SIP vs FD: Which Is Better for Indian Investors in 2026?

You have ₹10,000 sitting in your salary account every month. A friend says put it in an FD — safe, guaranteed, no stress. Another says start a SIP — the market has made people wealthy. Both are right in their own way. But which one is actually better for you, given where India's economy stands in 2026? This guide breaks down SIP vs FD across every dimension that matters — returns, tax, risk, liquidity, and long-term wealth creation — so you can make an informed decision based on real numbers.

What Is a SIP and How Does It Work?

A SIP (Systematic Investment Plan) is a method of investing a fixed amount into a mutual fund at regular intervals — usually monthly. When you start a SIP, your money buys units of a mutual fund at whatever the current NAV (Net Asset Value) happens to be that day. When markets are down, you buy more units. When markets are up, you buy fewer. Over time, this averages out your purchase cost — a concept called rupee cost averaging. SIPs are regulated by SEBI and can be started with as little as ₹100 per month.

See how much your monthly SIP could grow over 10 or 20 years — enter your monthly amount, expected return rate, and time horizon.

SIP Calculator →What Is an FD and How Does It Work?

An FD (Fixed Deposit) is a savings instrument offered by banks and post offices where you deposit a lump sum for a fixed period and earn a guaranteed interest rate. Unlike a SIP, the returns on an FD are completely predictable from day one — you know exactly how much you will receive at maturity. Most major Indian banks offer FD rates ranging from 6.5% to 7.5% per annum for general citizens in 2026. Senior citizens typically receive an additional 0.25% to 0.50%.

Calculate exactly how much your deposit will grow — accounting for quarterly compounding and TDS — so there are no surprises at maturity.

FD Calculator →SIP vs FD: A Side-by-Side Comparison

Investing ₹10,000 per month for 10 years: a SIP at an assumed 12% CAGR grows to approximately ₹23.2 lakhs against a total investment of ₹12 lakhs. The RD/FD route at 7% yields approximately ₹17.4 lakhs on the same investment — a difference of nearly ₹5.8 lakhs. That gap widens significantly over 15 or 20 years due to compounding. However, the 12% from SIP is market-linked and historical, not guaranteed. The 7% from FD is locked in from day one.

| Horizon | FD / RD at 7% (quarterly compound) | SIP at 10% CAGR | SIP at 12% CAGR |

|---|---|---|---|

| 3 years | ₹4.01L | ₹4.19L | ₹4.35L |

| 5 years | ₹7.31L | ₹7.74L | ₹8.17L |

| 10 years | ₹17.4L | ₹20.5L | ₹23.2L |

| 15 years | ₹32.6L | ₹41.8L | ₹50.5L |

| 20 years | ₹54.8L | ₹76.6L | ₹98.9L |

Risk: The Fundamental Difference

An FD carries virtually zero market risk. Your principal is protected, the interest rate is fixed, and as long as your bank is covered under DICGC, deposits up to ₹5 lakh per bank are insured.

A SIP in an equity mutual fund, by contrast, is subject to market risk. In a bad year — say 2020 or 2022 — your SIP portfolio could be in the red for months. There have been periods in Indian market history where even 5-year SIP returns were negative. If you cannot tolerate watching your portfolio value dip, a 100% SIP allocation will cause anxiety and lead to premature withdrawals at the worst possible time.

Tax Treatment: Where FDs Lose Ground

FD taxation: Interest earned on FDs is added to your total income and taxed at your applicable slab rate. If you are in the 30% tax bracket and earn ₹50,000 as FD interest in a year, you pay ₹15,000 in tax on that interest. Banks also deduct TDS at 10% once your annual FD interest crosses ₹40,000 (₹50,000 for senior citizens).

Equity mutual fund taxation (SIP): Under the current rules for AY 2026-27, long-term capital gains (LTCG) on equity mutual funds held for more than 12 months are taxed at 12.5% on gains exceeding ₹1.25 lakh per financial year. Short-term capital gains are taxed at 20%. For most long-term SIP investors, the effective tax on returns is significantly lower than the slab-based tax on FD interest.

| Scenario | SIP (Equity MF) | FD |

|---|---|---|

| Gross return p.a. | 12% | 7.5% |

| Tax rate on gains | 12.5% LTCG (above ₹1.25L exemption) | 30% income tax |

| Effective after-tax return | ~11.2% | ~5.25% |

| Post-tax corpus (20 years) | ~₹93L | ~₹45L |

For tax-saving investors, ELSS mutual funds also provide a deduction of up to ₹1.5 lakh under Section 80C with only a 3-year lock-in.

Use CalcPhi's ELSS Calculator to see both your investment growth and your 80C tax savings side by side.

ELSS Calculator → Income Tax Calculator →Liquidity: Which One Gives You Access to Your Money?

FDs are moderately liquid. You can break an FD prematurely, but banks typically charge a penalty of 0.5% to 1% on the applicable interest rate. Tax-saver FDs (5-year lock-in) cannot be broken at all before maturity without forfeiting the 80C benefit.

SIPs in open-ended equity mutual funds are highly liquid. There is no lock-in period (except for ELSS funds), and redemptions are typically processed within 2–3 business days. You can also stop or pause your SIP at any time without penalty. This flexibility makes SIPs far more suited to investors who may need access to funds in an emergency.

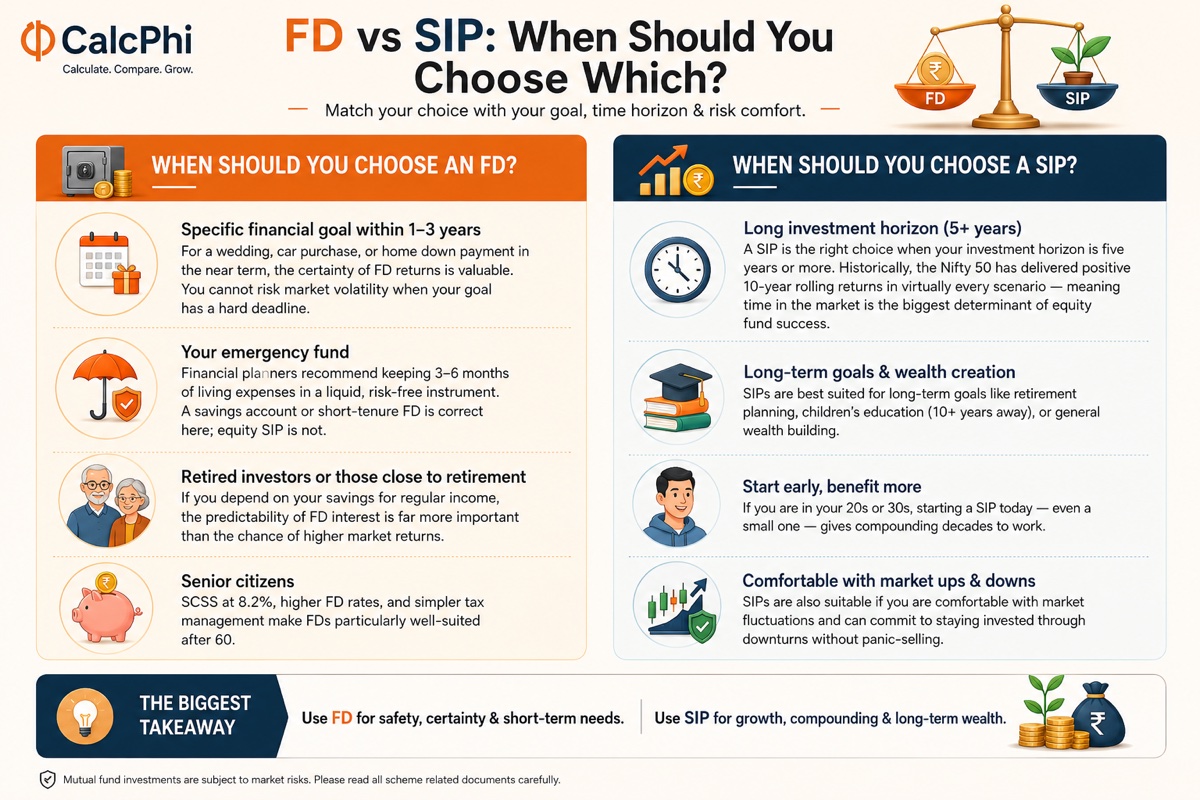

When Should You Choose an FD?

- Specific financial goal within 1–3 years: For a wedding, car purchase, or home down payment in the near term, the certainty of FD returns is valuable. You cannot risk market volatility when your goal has a hard deadline.

- Your emergency fund: Financial planners recommend keeping 3–6 months of living expenses in a liquid, risk-free instrument. A savings account or short-tenure FD is correct here; equity SIP is not.

- Retired investors or those close to retirement: If you depend on your savings for regular income, the predictability of FD interest is far more important than the chance of higher market returns.

- Senior citizens: SCSS at 8.2%, higher FD rates, and simpler tax management make FDs particularly well-suited after 60.

When Should You Choose a SIP?

A SIP is the right choice when your investment horizon is five years or more. Historically, the Nifty 50 has delivered positive 10-year rolling returns in virtually every scenario — meaning time in the market is the biggest determinant of equity fund success.

SIPs are best suited for long-term goals like retirement planning, children's education (10+ years away), or general wealth building. If you are in your 20s or 30s, starting a SIP today — even a small one — gives compounding decades to work. SIPs are also suitable if you are comfortable with market fluctuations and can commit to staying invested through downturns without panic-selling. The biggest risk in equity investing is not the market — it is the investor's own behaviour.

See how increasing your SIP amount by just 10% every year dramatically accelerates your wealth over 15–20 years.

Step-Up SIP Calculator →The Best Approach: Use Both

SIP vs FD is not an either/or decision for most Indian investors. The right strategy is to use both, based on what your money is for. A practical allocation for a 35-year-old salaried professional with moderate risk tolerance:

- Keep 3–6 months of expenses in a savings account or liquid FD for emergencies

- Invest in FDs for goals that are 1–3 years away

- Direct 60–70% of your monthly surplus into SIPs for long-term goals (retirement, children's education)

- Use ELSS specifically if you have not exhausted your Section 80C limit

This approach gives you the safety net of guaranteed returns alongside the wealth-creation engine of equity markets.

SIP vs FD at a Glance

| Feature | SIP (Equity Mutual Fund) | Fixed Deposit |

|---|---|---|

| Returns | Market-linked (10–14% historical CAGR) | Guaranteed (6.5–7.5% in 2026) |

| Risk | Moderate to High | Very Low |

| Liquidity | High (2–3 days) | Moderate (penalty on early break) |

| Tax on gains | 12.5% LTCG / 20% STCG | Slab rate (up to 30%) |

| Minimum investment | ₹100/month | ₹1,000 (most banks) |

| Best for | Long-term wealth (5+ years) | Short-term goals, capital protection |

| Inflation-beating? | Yes, historically | Marginal (barely above 6–7% CPI) |

| Regulatory oversight | SEBI | RBI / DICGC |

Frequently Asked Questions

Is SIP better than FD for 5 years?

For a 5-year horizon, SIP in equity mutual funds has historically outperformed FDs, but with greater volatility. If the 5-year goal is flexible and you can hold on for an extra year or two if markets dip, a SIP is likely to deliver better after-tax returns. If the goal has a hard deadline (like a home purchase in exactly 5 years), a hybrid approach — SIP for the first 3 years, then shifting to FD — reduces risk near the goal date.

Is SIP safe for long-term investment in India?

SIPs in diversified equity mutual funds are considered a reasonable long-term investment option in India, though they are not risk-free. Market risk is real, and short-term returns can be negative. However, over 10+ year periods, well-diversified equity funds regulated by SEBI have historically delivered positive inflation-adjusted returns. The probability of negative returns decreases significantly with time.

How much tax do I pay on SIP returns vs FD interest?

FD interest is taxed at your income tax slab rate — up to 30% for high earners. Equity mutual fund gains held for more than 12 months are taxed at 12.5% LTCG above a ₹1.25 lakh annual exemption. For someone in the 30% tax bracket, this difference in tax treatment means a SIP is often more tax-efficient than an FD over the long term, even if the pre-tax returns were identical.

Can I start a SIP with ₹500 per month?

Yes, many mutual funds in India allow SIPs starting at ₹100 to ₹500 per month. There is no excuse to delay starting because the amount feels small — ₹500/month at 12% CAGR over 20 years grows to over ₹4.99 lakhs. The habit of investing regularly matters more than the starting amount.

What happens to my FD if a bank fails?

Under DICGC insurance, deposits of up to ₹5 lakh per depositor per bank are insured, including both principal and interest. If your FD balance exceeds ₹5 lakh in a single bank, the excess is uninsured. To avoid this risk, distribute large FD amounts across multiple banks or consider government-backed options like Post Office Time Deposits, which carry sovereign guarantee.

Which is better for tax saving — SIP or FD?

ELSS (Equity Linked Savings Scheme), accessible via SIP, is superior to Tax-Saver FDs for most investors. ELSS has a 3-year lock-in (vs 5 years for Tax-Saver FD), historical returns of 12–15% CAGR (vs 6.5–7.5% for FD), and the same ₹1.5 lakh deduction under Section 80C. The only advantage of a Tax-Saver FD is the guaranteed return — relevant if you cannot tolerate any market risk.

Disclaimer: The information in this article is for educational and estimation purposes only. All figures, return assumptions, and tax references are based on data available as of AY 2026-27 and are subject to change. SIP returns shown are based on historical data and are not guaranteed. CalcPhi calculators are estimation tools and do not constitute financial advice. Please consult a SEBI-registered financial advisor or qualified CA before making investment decisions based on your personal financial situation.