Under-Construction vs Ready-to-Move Property: A Full Financial Comparison for Indian Buyers (2026)

Every Indian home buyer eventually faces this fork in the road. The under-construction flat is priced at ₹75 lakh, delivery promised in three years, and the builder's sales team is telling you it's the deal of the decade. The ready-to-move flat in the same locality is listed at ₹95 lakh — you can move in next month. On paper, the gap looks like ₹20 lakh in your favour if you go under construction. But the full financial picture is far more complicated, and for many buyers, the "cheaper" option ends up costing more by the time possession arrives.

The Hidden Costs That Change Everything

The sticker price difference between an under-construction (UC) and a ready-to-move (RTM) property rarely tells the real story. What matters is the total outflow over the entire waiting period — and that number is driven by four factors that most buyers underestimate.

GST: The Tax That Only Hits Under-Construction Buyers

Under-construction properties attract GST at 5% of the agreement value for regular housing and 1% for affordable housing (units priced below ₹45 lakh in metro cities). Ready-to-move properties — those that have received a completion certificate from the local municipal authority — are completely exempt from GST. On a ₹75 lakh under-construction flat, that 5% GST adds ₹3.75 lakh to your bill before you've even signed the loan documents.

This is not a small number. It's money you pay to the government and never get back, unlike stamp duty which at least forms part of the registered property value.

The Double Payment Trap: EMI Plus Rent

This is the single biggest financial burden that catches buyers off guard. When you take a home loan for an under-construction property, the bank typically disburses funds in tranches linked to construction milestones. During the construction period, many lenders charge "pre-EMI" — interest only on the amount disbursed. Once full disbursement happens, regular EMI kicks in. Throughout all of this, you're still paying rent for the place you're currently living in.

Assume you're renting at ₹20,000 per month and your full EMI on the ₹75 lakh loan (at 8.75% for 20 years) works out to approximately ₹65,800 per month. Over a 36-month construction period, you're paying close to ₹85,800 per month in combined housing costs — nearly ₹31 lakh in total outflow just on rent and loan repayment before you even get keys. Use CalcPhi's Home Loan EMI Calculator to model exactly what your EMI will be at current rates, and factor that against your expected rent duration.

Ready-to-move buyers have none of this burden. Their loan starts, they move in, and one payment replaces the other from day one.

Side-by-Side: Total Cost Comparison Over 3 Years

The table below uses a realistic scenario — under-construction at ₹75 lakh vs ready-to-move at ₹95 lakh, same locality, 36-month construction timeline, ₹20,000 monthly rent, 8.75% home loan rate on 80% LTV.

| Cost Component | Under-Construction (₹75L) | Ready-to-Move (₹95L) |

|---|---|---|

| Agreement value | ₹75,00,000 | ₹95,00,000 |

| GST (5% / 0%) | ₹3,75,000 | ₹0 |

| Stamp duty + registration (~7%) | ₹5,25,000 | ₹6,65,000 |

| Rent paid during wait (₹20k × 36 months) | ₹7,20,000 | ₹0 |

| Pre-EMI / EMI paid pre-possession | ~₹19,44,000 | ₹0 |

| Total outflow (3-year window) | ~₹1,10,64,000 | ~₹1,01,65,000 |

The under-construction flat costs approximately ₹9 lakh more over the three-year horizon — despite being ₹20 lakh cheaper on the agreement. If possession is delayed by even 12 months (which, as we'll see below, is extremely common), that gap widens by another ₹5–6 lakh.

Delay Risk: The Factor That Derails Most UC Calculations

According to ANAROCK Research, over 40% of under-construction projects across India's top seven cities experience possession delays exceeding 12 months. Even among reputed Tier-1 developers, the delay rate hovers between 15–20%. Regulatory clearances, labour disruptions, environmental holds, and financing gaps are the most common culprits.

RERA (Real Estate Regulatory Authority) provides legal protection. If possession is delayed beyond the committed date, the builder is required to pay you interest at SBI MCLR plus 2% on every rupee you've paid. In practice, collecting this compensation requires filing a complaint with your state RERA portal (such as rera.maharashtra.gov.in for Maharashtra or karnataka-rera.com for Karnataka) and following through on the process. Compensation is your right, but it's not automatic.

Before booking any under-construction project, verify its RERA registration number on the state portal, check the builder's track record on previous projects, and confirm that the bank is disbursing directly to the project escrow account (as required under RERA, 70% of collected funds must be parked in a project-specific account).

Tax Benefits: Where Under-Construction Buyers Face an Extra Hurdle

Home loan borrowers get two key income tax deductions: up to ₹2 lakh per year on interest under Section 24(b), and up to ₹1.5 lakh per year on principal under Section 80C. However, the Section 24(b) interest deduction for under-construction properties works differently.

The interest you pay during the construction period — what's called "pre-construction interest" — cannot be deducted in the year it's paid. Instead, it's pooled and then deducted in five equal instalments starting from the financial year in which you receive possession. This means you miss out on the tax benefit during the exact years you're paying the most in double payments.

Ready-to-move buyers, by contrast, get to claim Section 24(b) from the very first EMI. Use CalcPhi's Home Loan Tax Benefit Calculator to calculate exactly how much tax you'd save under both scenarios — it factors in your income, tax regime, and loan details to give a precise number.

When Under-Construction Actually Makes Financial Sense

Despite the risks, there are specific situations where going under-construction is the smarter financial move.

If you currently live rent-free — in your parents' home, for example — the double-payment problem largely disappears. You eliminate ₹7.2 lakh in rent from the equation, and the UC flat's lower entry price starts to look genuinely attractive, particularly in high-growth corridors where appreciation during the construction period can be significant.

Investors who don't need to occupy the property also benefit differently. There's no rent to pay, the pre-construction capital appreciation can be real (especially in projects in emerging micro-markets), and the lower entry price generates a better return on investment if the property is eventually sold.

First-time buyers using a construction-linked payment plan (CLP) can also manage cash flow better — you don't pay the full amount upfront, which means your loan disbursal (and EMI) is lower in the early months. This staged outflow can work well for those who are still building their down payment while the project is under construction.

The builder's reputation and project profile matter enormously here. Developers like Godrej Properties, Prestige Group, Sobha, Lodha, and Tata Housing have stronger on-time delivery records than smaller regional builders. A top-tier builder's UC project in a growth location can be a genuinely sound financial decision. A smaller builder's UC project with a shaky RERA record is a different proposition entirely.

Capital Appreciation: Does Under-Construction Have the Edge?

Theoretically, under-construction properties offer appreciation during the construction period itself — you lock in today's price and the property's market value rises over two to three years. In a market with strong demand (Bengaluru's north corridor, Hyderabad's outer ring road, Navi Mumbai, Pune's Wakad-Hinjewadi belt), this can add meaningful value.

In practice, the appreciation argument works best for investors with long time horizons and no rent burden. For an end-user, the capital appreciation needs to significantly outpace the extra costs incurred — the double payments, GST, and risk premium — before the UC option comes out ahead.

Ready-to-move properties, particularly in completed projects that have been around for a year or two, sometimes carry negotiation potential. Old inventory that builders are holding can often be purchased at a discount, especially in a slow market.

Ready-to-Move: The Advantages Beyond Cost

RTM properties eliminate uncertainty in ways that extend beyond just money. What you see is what you get — the exact flat, the actual construction quality, the views, the society, the amenities, the neighbourhood. There are no specification changes mid-project, no material downgrades, and no surprise layout alterations.

Home loans for ready-to-move properties are also cleaner to structure. Full disbursement happens on registration, regular EMIs start immediately, and there's no pre-EMI or tranche disbursement complexity. Some lenders also offer marginally better rates on completed properties compared to under-construction loans.

For buyers who have children in school, elderly parents, or specific professional commitments that make immediate occupancy non-negotiable, RTM is often the only practical option regardless of the financial comparison.

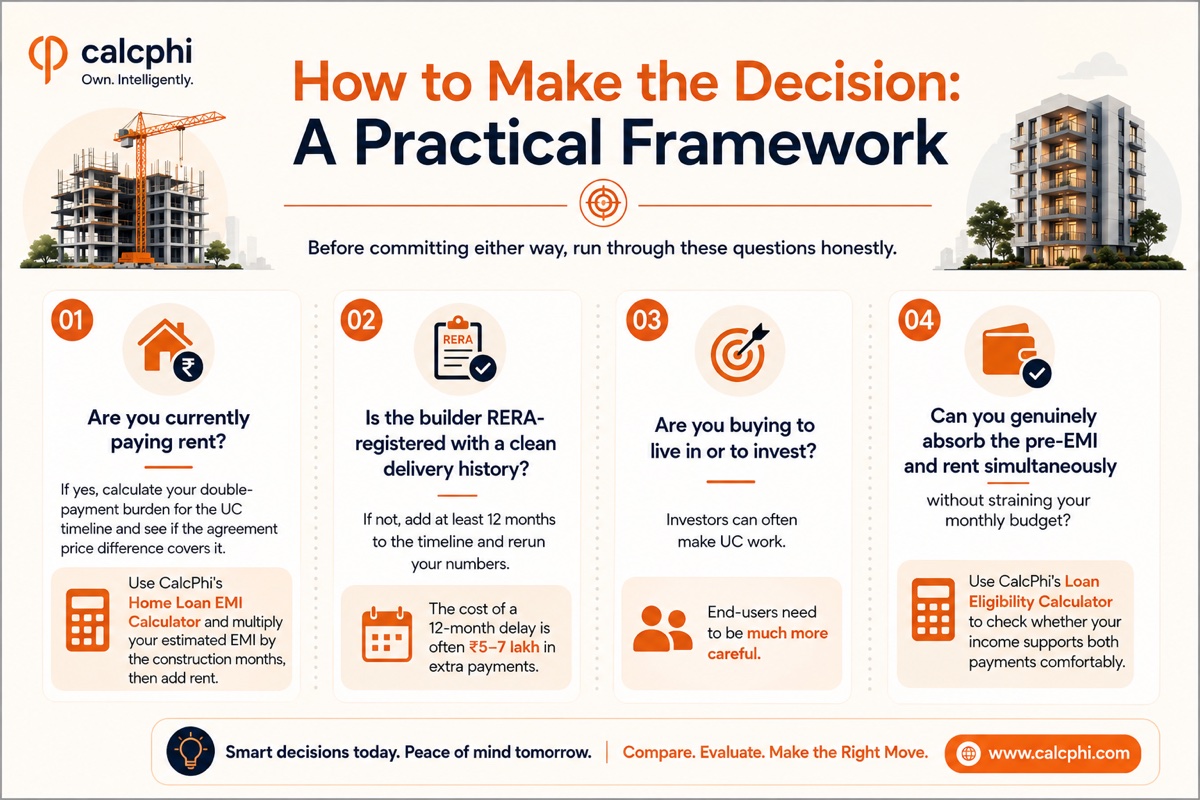

How to Make the Decision: A Practical Framework

Before committing either way, run through these questions honestly.

Are you currently paying rent? If yes, calculate your double-payment burden for the UC timeline and see if the agreement price difference covers it. Use CalcPhi's Home Loan EMI Calculator and multiply your estimated EMI by the construction months, then add rent.

Is the builder RERA-registered with a clean delivery history? If not, add at least 12 months to the timeline and rerun your numbers. The cost of a 12-month delay is often ₹5–7 lakh in extra payments.

Are you buying to live in or to invest? Investors can often make UC work. End-users need to be much more careful.

Can you genuinely absorb the pre-EMI and rent simultaneously without straining your monthly budget? Use CalcPhi's Loan Eligibility Calculator to check whether your income supports both payments comfortably.

Model your property purchase cost:

Home Loan EMI Calculator → Tax Benefit Calculator → Loan Eligibility →

Frequently Asked Questions

Is GST applicable on ready-to-move flats in India?

No. GST is applicable only on under-construction properties — at 5% for regular housing and 1% for affordable housing (below ₹45 lakh in specified cities). Once a builder obtains a completion certificate from the local municipal authority, the property is classified as ready-to-move, and all sales after that point are fully exempt from GST. This saving can be substantial — on a ₹1 crore property, it amounts to ₹5 lakh.

Can I claim home loan tax benefits during the construction period?

You can claim the principal repayment under Section 80C during construction, but the interest deduction under Section 24(b) is deferred. The total interest paid during the construction period (pre-construction interest) is aggregated and then deducted in five equal annual instalments starting from the year you receive possession. This means under-construction buyers miss out on the immediate interest deduction that RTM buyers enjoy.

What happens if my builder delays possession beyond the RERA date?

Under RERA, the builder is legally obligated to pay you interest at SBI MCLR plus 2% on all amounts paid if possession is delayed beyond the RERA-registered date. You can file a complaint on your state RERA portal. In practice, this process takes time and persistence, but thousands of buyers have successfully recovered compensation. Always keep all payment receipts and demand letters as documentation.

How much appreciation can I realistically expect from an under-construction property?

This varies enormously by location and market conditions. In high-demand corridors like Bengaluru's Whitefield, Hyderabad's Gachibowli, or Navi Mumbai's Kharghar, UC properties have historically appreciated 10–20% during the construction period. In slower markets or with less reputed builders, appreciation may be flat or even negative if the project stalls. Never factor in appreciation as a certainty — build your financial case on costs alone, and treat appreciation as upside.

Which is better for a first-time home buyer — under-construction or ready-to-move?

For most first-time buyers who are paying rent and have limited savings buffers, ready-to-move is the lower-risk choice. The elimination of GST, the immediate tax benefit on interest, and the certainty of what you're buying are significant advantages. If you are living rent-free and buying in an early-stage growth corridor with a reputed builder, under-construction can work — but model the numbers carefully before committing.

Does the home loan process differ between UC and RTM properties?

Yes. For RTM properties, the bank disburses the full loan amount on registration and EMIs begin immediately. For UC properties, the bank disburses in tranches linked to construction milestones, and you pay pre-EMI (interest only on the disbursed amount) until full disbursement. The total interest paid over the loan's life is higher for UC loans because of this structure. Some banks also charge a slightly higher processing fee or rate for under-construction loans.

Disclaimer: All figures in this article are illustrative estimates based on publicly available rates and typical market conditions as of 2026. CalcPhi's calculators are for educational and estimation purposes only. Nothing in this article constitutes financial, legal, or investment advice. Consult a SEBI-registered financial advisor, a qualified CA, or a legal professional before making any property purchase decision.