Australia Income Tax Brackets 2026-27: What Your Salary Actually Costs in Tax

If you have ever looked at your payslip and thought "where did all my money go?" — this article is for you. Australia uses a progressive tax system, which means the more you earn, the higher the rate you pay on the portion of income that falls into each band. But it does not mean your entire salary gets taxed at the highest rate that applies to you.

By the end of this guide, you will know exactly how the 2026-27 tax brackets work, what each common salary level actually costs in tax, and how offsets like the Low Income Tax Offset (LITO) change your final bill. We have also included sections on how the Medicare levy, HECS-HELP debt, and salary sacrifice all interact with these brackets — because your real-world take-home pay depends on more than just the rate table.

How Australia's Progressive Tax System Works

Australia's income tax system is built on brackets, sometimes called "tax bands." Each bracket has a rate that applies only to the income that falls within that specific range — not to everything you earn. Think of it like filling buckets: the first bucket fills at 0%, the next at 19%, and so on.

For FY 2026-27, the tax-free threshold sits at $18,200. This means the first $18,200 of anyone's income is completely free of income tax. After that, the rate climbs across four additional brackets. The structure rewards lower and middle earners by ensuring the bulk of average wages are taxed at 19% or 32.5%, not at the top rate of 45%.

The 2026-27 Australian Income Tax Brackets

The following table shows the official ATO resident tax rates for the 2026-27 financial year. These rates apply to Australian tax residents only — non-residents face a different schedule with no tax-free threshold.

| Taxable Income Range | Marginal Tax Rate | Tax Owed on This Portion |

|---|---|---|

| $0 – $18,200 | 0% | Nil |

| $18,201 – $45,000 | 19% | Up to $5,092 |

| $45,001 – $135,000 | 32.5% | Up to $29,250 |

| $135,001 – $190,000 | 37% | Up to $20,350 |

| $190,001 and above | 45% | Uncapped |

On top of these rates, the Medicare levy of 2% is added to most taxpayers' bills. The levy funds Australia's public health system and kicks in at income levels above the low-income Medicare levy threshold (around $26,000 for singles in 2026-27). This brings the true marginal rates that most working Australians experience to 21%, 34.5%, 39%, and 47% at the relevant brackets.

Understanding Marginal Rate vs. Effective Tax Rate

One of the most common points of confusion — and one that genuinely costs Australians money in poor financial decisions — is mixing up marginal rate and effective rate.

Your marginal rate is the rate applied to the very next dollar you earn. If you earn $80,000, your marginal rate is 32.5% (or 34.5% including Medicare). That does not mean you pay 32.5% of $80,000. It means you pay 32.5% only on the portion of income above $45,000.

Your effective rate (also called the average rate) is simply your total tax bill divided by your gross income. It is almost always lower than the marginal rate, because the lower brackets are doing most of the heavy lifting for the first portion of your income.

Here is why the distinction matters practically: if you are offered a $10,000 pay rise and your marginal rate is 34.5%, you take home about $6,550 of that extra $10,000 — not $6,700 (which would be the case if your effective rate were 33%). Decisions about salary sacrifice into super, making additional deductible contributions, or whether to chase overtime all depend on your marginal rate, not your effective rate.

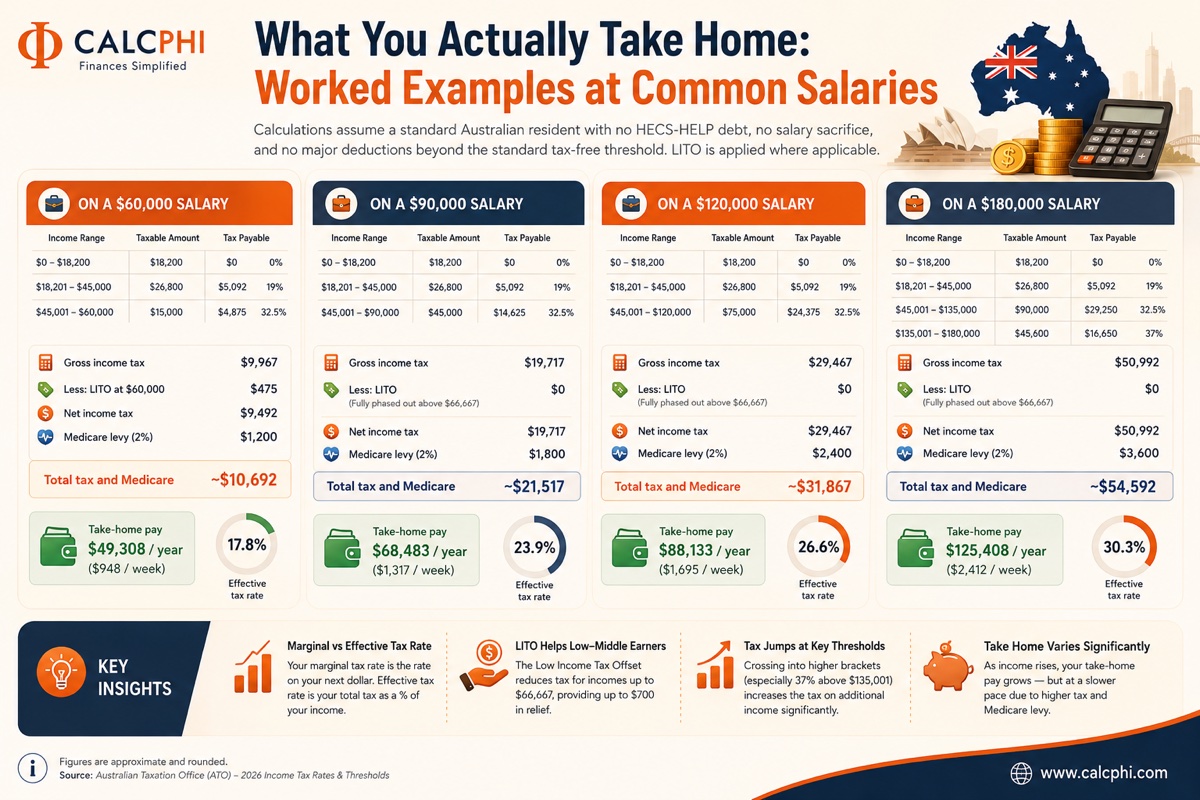

What You Actually Take Home: Worked Examples at Common Salaries

The calculations below assume a standard Australian resident with no HECS-HELP debt, no salary sacrifice arrangement, and no major deductions beyond the standard tax-free threshold. LITO is applied where applicable.

On a $60,000 Salary

- $0 to $18,200 — $0 tax

- $18,201 to $45,000 — $26,800 × 19% = $5,092

- $45,001 to $60,000 — $15,000 × 32.5% = $4,875

- Gross income tax: $9,967

- LITO at $60,000: $700 − ($15,000 × 1.5%) = $475 offset

- Net income tax: $9,967 − $475 = $9,492

- Medicare levy (2%): $60,000 × 2% = $1,200

- Total tax and Medicare: ~$10,692

- Take-home pay: approximately $49,308 per year ($948/week)

- Effective tax rate: ~17.8%

On a $90,000 Salary

At $90,000, LITO has fully phased out (it ceases at $66,667). The entire income above $45,000 is taxed at 32.5%.

- $0 to $18,200 — $0

- $18,201 to $45,000 — $5,092

- $45,001 to $90,000 — $45,000 × 32.5% = $14,625

- Gross income tax: $19,717

- LITO: $0 (fully phased out above $66,667)

- Medicare levy: $90,000 × 2% = $1,800

- Total tax and Medicare: ~$21,517

- Take-home pay: approximately $68,483 per year ($1,317/week)

- Effective tax rate: ~23.9%

On a $120,000 Salary

- $0 to $18,200 — $0

- $18,201 to $45,000 — $5,092

- $45,001 to $120,000 — $75,000 × 32.5% = $24,375

- Gross income tax: $29,467

- LITO: $0

- Medicare levy: $120,000 × 2% = $2,400

- Total tax and Medicare: ~$31,867

- Take-home pay: approximately $88,133 per year ($1,695/week)

- Effective tax rate: ~26.6%

On a $180,000 Salary

At $180,000, the earner spans three brackets — 19%, 32.5%, and 37%. The jump into the 37% bracket at $135,001 adds a meaningful extra impost.

- $0 to $18,200 — $0

- $18,201 to $45,000 — $5,092

- $45,001 to $135,000 — $90,000 × 32.5% = $29,250

- $135,001 to $180,000 — $45,000 × 37% = $16,650

- Gross income tax: $50,992

- LITO: $0

- Medicare levy: $180,000 × 2% = $3,600

- Total tax and Medicare: ~$54,592

- Take-home pay: approximately $125,408 per year ($2,412/week)

- Effective tax rate: ~30.3%

The Low Income Tax Offset (LITO) Explained

The LITO is one of the most important but least understood features of the Australian tax system. It is not a deduction — it is a direct reduction of the tax you owe after the standard bracket calculations are done. For 2026-27, the maximum LITO is $700, available to taxpayers earning up to $37,500.

- Between $37,500 and $45,000: offset reduces by 5 cents per dollar

- Between $45,001 and $66,667: offset reduces by 1.5 cents per dollar

- Above $66,667: LITO is entirely gone

The practical effect of LITO is to push the real tax-free threshold from $18,200 up to approximately $21,884. Someone earning $20,000 technically has $1,800 of taxable income above the threshold and would owe 19% × $1,800 = $342 in income tax — but the LITO of $700 more than covers this, so they actually owe $0.

How the Medicare Levy Surcharge Can Add Another 1–1.5%

The Medicare levy of 2% applies to most working Australians. But there is an additional surcharge — the Medicare Levy Surcharge (MLS) — that hits people who earn above $93,000 (for singles in 2026-27) and do not hold an appropriate level of private hospital cover.

| Income (Single) | MLS Rate |

|---|---|

| Up to $93,000 | 0% |

| $93,001 – $108,000 | 1% |

| $108,001 – $144,000 | 1.25% |

| $144,001 and above | 1.5% |

If you earn $100,000 and have no private hospital cover, you pay the standard 2% Medicare levy plus an extra 1% MLS — effectively a 3% health contribution on top of your income tax. For high earners, taking out private hospital insurance with a premium under $2,000 per year often saves money compared to paying the MLS.

How HECS-HELP Repayments Change Your Real Take-Home Pay

If you have a HECS-HELP debt, your take-home pay will be lower than the figures shown above, even though HECS repayments are not technically income tax. HECS-HELP repayments are calculated as a percentage of your repayment income and deducted by your employer alongside tax withholding.

For 2026-27, the repayment threshold is around $54,435. Repayment rates range from 1% at the lower threshold up to 10% for income above $151,200. On a $90,000 salary with a HECS-HELP debt, your employer withholds approximately 3.5% of your income ($3,150 per year) toward your debt. Add this to your ~$21,517 in tax and Medicare, and your effective deduction from gross income is closer to $24,667 — meaning take-home pay drops from $68,483 to around $65,333.

Salary Sacrifice: Reducing Your Tax Bracket Legally

Salary sacrifice into superannuation is one of the most powerful tools available to Australian workers for reducing their income tax bill. It works by redirecting a portion of your pre-tax salary into your super fund, which is then taxed at just 15% inside the fund instead of your marginal rate.

Consider someone earning $140,000. At this income level, the marginal rate is 37% plus 2% Medicare — a total of 39% on each additional dollar. If this person salary sacrifices $10,000 into super, their taxable income drops to $130,000, keeping them below the $135,000 threshold and back in the 32.5% bracket. The $10,000 is taxed at 15% inside super instead of 39% — a saving of $2,400 on that portion alone, plus the benefit of additional super growth.

The concessional (pre-tax) super contribution cap for 2026-27 is $30,000 per year, which includes your employer's compulsory 11.5% Superannuation Guarantee contributions. Plan your salary sacrifice around what remains of this cap after employer contributions.

Your Employer, PAYG, and the ATO: How Tax Gets Collected

Most Australian employees never deal directly with the ATO during the year. Your employer withholds tax from each pay cycle under the Pay As You Go (PAYG) withholding system, using ATO tax tables that estimate what you will owe for the full year. This withheld amount is sent to the ATO on your behalf.

At tax time — when you lodge your return by 31 October for self-lodgers, or later if using a registered tax agent — the ATO reconciles the total withheld against what you actually owe. If more was withheld than you owe, you get a tax refund. If less was withheld (common for people with multiple jobs or freelance income), you owe the balance.

Since Single Touch Payroll (STP) became universal, your employer reports each pay event to the ATO in real time. This means the ATO's pre-filled myTax already contains your salary and withholding data when you go to lodge — you just need to check, add any unreported income or deductions, and submit.

Frequently Asked Questions

What are the income tax brackets in Australia for 2026-27?

For Australian residents in FY 2026-27, the brackets are: 0% on income up to $18,200; 19% on $18,201 to $45,000; 32.5% on $45,001 to $135,000; 37% on $135,001 to $190,000; and 45% on income above $190,000. The Medicare levy of 2% applies on top of these rates for most taxpayers.

What is the tax-free threshold in Australia in 2026-27?

The official tax-free threshold is $18,200. However, when the Low Income Tax Offset (LITO) is applied, the effective tax-free amount rises to approximately $21,884 for eligible taxpayers — meaning people earning below this level pay no income tax at all.

How much tax do I pay on a $100,000 salary in Australia?

On a $100,000 salary with no deductions or offsets other than LITO (which is fully phased out at this income level), you pay approximately $22,967 in income tax plus $2,000 in Medicare levy — a total of around $24,967. Your effective tax rate is roughly 25%, even though your marginal rate is 34.5%.

What is the difference between marginal and effective tax rate?

Your marginal rate is the rate applied to the next dollar you earn — it is determined by which bracket your income sits in. Your effective rate is your total tax bill as a percentage of your total income. Because the lower brackets are taxed at lower rates, the effective rate is always lower than the marginal rate. The marginal rate is the one that matters for decisions like salary sacrifice, overtime, and side income.

Does the Medicare levy count as income tax in Australia?

Not technically — it is a separate levy collected alongside income tax. However, for practical budgeting purposes, most people treat it as part of their overall tax rate because it is deducted from every pay in the same withholding calculation. The standard Medicare levy is 2%, and higher earners without private hospital cover may also pay the Medicare Levy Surcharge of 1% to 1.5% on top.

How can I legally reduce my income tax in Australia?

The most effective legal methods include: salary sacrificing into superannuation (taxed at 15% inside the fund instead of your marginal rate), claiming legitimate work-related deductions, making personal deductible super contributions, investing in negatively geared property (though this involves other risks), and — for higher earners — taking out private hospital cover to avoid the Medicare Levy Surcharge. Each strategy has different rules and suitability depending on your circumstances.

Disclaimer: The calculations, bracket figures, and worked examples in this article are for educational and estimation purposes only. While every effort has been made to ensure accuracy based on ATO guidelines for FY 2026-27, individual tax outcomes can vary based on specific circumstances including deductions, offsets, residency status, and other income sources. Nothing in this article constitutes financial or tax advice. Please consult a registered tax agent or qualified financial adviser for guidance tailored to your situation.

Written & verified by James O'Brien

Chartered Tax Adviser & CPA

James is a CPA and registered tax agent based in Melbourne with 14 years of experience in Australian tax law, CGT, PAYG withholding, and HECS-HELP repayment rules for salaried professionals and investors.