HECS-HELP Repayment Guide 2026: Thresholds, Rates, and Paying It Off Faster

If you studied at university or TAFE in Australia, there is a good chance you graduated with a HECS-HELP debt sitting quietly in the background. For many Australians, it is the largest debt they carry before they even consider a home loan. Yet unlike a credit card or personal loan, HECS-HELP works very differently — and misunderstanding how it works can cost you years of unnecessary repayments or hundreds of dollars in avoidable indexation. This guide breaks down exactly how HECS-HELP repayments work in 2026-27, what the current income thresholds are, how indexation affects your balance, and what smart strategies can help you clear your debt faster.

What Is HECS-HELP and How Does It Work?

HECS-HELP stands for Higher Education Contribution Scheme — Higher Education Loan Program. When you enrol as a Commonwealth Supported Place (CSP) student at an Australian university, the government covers part of your tuition fees upfront and creates a debt in your name. That debt is recorded by the Australian Taxation Office (ATO) and sits interest-free — but it is not completely frozen.

Instead of charging interest, the government applies indexation to your balance each year on 1 June. Indexation means your debt grows in line with inflation, so the purchasing power of what you owe stays roughly constant over time. It is not the same as interest — but if the rate of indexation is high (as it was in 2023), your balance can grow faster than your repayments reduce it.

Repayments are income-contingent, meaning you only repay when you earn above a minimum income threshold. There is no fixed monthly repayment schedule. Your employer withholds the compulsory repayment amount from your salary each payslip once you notify them you have a HECS-HELP debt, and the ATO reconciles everything at tax time.

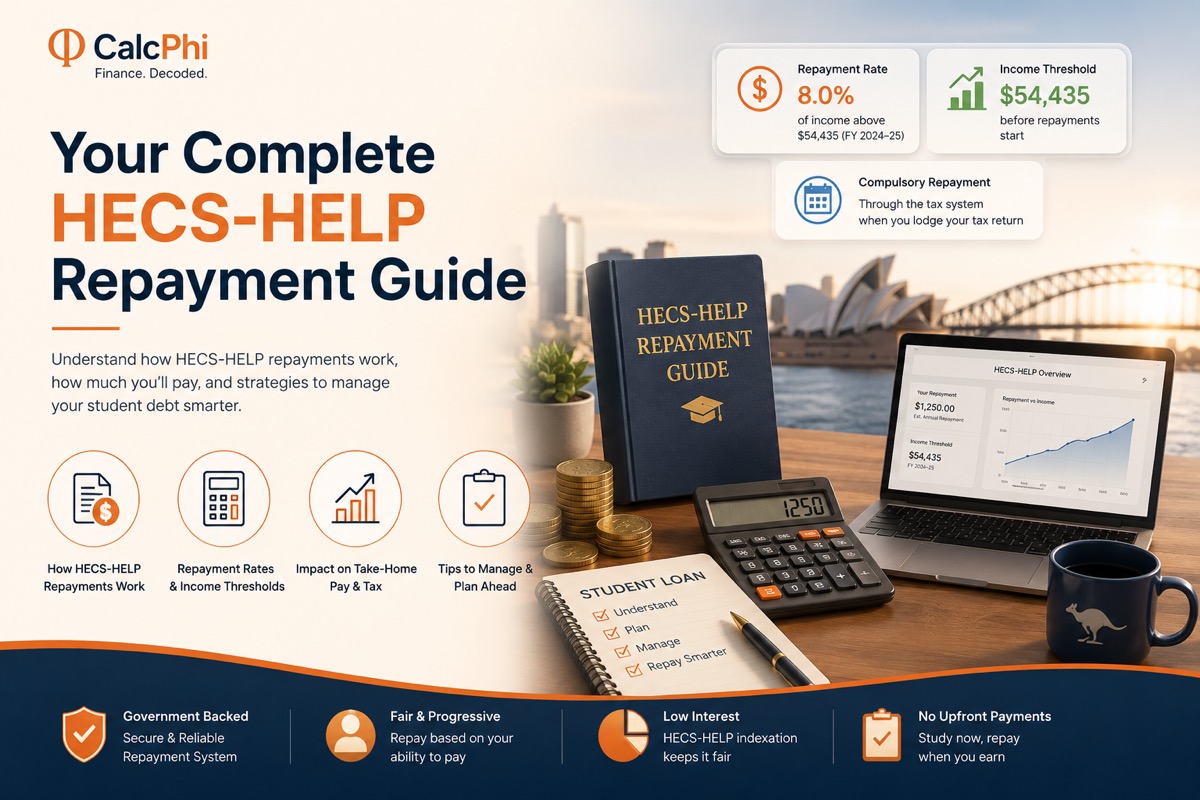

HECS-HELP Repayment Thresholds for FY2025–26

The repayment threshold is the income level at which you are legally required to start making HECS-HELP repayments. For FY2025–26, that threshold is $54,435. Below that figure, you owe nothing — even if you have a large outstanding balance.

Above $54,435, a percentage of your total income is applied as a compulsory repayment. The rate increases progressively as your income rises. It is important to understand that the repayment rate applies to your entire income, not just the amount above the threshold. So if you earn $65,000, your compulsory repayment is 2.0% of $65,000 — which equals $1,300 — not just 2% of the amount above $54,435.

| Annual Income | Repayment Rate |

|---|---|

| Below $54,435 | Nil |

| $54,435 – $62,998 | 1.0% |

| $62,999 – $66,819 | 2.0% |

| $66,820 – $70,539 | 2.5% |

| $70,540 – $74,919 | 3.0% |

| $74,920 – $79,489 | 3.5% |

| $79,490 – $84,268 | 4.0% |

| $84,269 – $89,524 | 4.5% |

| $89,525 – $95,092 | 5.0% |

| $95,093 – $100,996 | 5.5% |

| $100,997 – $107,214 | 6.0% |

| $107,215 – $113,847 | 6.5% |

| $113,848 – $120,899 | 7.0% |

| $120,900 – $128,392 | 7.5% |

| $128,393 – $136,331 | 8.0% |

| $136,332 – $144,730 | 8.5% |

| $144,731 – $151,200 | 9.0% |

| $151,201 and above | 10.0% |

Want to see your exact repayment amount and how many years until you are debt-free? Use CalcPhi's free HECS-HELP Repayment Calculator — enter your income, balance, and expected income growth to get a year-by-year projection instantly.

How HECS-HELP Indexation Works in 2026

Indexation is the mechanism that adjusts your HECS-HELP balance in line with the cost of living. It is applied on 1 June each year to your outstanding balance. Before 2023, the indexation rate was tied solely to the Consumer Price Index (CPI). In 2023, that resulted in a 7.1% increase — the highest in decades — which shocked many borrowers whose balances grew by thousands of dollars overnight.

The government responded by legislating a change: from 2024 onwards, indexation is applied at the lower of CPI or the Wage Price Index (WPI). For 2024-25, the indexation rate came down to approximately 4.0–4.7%. For 2025-26, analysts expect it to sit in the range of 3.0–3.5%, in line with moderating inflation. This is still not zero, though. On a $40,000 balance, a 3.2% indexation rate adds $1,280 to your debt in a single day — before any repayments offset it.

This is why understanding the interplay between your repayment rate and the indexation rate matters so much. If your income is near the lower end of the threshold bands, your annual repayment may be only slightly higher than what indexation adds back. Progress can feel painfully slow.

Real-World Repayment Examples

Graduate earning $72,000 with a $35,000 debt

At $72,000 income, the repayment rate is 3.5%, giving a compulsory repayment of $2,520 per year. With indexation at 3.2%, approximately $1,120 is added back to the $35,000 balance. The net annual reduction is around $1,400. At this rate, with modest income growth of 3.5% per year, it would take approximately 12 years to clear the debt — with total repayments of around $38,500.

Mid-career professional earning $110,000 with a $55,000 debt

At $110,000, the repayment rate jumps to 6.5%, meaning $7,150 is withheld annually. Indexation at 3.2% adds around $1,760 to the $55,000 balance. The net reduction is approximately $5,390 per year, and the debt would be cleared in roughly 8 years. These examples illustrate how significantly income affects your repayment trajectory — a salary increase that moves you into a higher threshold band can shave years off your debt.

Does HECS-HELP Debt Affect Your Home Loan?

Yes — and this surprises many first-home buyers. When a lender assesses your borrowing capacity, they treat your compulsory HECS repayment as a committed expense, just like a car loan repayment. It reduces your disposable income, which in turn reduces how much the bank will lend you.

On a $95,000 income with a 5.5% repayment rate, your HECS commitment is $5,225 per year — or about $435 per month. Depending on the lender's methodology, that could reduce your borrowing capacity by $80,000 to $100,000. If you are saving for your first home and wondering why your borrowing estimate feels lower than expected, your HECS-HELP debt may be a contributing factor.

Use CalcPhi's Salary Take-Home Pay Calculator to understand your true take-home pay after both tax and HECS withholding — this gives you a much clearer picture of what you can actually afford to borrow and repay.

Should You Pay Off HECS-HELP Early?

HECS-HELP is not a traditional debt. It does not accrue interest. The only cost is indexation, which in a normal inflation environment runs at 3–4% per year. That is relatively cheap compared to mortgage rates (currently 5.5–6.5%), credit card rates (18–22%), or personal loan rates (8–15%).

From a purely financial perspective, voluntary HECS repayments only make sense if the effective "cost" of your HECS debt — the indexation rate — is higher than the after-tax return you could earn by investing that money elsewhere. In a high-inflation year like 2023 when indexation hit 7.1%, that calculation shifted significantly toward paying off HECS. In a more normal 3–3.5% environment, many Australians are financially better off putting spare cash into super, an offset account on their mortgage, or an investment portfolio.

Note that the ATO used to offer a 5% discount on voluntary repayments of $500 or more. That incentive was abolished in January 2017 and has not returned. That said, there is a psychological value to being debt-free — and reducing your HECS balance does improve your borrowing capacity for a home loan, which has real financial consequences for many people in their late twenties and thirties.

4 Practical Strategies to Pay Off HECS Faster

1. Make voluntary lump-sum payments

You can make voluntary repayments at any time through the ATO's online services via myGov. There is no minimum amount and no penalty. If you receive a work bonus, an inheritance, or a tax refund, redirecting part of it to your HECS balance is a simple way to accelerate repayment — particularly in periods of high indexation.

2. Salary sacrifice into super

Salary sacrificing into super reduces your taxable income, which can drop you into a lower HECS repayment bracket. For example, if you earn $85,000 and salary sacrifice $5,000 into super, your taxable income falls to $80,000 — dropping your repayment rate from 4.5% to 3.5%. That saves you roughly $475 in HECS repayments while also building your retirement balance. Use CalcPhi's Salary Sacrifice Calculator to model this.

3. Check your withholding closely

Your employer withholds an estimated HECS repayment each payslip based on an annualised income figure. If your income varies — through overtime, commissions, or part-year work — the withholding can be off. Check your PAYG summary and tax return carefully each year to ensure the ATO's reconciliation is accurate.

4. Keep an eye on the June 1 indexation date

If you have spare cash and indexation is expected to be high in a given year, making a voluntary payment before 1 June means you pay indexation on a lower balance. Timing a lump-sum payment a few days before 1 June can save you a meaningful amount — particularly on large balances.

What Happens to Your HECS Debt If You Live Overseas?

From 1 January 2016, the ATO extended the repayment obligation to Australians living and working overseas. If your worldwide income exceeds the repayment threshold — currently $54,435 — you are required to submit a Worldwide Income Assessment each year and make repayments accordingly. The same threshold table applies regardless of whether your income is earned in Australia or abroad.

Before this change, it was common for Australians living overseas to simply ignore their HECS debt for years. That loophole is now closed, and penalties apply for non-compliance.

Frequently Asked Questions

-

What is the HECS-HELP repayment threshold for 2026-27?

The minimum repayment income threshold for FY2025–26 is $54,435. If your taxable income is below this amount, no HECS repayment is required for that financial year. The threshold is adjusted annually by the ATO in line with wage growth and is published as part of the annual tax schedule.

-

Does my HECS debt affect my take-home pay?

Yes. Once your income exceeds $54,435, your employer withholds an additional percentage from each payslip on top of regular income tax. This HECS withholding is separate from PAYG tax withholding and appears as a line item on your payslip. For someone earning $80,000, this amounts to roughly $266 per month being withheld toward HECS.

-

Is HECS-HELP debt cancelled if I die or become permanently incapacitated?

Yes. The ATO will waive or cancel a HECS-HELP debt if the borrower dies, is permanently unable to work, or if a doctor certifies that the debt is causing permanent financial hardship in extreme circumstances. This must be formally applied for through the Study Assist process administered by the Department of Education.

-

Can I claim a tax deduction for HECS-HELP repayments?

No. Compulsory HECS-HELP repayments are not tax-deductible because the debt was used for personal education, not for income-producing purposes. However, if you paid course fees out-of-pocket for a course directly related to your current job — and did not use HELP — those fees may qualify as a self-education expense deduction under ATO rules.

-

What happens if I overpay my HECS through payroll withholding?

If your employer withholds more than your actual compulsory repayment — which can happen if your income varies through the year — the ATO reconciles this at tax time and either credits the overpayment to your HECS balance or issues a tax refund, depending on your overall tax position. Lodging your tax return on time each year ensures this is handled correctly.

-

How do I check my current HECS-HELP balance?

Log in to your myGov account and navigate to the ATO section. Under "Tax" and then "Loan accounts," you can see your current HECS-HELP balance including any changes from indexation and the repayments applied from your most recent tax return. This is the most accurate and up-to-date figure available.

Use our Australia calculators:

HECS Repayment Calculator → Salary Take-Home Calculator → Salary Sacrifice Calculator → Income Tax Calculator →Disclaimer: The information in this article is for educational and general guidance purposes only. All repayment figures and threshold amounts are based on ATO-published data for FY2025–26 and are subject to change by the government. Nothing in this article constitutes financial advice. Individual circumstances vary significantly, and you should consult a qualified financial adviser (holding an Australian Financial Services Licence) for personalised guidance on managing your HECS-HELP debt and broader financial strategy.