Buying vs Renting in Australia 2026: The Real Financial Comparison

Australians have been told for decades that renting is "throwing money away" and that buying a home is the surest path to financial security. The reality in 2026 is far more nuanced. In cities like Sydney, where the median house price has crossed $1.6 million, buying the same property you can rent costs tens of thousands of dollars more per year — at least in the short run. The wealth-building argument for buying is real, but it plays out over the long term through leveraged capital growth, not through annual cash savings.

This guide cuts through the cultural noise and gives you the actual numbers by city, the hidden costs both sides ignore, and a clear framework to help you decide what makes financial sense for your situation right now.

What Does Buying a Home Actually Cost in 2026?

Most people think of homeownership costs as the mortgage repayment. That is only part of the picture. The true cost of owning a property includes upfront purchase costs, ongoing holding costs, and the opportunity cost of your capital — all of which renters avoid.

Upfront Costs When Buying

Before you even get the keys, buying a property comes with a significant set of one-time costs that most buyers underestimate. For a median Sydney house at $1.6 million with a 20% deposit:

| Cost Item | Estimated Amount |

|---|---|

| Deposit (20%) | $320,000 |

| Stamp duty (NSW, owner-occupier) | ~$67,500 |

| Legal / conveyancing fees | ~$2,000 |

| Building and pest inspection | ~$700 |

| Loan application / establishment fees | ~$600 |

| Lenders Mortgage Insurance (if <20% deposit) | $0 |

| Moving costs | ~$1,500 |

| Total cash required at settlement | ~$392,300 |

For the same property with only a 10% deposit ($160,000), you'd also face Lenders Mortgage Insurance of approximately $25,000–$35,000 — a cost that protects the lender, not you. Stamp duty varies significantly by state: a $1 million property attracts around $40,000 in Victoria, $40,490 in NSW, $38,550 in Queensland, and roughly $43,000 in Western Australia.

Annual Holding Costs When You Own

Once you've bought, you face a recurring set of costs every year that most buy-vs-rent comparisons ignore:

| Cost Item | Annual Amount |

|---|---|

| Mortgage repayments (principal + interest) | $94,800 |

| Of which: interest only (year 1) | ~$79,360 |

| Council rates | ~$1,800–$2,500 |

| Water and sewerage rates | ~$900–$1,200 |

| Building and contents insurance | ~$2,000–$3,000 |

| Maintenance and repairs (1% of value) | ~$16,000 |

| Total annual cost of ownership (owner-occupier) | ~$115,500 |

The maintenance figure of 1% of property value per year is a widely used industry rule of thumb. On a $1.6 million home, that's $16,000 per year for ongoing upkeep — plumbing, painting, appliances, gutters, roof repairs, and so on. This cost does not exist for renters; it is the landlord's responsibility entirely.

The True Cost of Renting in 2026

Renting is not free, and it is not without financial consequence — but it is also not the financial dead-end it is made out to be. According to Domain's April 2026 Rental Report, median weekly house rents across Australia's major cities are:

| City | Median Weekly House Rent | Annual Rent |

|---|---|---|

| Sydney | $775 | $40,300 |

| Melbourne | $580 | $30,160 |

| Brisbane | $660 | $34,320 |

| Perth | $700 | $36,400 |

| Adelaide | $620 | $32,240 |

| Hobart | $580 | $30,160 |

The critical financial question for renters is not just what they pay — it is what they do with the money they save compared to owning. That is where the renting-vs-buying equation either works in your favour or collapses entirely.

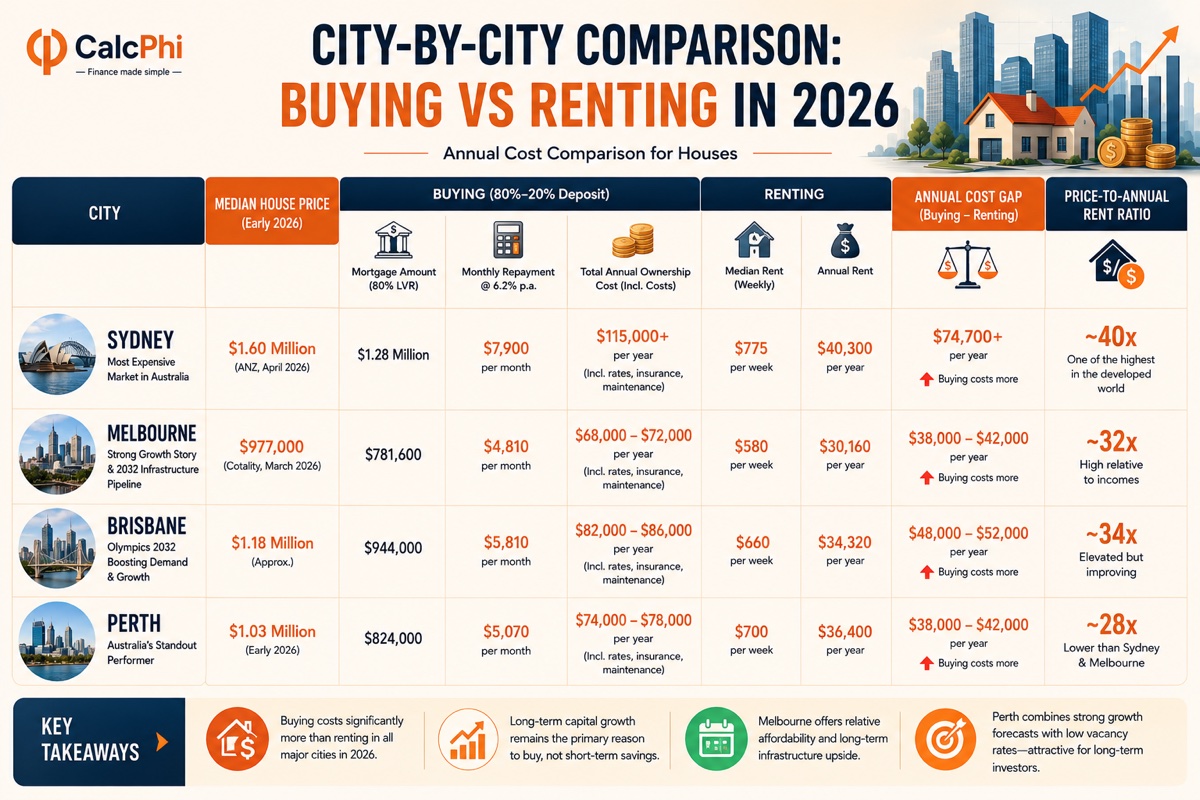

City-by-City Comparison: Buying vs Renting in 2026

Sydney

With a median house price of around $1.6 million (ANZ data, April 2026), Sydney remains the most expensive market in Australia. An 80% mortgage of $1.28 million at 6.2% costs approximately $7,900 per month — or $94,800 per year — before rates, insurance, and maintenance. Total annual ownership cost comes to approximately $115,000 or more. Renting the same house costs around $775 per week, or $40,300 per year. The annual cost of buying exceeds renting by more than $74,000 in year one. The price-to-annual-rent ratio is approximately 40x — one of the highest in the developed world.

The case for buying in Sydney rests entirely on long-term capital growth. Sydney values have risen by 31% over the past five years and have averaged 6–7% annually over the long term. But in the short run, buyers pay a very steep premium over renters.

Melbourne

Melbourne's median house price sits at around $977,000 (Cotality, March 2026). An 80% mortgage of $781,600 at 6.2% costs approximately $4,810 per month, or $57,720 per year. With rates, insurance, and maintenance, total annual holding costs reach approximately $68,000–$72,000. Median weekly rent for a house is $580, meaning annual rent is around $30,160. The annual cost gap between buying and renting in Melbourne is approximately $38,000–$42,000.

Melbourne's relative affordability compared to Sydney, combined with its long-term growth story and the 2032 infrastructure pipeline, makes it an interesting market for buyers with a 7–10 year horizon.

Brisbane

Brisbane has been one of Australia's strongest property markets over the past five years, with values rising 84–86% since 2021. The median house price is now approximately $1.18 million. A 20% deposit leaves a $944,000 mortgage at 6.2%, costing around $5,810 per month, or $69,720 per year. Including holding costs, total annual ownership cost is approximately $82,000–$86,000. Median rent is $660 per week — $34,320 annually. The annual cost gap is approximately $48,000–$52,000.

The Olympics effect — Brisbane is hosting the 2032 Summer Games — continues to support property demand and long-term growth expectations, particularly in inner-city and transport-corridor suburbs.

Perth

Perth has been Australia's standout performer, with median house prices rising 90% over five years and reaching approximately $1.03 million in early 2026. KPMG forecasts Perth to lead house price growth nationally at 12.8% in 2026. A 20% deposit leaves an $824,000 mortgage, costing around $5,070 per month, or $60,840 per year. With holding costs, total annual ownership cost is approximately $74,000–$78,000. Median weekly rent is around $700 — $36,400 annually. The annual cost gap is approximately $38,000–$42,000.

Perth's price-to-rent ratio remains lower than Sydney and Melbourne despite recent rapid growth, and combined with strong rental demand (vacancy rates below 1%), the investment case for buying in Perth in 2026 is compelling for long-term holders.

The Opportunity Cost Argument: What Happens to Your Deposit?

One of the most overlooked elements of the buying calculation is the opportunity cost of your deposit. A 20% deposit on a $1.6 million Sydney home is $320,000. If instead of putting that into a property, you invested it in a diversified share portfolio returning 8% per annum, it would grow to approximately $345,600 in year one — a gain of $25,600. Over 10 years at 8% p.a., that $320,000 compounds to around $690,000.

This is not an argument against buying. It is an argument for thinking clearly about all the returns involved. Property benefits from leverage — you put in $320,000 and control $1.6 million worth of asset. If that asset grows at 6% per year, the $1.6 million property gains $96,000 in year one, which is a 30% return on your $320,000 cash invested. Shares growing at 8% on your $320,000 return $25,600. Leverage fundamentally changes the comparison in property's favour.

The Renting-and-Investing Strategy: Does It Actually Work?

The renting-and-investing strategy — also called "rent-vesting" — involves renting in the area where you want to live while investing the money you save (compared to owning) in shares, ETFs, or investment properties elsewhere. In theory, if renting costs $40,000 per year and owning the equivalent property costs $115,000, you invest the $75,000 difference and build wealth that way.

In theory, this works brilliantly. In practice, it requires three things most people struggle with: the discipline to actually invest rather than spend the savings, the risk tolerance to stay invested through market downturns, and the financial literacy to build and manage a share or property portfolio effectively.

Research consistently shows that the biggest advantage of buying is the behavioural one. A mortgage is a forced savings plan — you have no choice but to make repayments every month. Renting requires active, disciplined investing of the surplus, and many people simply do not maintain that discipline. If you are confident in your investing habits, renting and investing can be a viable wealth strategy. If you are not, homeownership provides a powerful structure that automates wealth-building.

When Buying Clearly Makes Sense

Buying makes stronger financial sense when several conditions align. The most important is your time horizon — the property transaction costs (stamp duty, legal fees, agent fees when you sell) mean you need to hold a property for at least 7–10 years in a high-cost city before capital growth meaningfully outweighs those costs. In more affordable markets with lower price-to-rent ratios, this break-even period can be 4–6 years.

Buying also makes sense when you have job and income stability, when you want the lifestyle benefits of permanence (renovating to your taste, having pets, raising children in one school zone), and when you are buying in a high-growth corridor — inner-ring suburbs, near planned transport infrastructure, or in markets like Perth and Brisbane with strong population growth and limited housing supply.

For first home buyers specifically, 2026 offers meaningful support. The First Home Guarantee scheme allows eligible buyers to purchase with as little as a 5% deposit without paying LMI. State-based grants of $10,000–$30,000 are also available for new builds in most states.

When Renting Makes Stronger Financial Sense

Renting is the smarter short-term choice when your time horizon is less than five years — moving cities for work, relationship uncertainty, or career transitions all make renting the flexible choice. It also makes sense when your deposit is below 20% and you would face significant LMI costs, when the price-to-rent ratio in your target suburb is extremely high (above 35x annual rent), or when buying would stretch your budget to a point that leaves little financial buffer.

Renting also provides genuine lifestyle and financial flexibility that is easy to undervalue. If a better job opportunity comes up in another city, a renter can move in 60 days. An owner-occupier faces a selling process, agent fees of 2–3%, legal costs, and the emotional cost of leaving. In fast-changing careers and industries, that mobility has real financial value.

Finally, renting in an area you cannot afford to buy — a well-located suburb with great schools and transport — while buying an investment property in a more affordable market (rent-vesting) is a growing strategy among younger Australians.

The Behavioural Edge of Buying

No financial model fully captures the behavioural reality of money decisions. Buying a home is one of the most powerful wealth-building mechanisms Australians have access to — not solely because property grows in value, but because it forces you to save, month after month, year after year, without relying on willpower. Every repayment builds equity. Every year of ownership compounds your capital gains on a leveraged asset.

For many Australians, especially those without strong investing habits or financial confidence, this forced-savings mechanism is worth more than any theoretical return advantage renting-and-investing might offer on paper. The behavioural argument for buying is not irrational — it is grounded in decades of real-world financial psychology.

Frequently Asked Questions

Is renting really "throwing money away" in Australia?

No. Rent pays for housing — a real service with genuine value. You are not throwing money away any more than you throw money away on food or utilities. Mortgage interest, which forms the majority of repayments in the early years of a loan, is also money that does not build equity — it goes to the bank. In 2026, the interest component of a $1.28 million Sydney mortgage at 6.2% is approximately $79,360 in year one alone. The relevant question is not whether renting wastes money, but whether buying offers better value over your specific time horizon.

How many years do you need to hold a property to make buying worth it in Australia?

In high-cost cities like Sydney and Melbourne, the general break-even point — where capital growth and equity build-up outweigh transaction costs and the higher annual ownership cost — is around 7 to 10 years. In more affordable markets like Adelaide, Hobart, and regional areas with lower price-to-rent ratios, break-even can occur in 4 to 6 years. The faster a property appreciates, the shorter the break-even period.

What are the hidden costs of buying a home that people miss?

The most commonly missed costs are stamp duty (which can be $40,000 to $80,000+ depending on the state and price), maintenance and repairs (budget around 1% of property value per year), council and water rates (typically $2,500–$3,500 per year combined), building insurance, and the opportunity cost of your deposit capital. Buyers who calculate only the mortgage repayment typically underestimate total ownership cost by 30–50%.

Can I use superannuation to buy a house in Australia?

Under the First Home Super Saver Scheme (FHSS), you can withdraw up to $50,000 in voluntary super contributions — both concessional (pre-tax) and non-concessional (after-tax) — to use as part of your home deposit. This is the only legal mechanism for using super to buy a home. You cannot access compulsory employer Superannuation Guarantee contributions through FHSS. The tax advantage of saving within super often makes this strategy worthwhile for first home buyers.

What is a good price-to-rent ratio, and how do I use it?

The price-to-rent ratio is calculated by dividing the property purchase price by the annual rent for an equivalent property. A ratio below 15x generally favours buying, 15–20x is a neutral zone, and above 20x tends to favour renting from a pure cash-flow standpoint. Sydney's ratio sits at approximately 40x in 2026 — one of the highest globally — while regional markets often sit in the 15–20x range, making them more favourable for buyers from a yield perspective.

How does stamp duty affect the buy-vs-rent decision?

Stamp duty is a significant upfront cost that directly affects how long you need to hold a property before buying makes financial sense. On a $1 million home in NSW, stamp duty is approximately $40,490. If a property grows 6% annually, it takes roughly three years just to recover that stamp duty cost before any other transaction costs. In markets with higher price growth, this recovery is faster — but it underscores why short time horizons make buying expensive relative to renting.

Disclaimer: The calculations, figures, and comparisons in this article are provided for educational and estimation purposes only. Property prices, interest rates, stamp duty rules, and rental figures are subject to change and vary by location and individual circumstance. Nothing in this article constitutes financial advice. Please consult a qualified financial adviser holding an AFS licence before making any property purchase or investment decision.

Written & verified by Emma Hartley

Certified Financial Planner & Mortgage Specialist

Emma is a CFP based in Brisbane with 9 years of experience in mortgage advice, first home buyer strategy, and retirement planning for Australian households navigating property markets and the age pension system.