Senior Citizen Savings Scheme vs FD: The Best Option After 60 in 2026

You have just crossed 60. The EPF corpus has arrived, the gratuity cheque has cleared, and you are staring at perhaps the largest sum of money you have ever held at one time. The question is immediate and real: where does it go?

Two options come up in almost every retirement conversation in India — the Senior Citizen Savings Scheme (SCSS) and bank Fixed Deposits. Both are low-risk and both offer predictable income, but they are not the same product. The difference in interest rates, tax treatment, investment limits, and safety nets can translate to lakhs of rupees over a five-year period. This guide breaks down every dimension so you can make the right call — or more likely, the right combination.

What Is the Senior Citizen Savings Scheme?

SCSS is a government-backed savings scheme specifically designed for people aged 60 and above. It is operated through post offices and most nationalised banks across India. You deposit a lump sum, and the government pays you interest every quarter — automatically, without you having to do anything.

The current SCSS interest rate for Q1 FY 2026-27 is 8.2% per annum, paid quarterly. This rate is set by the Ministry of Finance and reviewed every quarter, though it has remained stable at 8.2% since early 2023. The maximum you can invest as an individual is ₹30 lakh, raised from ₹15 lakh in Budget 2023. If both spouses are eligible, each can open their own account, effectively allowing a couple to park ₹60 lakh in SCSS.

The tenure is five years with a one-time extension of three years available. You can open an SCSS account at any post office, SBI, and most public sector banks like Punjab National Bank, Bank of Baroda, and Canara Bank — as well as private banks including ICICI Bank and HDFC Bank.

What Are Senior Citizen FD Rates in 2026?

Fixed deposits for senior citizens typically carry an extra 0.25% to 0.50% over regular FD rates as a standard benefit extended by most banks. For the current FY 2026-27, major bank rates look approximately like this:

| Bank | Senior Citizen FD Rate (1–5 years) |

|---|---|

| SBI | 7.25%–7.50% p.a. |

| HDFC Bank | 7.40%–7.75% p.a. |

| ICICI Bank | 7.40%–7.75% p.a. |

| Axis Bank | 7.50%–7.75% p.a. |

| Ujjivan Small Finance Bank | 8.75%–9.00% p.a. |

| AU Small Finance Bank | 8.50%–8.75% p.a. |

Large PSU and private banks hover between 7.25% and 7.75% for senior citizens. Small finance banks push rates to 8.5%–9%, which is higher than SCSS — but with a critical difference in the safety net, which we will cover shortly.

Want to calculate exactly how much your FD will earn after five years? Use CalcPhi's Senior Citizen FD Calculator — it factors in the 0.5% senior citizen premium and shows you quarterly and cumulative payout options side by side.

Head-to-Head: SCSS vs Senior Citizen FD

| Feature | SCSS | Senior Citizen FD (Large Bank) | Small Finance Bank FD |

|---|---|---|---|

| Interest rate | 8.2% p.a. | 7.25%–7.75% p.a. | 8.5%–9.0% p.a. |

| Maximum investment | ₹30 lakh per person | No limit | No limit |

| Interest payment | Quarterly (mandatory) | Monthly / quarterly / cumulative | Monthly / quarterly / cumulative |

| Tenure | 5 years + 3 year extension | 7 days to 10 years | 7 days to 10 years |

| Premature withdrawal | Allowed with penalty | Allowed with penalty | Allowed with penalty |

| Deposit insurance | Sovereign guarantee | DICGC: ₹5 lakh per bank | DICGC: ₹5 lakh per bank |

| TDS threshold | ₹50,000/year interest | ₹50,000/year (senior citizen limit) | ₹50,000/year interest |

The interest rate comparison tells most of the story. SCSS at 8.2% beats every large bank's senior citizen FD rate. The only instruments that beat SCSS are small finance bank FDs — and their advantage comes with a meaningful safety trade-off.

The Income Numbers: ₹30 Lakh at Retirement

Let us run the actual math. For someone depositing ₹30 lakh (the SCSS maximum):

| Scheme | Rate | Quarterly Income | Annual Income | 5-Year Total Income |

|---|---|---|---|---|

| SCSS | 8.2% | ₹61,500 | ₹2,46,000 | ₹12,30,000 |

| SBI Senior Citizen FD | 7.5% | ₹56,250 | ₹2,25,000 | ₹11,25,000 |

| HDFC/ICICI Senior Citizen FD | 7.75% | ₹58,125 | ₹2,32,500 | ₹11,62,500 |

| AU Small Finance Bank FD | 8.75% | ₹65,625 | ₹2,62,500 | ₹13,12,500 |

SCSS pays ₹21,000 more per year than SBI's senior citizen FD on a ₹30 lakh investment — roughly ₹1,05,000 extra over five years. That is genuinely meaningful for a retiree relying on fixed income.

The only option that earns more is a small finance bank FD. But that extra income comes with a significant risk: the Deposit Insurance and Credit Guarantee Corporation (DICGC) only insures ₹5 lakh per depositor per bank. Parking ₹30 lakh in a small finance bank exposes ₹25 lakh to institutional risk — something that is hard to stomach on retirement savings.

Eligibility Rules You Must Know

SCSS eligibility is more specific than people realise. Here are the key rules.

Individuals aged 60 years and above can open an SCSS account at any time. There is no deadline. Individuals aged 55 to 60 who have taken Voluntary Retirement Scheme (VRS) or superannuation can also open an SCSS account, but only within one month of receiving their retirement benefits. Miss that one-month window, and you lose eligibility until you turn 60. Defence service personnel who retire early can open an SCSS account at age 50, again within one month of receiving benefits.

The amount deposited in SCSS cannot exceed the retirement benefits received. If you received ₹28 lakh from EPF and gratuity combined, your SCSS deposit cannot exceed ₹28 lakh even though the ceiling is ₹30 lakh.

Premature Withdrawal: What the Penalties Look Like

Both SCSS and FDs allow early withdrawal, but the penalties differ.

For SCSS, if you close the account before one year, no interest is paid — in fact, any interest already disbursed is recovered. Between one and two years, a penalty of 1.5% on the principal is deducted. Between two and five years, the penalty is 1% on the principal. After five years (during the three-year extension), the penalty is 1% on the principal if you close before the extended maturity.

For bank FDs, the standard penalty across most banks is 0.5% to 1% below the applicable rate for the period you held the deposit. So if you break a five-year FD after two years, you get the two-year rate minus the penalty — which is typically less severe than SCSS's flat penalty in the first two years.

If liquidity is important to you — for example, if you might need the corpus for a medical emergency — bank FDs offer more flexibility without as steep a cost for early exit.

Tax Treatment: The 80TTB Advantage

Both SCSS and FD interest are fully taxable at your applicable income tax slab rate. Neither instrument offers a tax deduction on the principal under Section 80C anymore for new deposits.

However, both qualify for the Section 80TTB deduction — a provision exclusively for senior citizens that allows a deduction of up to ₹50,000 per financial year on interest income from savings accounts, fixed deposits, recurring deposits, and post office deposits. This is available only under the old tax regime; if you have opted for the new regime, 80TTB does not apply.

TDS is deducted by the post office or bank if your total interest from that institution crosses ₹50,000 in a financial year (this higher limit applies specifically to senior citizens; the regular limit is ₹40,000). If your total income is below the taxable threshold, you can submit Form 15H to prevent TDS deduction altogether.

Use CalcPhi's TDS on FD Calculator to estimate your net payout after TDS, and CalcPhi's Income Tax Calculator to see how interest income affects your total tax liability under both regimes.

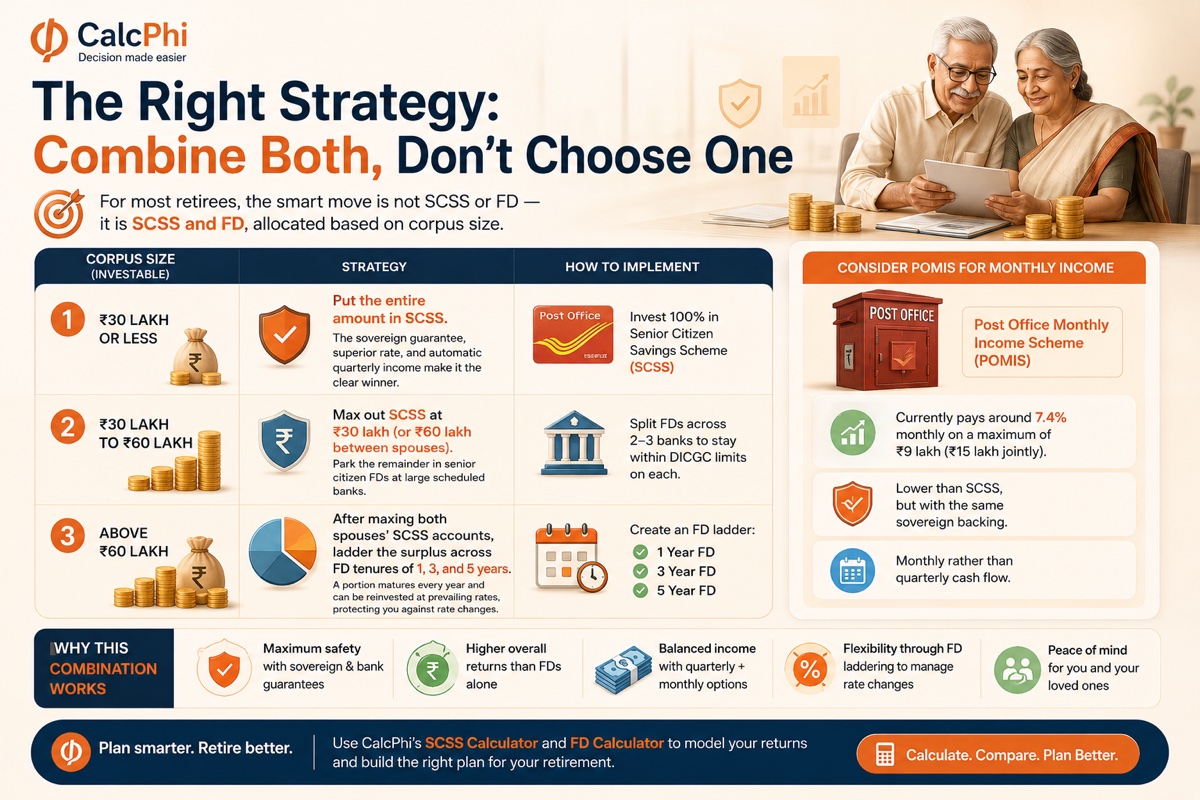

The Right Strategy: Combine Both, Don't Choose One

For most retirees, the smart move is not SCSS or FD — it is SCSS and FD, allocated based on corpus size. Here is a framework.

If your investable corpus is ₹30 lakh or less: Put the entire amount in SCSS. The sovereign guarantee, superior rate, and automatic quarterly income make it the clear winner.

If your corpus is between ₹30 lakh and ₹60 lakh: Max out SCSS at ₹30 lakh (or ₹60 lakh between spouses). Park the remainder in senior citizen FDs at large scheduled banks like SBI, HDFC, or ICICI — split across two or three banks to stay within DICGC limits on each.

If your corpus exceeds ₹60 lakh: After maxing both spouses' SCSS accounts, consider laddering the surplus across FD tenures of 1, 3, and 5 years. This way, a portion matures every year and can be reinvested at prevailing rates, protecting you against rate changes. Explore CalcPhi's SCSS Calculator and FD Calculator to model exactly what each scenario returns over your chosen time horizon.

A small allocation to Post Office Monthly Income Scheme (POMIS) is also worth considering if you prefer monthly payments over SCSS's quarterly cycle. POMIS currently pays around 7.4% monthly on a maximum of ₹9 lakh (₹15 lakh jointly) — lower than SCSS but with the same sovereign backing and monthly rather than quarterly cash flow.

Frequently Asked Questions

Is SCSS better than FD for senior citizens in 2026?

For amounts up to ₹30 lakh, SCSS is almost always the better option in 2026. It pays 8.2% compared to 7.25%–7.75% from most large banks, and it carries a sovereign guarantee from the Government of India rather than just DICGC insurance capped at ₹5 lakh. The only exception is if you need flexibility to withdraw early or want a tenor shorter than five years, where FDs offer more options.

Can husband and wife both open SCSS accounts?

Yes. Each individual has a separate ₹30 lakh limit in SCSS. A couple can therefore invest a combined ₹60 lakh across their individual accounts. Joint accounts are allowed, but the maximum limit applies to the first account holder — so a joint account still counts toward the first holder's ₹30 lakh ceiling.

Is SCSS interest taxable?

Yes, SCSS interest is fully taxable at your applicable slab rate. However, senior citizens can claim a deduction of up to ₹50,000 per year on interest income under Section 80TTB, available under the old tax regime. TDS is deducted at 10% if annual interest from an institution crosses ₹50,000. Submit Form 15H if your total income is below the taxable limit to avoid TDS deduction at source.

What happens to my SCSS account after five years?

After the five-year maturity, you can extend the SCSS account for one additional block of three years by submitting an application within one year of maturity. During this extension period, the interest rate applicable at the time of extension applies — not the rate from your original deposit. If you do not extend or withdraw, the account earns post office savings account interest (currently around 4%) on the balance until you close it.

Can I open an SCSS account at a private bank?

Yes. SCSS accounts can be opened at ICICI Bank, HDFC Bank, and Axis Bank in addition to all post offices and public sector banks. The terms, interest rate, and government guarantee are identical regardless of where you open the account, since SCSS is a government scheme administered through authorised banks.

What is the minimum amount to open an SCSS account?

The minimum deposit for SCSS is ₹1,000. The maximum is ₹30 lakh. Deposits must be made in multiples of ₹1,000. Unlike FDs, you cannot add money to an existing SCSS account — each deposit creates a separate account, and all your SCSS account balances combined cannot exceed ₹30 lakh per individual.

Disclaimer: The figures in this article are based on SCSS interest rates and bank FD rates as of Q1 FY 2026-27 and are subject to change. CalcPhi calculators are for educational and estimation purposes only. Nothing in this article constitutes personalised financial advice. Please consult a SEBI-registered investment advisor or a Certified Financial Planner (CFP) before making investment decisions.