the Section 87A rebate of up to ₹60,000 makes taxable income up to ₹12 lakh fully tax-free. Adding the standard deduction of ₹75,000, gross salary up to ₹12.75 lakh attracts zero tax.

Can I switch between the old and new tax regime every year?

Yes. Salaried individuals without business income can switch between regimes every year while filing the ITR. Those with business income can switch only once and must file Form 10-IEA to opt out of the new regime.

Is filing ITR mandatory if my employer has already deducted TDS?

Yes. TDS is only a tax payment, not a return. If your gross total income exceeds the basic exemption limit (₹4 lakh under the new regime), you must file an ITR irrespective of TDS deduction. Filing is also advisable even below the limit — it serves as income proof and enables refunds.

What if I miss the 31 July 2026 deadline?

You can file a belated return by 31 December 2026 with a late fee under Section 234F — ₹5,000 (or ₹1,000 if income is below ₹5 lakh) plus interest on any unpaid tax. However, you lose the right to carry forward most losses.

Do NRIs get the Section 87A rebate?

No. The Section 87A rebate is available only to resident individuals. NRIs and RNORs cannot claim it, regardless of their income level.

What is the difference between Form 16 and Form 26AS?

Form 16 is issued by your employer and shows your salary and TDS deducted from it. Form 26AS is a consolidated tax credit statement reflecting all TDS, advance tax, and self-assessment tax credited to your PAN from all sources — not just your employer. Always reconcile both before filing to catch any mismatches.

Calculate your tax before filing:

Income Tax Calculator → Old vs New Regime Calculator → HRA Exemption Calculator →Disclaimer: This article is for informational purposes only and should not be construed as tax or legal advice. Tax laws are subject to change. The information here is based on publicly available rules for FY 2025-26 / AY 2026-27. For personalised advice, please consult a qualified Chartered Accountant or tax professional.