Conveyancing Australia Guide: What It Costs and What Your Conveyancer Does

Buying a property is the largest financial commitment most Australians will ever make — and yet one of the least understood parts of the process is conveyancing. Most buyers know they need a conveyancer, sign the paperwork, and receive keys at the end. But very few understand what actually happens between signing the contract and settlement day, why it takes weeks, and what they are paying for.

This guide explains every stage of the conveyancing process in plain language, breaks down exactly what you will pay in 2026, and shows you how to work with your conveyancer to make the transaction as smooth as possible.

What Is Conveyancing?

Conveyancing is the legal process of transferring ownership of real property from one person to another. In Australia, it is a mandatory part of every property transaction — whether you are buying a house, apartment, townhouse, or a vacant block of land. Conveyancing cannot be skipped or simplified away; the law requires a formal title transfer, and that transfer requires specific legal documents, searches, and registrations to be completed correctly.

The person who handles this process on your behalf is called a conveyancer or a property solicitor. Both can perform conveyancing legally, but they differ in their qualifications and what else they can do — more on that below.

In most Australian states, the entire conveyancing process now happens electronically through a platform called PEXA (Property Exchange Australia). This has made settlement faster and more secure, though it has not reduced the complexity of the underlying legal work.

The Five Stages of Conveyancing — Explained

Understanding the timeline of a property purchase makes the whole process far less stressful. Here is what your conveyancer is doing at each stage.

Stage 1: Pre-Exchange Review

This is the most important stage, and sadly the one most buyers rush. Before you sign a contract of sale, your conveyancer reviews the entire document on your behalf. This includes checking the title for any easements (rights others may have over the land, such as electricity lines or shared driveways), encumbrances (charges or restrictions on the title), covenants (conditions attached to how the land can be used), and any special conditions the vendor has included.

For apartments and townhouses, your conveyancer also reviews the strata records — levies, pending special levies, by-laws, and any disputes or defects affecting the building. A pending special levy for a building facade repair, for example, could mean an unexpected bill of $10,000 or more shortly after you move in.

At this stage, your conveyancer can flag concerns and negotiate amendments to the contract before you are legally committed. Engaging a conveyancer before you sign is the single most valuable thing you can do.

Stage 2: Exchange of Contracts

Exchange is the moment both parties sign the contract and it becomes legally binding. For private sale properties, this typically happens after price and conditions have been negotiated. For auction properties, exchange occurs when the hammer falls — you sign and hand over the deposit (usually 10% of the purchase price) on the day.

After exchange, a cooling-off period applies in most states for private sales — typically two to five business days — during which you can withdraw from the contract, usually with a small financial penalty (0.25% of the purchase price in NSW, for example). Auctions have no cooling-off period. Your conveyancer will confirm the cooling-off rules for your state and property type.

Stage 3: Searches and Due Diligence

Once under contract, your conveyancer orders a comprehensive set of property searches. These verify the legal and financial status of the property and are essential to protect you at settlement. Typical searches include:

- Title search (confirms the vendor legally owns the property and there are no undisclosed mortgages)

- Land tax clearance certificate (confirms no outstanding land tax is owed by the vendor that could become your liability)

- Council rate certificate (confirms the current council rates and any outstanding amounts)

- Water/sewerage search (outstanding charges and location of pipes)

- Land registry search (zoning, heritage overlays, road widening proposals)

- Body corporate / owners corporation records (for strata properties)

Each search has a separate fee, and the costs are passed to you as disbursements. Most searches take a few days to return; some council searches in regional areas can take longer. This stage typically spans the first two to four weeks after exchange.

Stage 4: Settlement Preparation

In the weeks before settlement, your conveyancer coordinates with your lender, the vendor's conveyancer, and the relevant state land registry to prepare all documentation. Key tasks include preparing the transfer of land document, calculating settlement adjustments (the financial split of council rates and water charges between buyer and seller as of the settlement date), and confirming the final settlement figures with your lender.

Your lender will issue a loan drawdown instruction confirming how much they are contributing to settlement. Your conveyancer reconciles this with the outstanding purchase price and your own contribution, ensuring the exact correct amount is transferred on settlement day.

Thinking about how much you can borrow for your purchase? Use CalcPhi's free Borrowing Power Calculator to see your maximum loan based on income, existing debts, and the APRA 3% serviceability buffer — no sign-up needed.

Stage 5: Settlement

Settlement is the day legal ownership transfers. In most Australian states, this now occurs entirely through the PEXA electronic settlement platform. Funds are transferred between financial institutions in real time, the title is registered in your name with the state land registry, and the vendor's real estate agent is authorised to release the keys.

You do not need to attend settlement in person — it is handled digitally by your conveyancer and your lender. The entire process typically takes 15 to 30 minutes on the day. You will receive a settlement confirmation from your conveyancer, at which point the property is legally yours.

How Much Does Conveyancing Cost in Australia?

Conveyancing fees vary by state, complexity, and whether you use a traditional conveyancer, a property solicitor, or an online conveyancing service. Here is a realistic breakdown for a standard residential purchase in 2026.

| Cost Item | Typical Range (AUD) | Notes |

|---|---|---|

| Professional fee | $800 – $1,800 | Fixed or hourly; confirm upfront |

| Title search | $30 – $80 | State land registry fee |

| Searches (council, water, land tax) | $200 – $500 | Disbursements; varies by state |

| PEXA electronic settlement fee | $100 – $150 | Platform fee |

| Land transfer registration | $100 – $300 | State-dependent |

| Total conveyancing (exc. stamp duty) | $1,200 – $2,600 | Standard residential purchase |

Stamp duty is separate and is one of the largest costs of buying property in Australia. In NSW, stamp duty on an $800,000 property is around $31,490 for a non-first-home buyer. First home buyers may be fully or partially exempt depending on the property value and state. Use CalcPhi's Stamp Duty Calculator to get an exact figure for your state, property value, and buyer status in under 30 seconds.

Online conveyancing platforms can reduce professional fees to $800–$1,200 for straightforward transactions. They are suitable for standard residential purchases in metropolitan areas with clean titles and no complications. For off-the-plan purchases, rural properties, deceased estates, or properties with title issues, a more experienced and typically higher-fee practitioner is worth the extra cost.

Conveyancer vs Property Solicitor: Which Should You Choose?

A licensed conveyancer specialises exclusively in property transactions. They are regulated by state-based licensing bodies (such as the Australian Institute of Conveyancers), carry professional indemnity insurance, and are trained specifically for the work involved. For the vast majority of residential property purchases, a licensed conveyancer is entirely sufficient.

A property solicitor (lawyer) has broader legal qualifications that encompass property law among other areas. The key advantage of a solicitor is that they can handle legal issues that go beyond conveyancing — contract disputes, boundary disagreements, vendor disclosure breaches, or complex off-the-plan contractual conditions. If your transaction has any unusual complexity, a solicitor provides greater legal protection.

For a standard suburban house or apartment purchase, a licensed conveyancer with strong reviews and clear communication is the right choice for most buyers. Price should not be the deciding factor — a $200 saving that results in a missed search or a contract clause you didn't understand is not a saving at all.

Settlement Adjustments: The Numbers Your Conveyancer Calculates

Many buyers are surprised to find the final settlement amount differs slightly from what they expected. This is because of settlement adjustments — the financial reconciliation of expenses the vendor has paid in advance or owes up to the settlement date.

The most common adjustments are council rates and water rates. If the vendor has paid the full quarter's council rates and settlement occurs mid-quarter, you reimburse the vendor for the remaining days of the quarter. Conversely, if rates are in arrears, the vendor pays those from settlement funds. Your conveyancer calculates these to the day and includes them in the settlement statement provided before settlement.

After settlement, you will also need to set up your mortgage repayments. CalcPhi's Mortgage Calculator shows your exact monthly repayment, total interest over the loan term, and a full amortisation schedule — useful for planning your budget in those first weeks of home ownership.

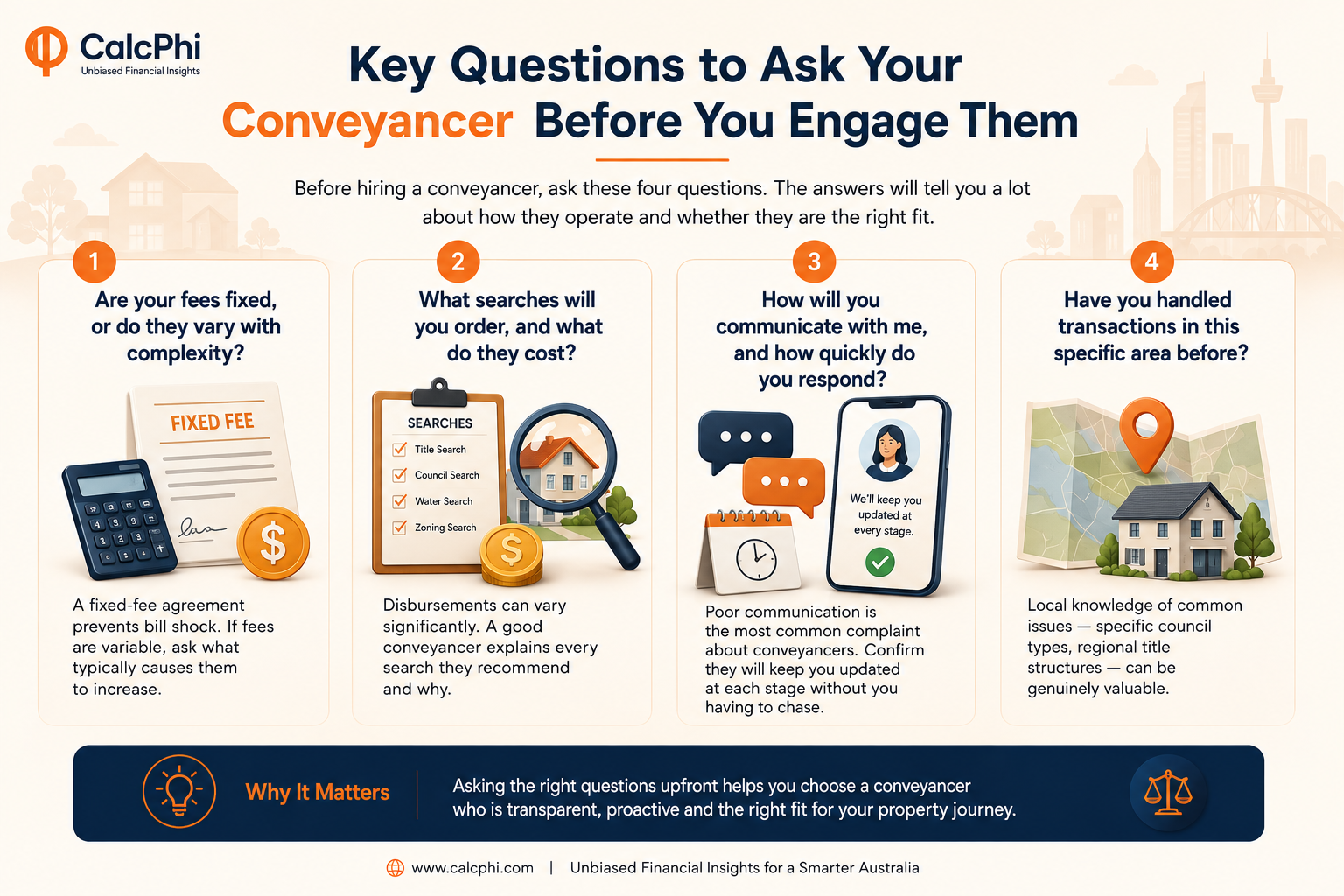

Key Questions to Ask Your Conveyancer Before You Engage Them

Before hiring a conveyancer, ask these four questions. The answers will tell you a lot about how they operate and whether they are the right fit.

- Are your fees fixed, or do they vary with complexity? A fixed-fee agreement prevents bill shock. If fees are variable, ask what typically causes them to increase.

- What searches will you order, and what do they cost? Disbursements can vary significantly. A good conveyancer explains every search they recommend and why.

- How will you communicate with me, and how quickly do you respond? Poor communication is the most common complaint about conveyancers. Confirm they will keep you updated at each stage without you having to chase.

- Have you handled transactions in this specific area before? Local knowledge of common issues — specific council types, regional title structures — can be genuinely valuable.

What Happens If Something Goes Wrong?

Conveyancing is generally a smooth process, but issues do arise. Common complications include title defects (easements or covenants not disclosed by the vendor), settlement delays (vendor finance falling through, documentation not ready), or failed pre-settlement inspections (where the property's condition has materially changed since the contract was signed).

Your conveyancer's job is to identify and manage these issues. If the vendor cannot settle on the agreed date, your conveyancer can issue a notice to complete — a formal legal notice giving the vendor a further 14 days to settle, during which you can claim penalty interest on the purchase price. If they still fail to settle, you may be entitled to rescind the contract and recover your deposit and associated costs.

Understanding your rights in these scenarios is exactly why engaging a qualified professional — rather than attempting self-conveyancing — is the right decision for the overwhelming majority of buyers.

Plan your full property purchase costs with CalcPhi's free Australian calculators:

Stamp Duty Calculator → Mortgage Calculator → Borrowing Power Calculator → First Home Buyer Calculator →Frequently Asked Questions

When should I engage a conveyancer?

Before you sign anything. For private sale properties, engage your conveyancer before making a formal offer, so they can review the contract first. For auction purchases, you need your conveyancer briefed at least a week before auction day — there is no cooling-off period after an auction, so any issues with the contract must be identified beforehand. Acting early costs nothing extra and can save you significantly.

Can I do my own conveyancing in Australia?

Legally, self-conveyancing is permitted in some states (NSW, VIC, and QLD do allow it). In practice, however, most lenders require a qualified conveyancer or solicitor to handle the settlement if there is a mortgage involved — which applies to most buyers. Beyond the lender requirement, the risk of missing a critical search, lodging incorrect documents, or missing a deadline is real and potentially very costly. For most buyers, the professional fee is a very small cost relative to the value of the transaction.

How long does conveyancing take in Australia?

A standard residential property transaction typically takes between four and twelve weeks from exchange to settlement. The most common settlement period is six weeks, though buyers and vendors can negotiate shorter or longer periods depending on their circumstances. Off-the-plan purchases have much longer timelines — often one to three years from contract exchange to settlement, depending on construction completion.

What is the difference between exchange and settlement?

Exchange is when both parties sign the contract — you are legally committed at this point. Settlement is when the legal ownership actually transfers and you receive the keys. The period between exchange and settlement (typically four to six weeks) is when your conveyancer conducts searches, prepares documents, and coordinates with your lender. Think of exchange as "sold" and settlement as "yours."

What does the PEXA fee cover?

PEXA (Property Exchange Australia) is the electronic platform used for settlement in most Australian states. The PEXA fee — typically $100 to $150 for buyers — covers the digital lodgement and registration of the title transfer and the secure electronic transfer of settlement funds between financial institutions. It replaces the older manual settlement process of meeting physically with cheques.

Is stamp duty paid at settlement?

Stamp duty timing varies by state. In NSW, stamp duty is due within three months of the contract date (or 14 days in some circumstances). In Victoria, it is due at settlement. Your conveyancer will advise you of the specific timing and payment method for your state. Failing to pay stamp duty on time results in penalty interest. Use CalcPhi's Stamp Duty Calculator to confirm your exact duty liability before exchange.

Disclaimer: The information in this article is for educational and general guidance purposes only. Conveyancing fees, stamp duty rates, and legal processes vary by state and individual transaction circumstances. Nothing in this article constitutes legal or financial advice. Always engage a licensed conveyancer or property solicitor for your specific transaction, and consult a qualified financial adviser for personalised guidance on your property purchase.