How to Calculate Real ROI on Rental Property in India — Beyond the Gross Yield

Walk into any property expo in Bengaluru, Hyderabad, or Pune and the sales team will greet you with a laminated sheet showing "rental yield: 3.5 to 4%." That number is real — but it is also deeply misleading. Gross rental yield is a starting point, not a finish line. By the time you account for vacancy periods, maintenance costs, property tax, brokerage, and income tax on rent, many properties in India's major metros deliver a net yield closer to 1.5 to 2%.

Why Gross Yield Is Not Enough

Gross rental yield is calculated by dividing the annual rent by the property's purchase price. If you bought a flat for ₹70 lakh and charge ₹22,000 per month in rent, your gross yield is ₹2,64,000 ÷ ₹70,00,000 = 3.77%. Simple, clean, and completely insufficient for making an investment decision.

Gross yield treats your rental property as if tenants stay forever, maintenance costs nothing, the government takes no share, and the flat is always occupied. None of those things are true. The real ROI — what actually lands in your bank account after every cost and deduction — is called net rental yield, and it requires a more careful calculation.

Over a 15-year holding period, the gap between a 3.8% gross yield and a 1.9% net yield on a ₹70 lakh property amounts to roughly ₹19.95 lakh in "missing" income that most landlords never see because they never accounted for it in the first place.

Step 1 — Start With Gross Rental Income

The starting point is straightforward: how much rent does the property generate in a full year if it is always occupied?

Formula: Gross Annual Rent = Monthly Rent × 12

For example, a 2BHK flat in Whitefield, Bengaluru purchased for ₹85 lakh, currently rented at ₹24,000 per month:

Gross Annual Rent = ₹24,000 × 12 = ₹2,88,000

Gross Yield = ₹2,88,000 ÷ ₹85,00,000 = 3.39%

This is the number your broker will show you. Now let us find out what you actually keep.

Step 2 — Deduct Vacancy Loss

Rental properties in India are rarely occupied 365 days a year. Tenants give notice, move out, and the landlord needs time to find a replacement. In most Indian metros, a realistic vacancy allowance is one to two months per year — roughly 8 to 17% of gross rent. For tier-2 cities and less sought-after localities, vacancy can run even higher.

In our Bengaluru example, assume a conservative 1.5 months of vacancy per year:

Vacancy Loss = ₹24,000 × 1.5 = ₹36,000

Effective Annual Rent = ₹2,88,000 − ₹36,000 = ₹2,52,000

If you are evaluating a property and want to stress-test your vacancy assumptions, CalcPhi's Rental Yield Calculator lets you plug in different vacancy rates and see how they affect your net income instantly.

Step 3 — Subtract Operating Costs

This is the part most landlords either forget or dramatically underestimate. Several real, recurring costs come directly out of rental income.

Society Maintenance (Owner's Share)

Most housing societies charge maintenance fees. A portion is covered by the tenant, but the owner typically pays for the building's capital expenditure fund, major repairs, and sinking fund contributions. For a mid-range 2BHK, this can run ₹1,200 to ₹2,500 per month, or ₹14,400 to ₹30,000 per year.

Property Tax (Municipal Tax)

Every property in India attracts annual property tax payable to the local municipal body — BBMP in Bengaluru, MCGM in Mumbai, GHMC in Hyderabad. For a typical urban apartment in a major city, expect ₹8,000 to ₹20,000 per year.

Repairs and Maintenance

Appliances break, paint fades, plumbing develops issues. A practical estimate is ₹15,000 to ₹25,000 per year in amortised costs, assuming a full repaint every four to five years at roughly ₹35,000 to ₹60,000.

Brokerage

Unless you find tenants through personal contacts every time, you will pay a broker one month's rent per new tenant agreement. Amortised over a typical two to three year tenancy cycle, this works out to roughly half a month's rent per year — around ₹12,000 annually in our example.

| Operating Cost | Annual Amount |

|---|---|

| Society maintenance (owner's share) | ₹18,000 |

| Property tax (BBMP estimate) | ₹12,000 |

| Repairs and maintenance | ₹18,000 |

| Brokerage (amortised) | ₹12,000 |

| Total Operating Costs | ₹60,000 |

Net Income Before Tax = ₹2,52,000 − ₹60,000 = ₹1,92,000

Step 4 — Account for Income Tax on Rental Income

Rental income in India is taxed under the head "Income from House Property." The Income Tax Act gives landlords a flat 30% standard deduction on Net Annual Value (NAV) — this is meant to account for repairs and depreciation, and you get it automatically without needing to submit any bills.

Step 4a — Calculate Net Annual Value (NAV)

NAV = Annual Rent Received − Municipal Tax Paid

NAV = ₹2,52,000 − ₹12,000 = ₹2,40,000

Step 4b — Apply 30% Standard Deduction

Standard Deduction = 30% of ₹2,40,000 = ₹72,000

Step 4c — Deduct Home Loan Interest (if applicable)

If the property is financed, you can deduct the entire home loan interest under Section 24(b) for let-out property — there is no ₹2 lakh ceiling that applies to self-occupied homes. For our example, assume the property is owned outright (no loan).

Taxable Income from House Property = ₹2,40,000 − ₹72,000 = ₹1,68,000

Tax liability (30% bracket) = ₹1,68,000 × 30% = ₹50,400

Net Rental Income After Tax = ₹1,92,000 − ₹50,400 = ₹1,41,600

You can use CalcPhi's Income Tax Calculator to see exactly how rental income interacts with your total taxable income and which tax bracket applies.

The Complete Net Yield Summary

| Item | Amount |

|---|---|

| Gross Annual Rent (₹24,000 × 12) | ₹2,88,000 |

| Less: Vacancy Loss (1.5 months) | −₹36,000 |

| Less: Society Maintenance | −₹18,000 |

| Less: Property Tax | −₹12,000 |

| Less: Repairs and Maintenance | −₹18,000 |

| Less: Brokerage (amortised) | −₹12,000 |

| Net Income Before Tax | ₹1,92,000 |

| Less: Income Tax (30% bracket) | −₹50,400 |

| Net Income After All Costs and Tax | ₹1,41,600 |

| True Net Rental Yield | 1.67% |

The broker's 3.39% has become 1.67% in reality — less than half the headline number. Want to run this calculation for your own property? CalcPhi's Real Estate ROI Calculator takes all these variables as inputs and gives you both gross and net yield in seconds.

Step 5 — Add Capital Appreciation to Get Total ROI

Rental yield alone is not the full picture. Real estate earns returns in two ways: current income (yield) and capital appreciation. The total return equation is:

Total ROI = Net Rental Yield + Annual Capital Appreciation Rate

Capital appreciation varies enormously by city and micro-market:

- High-growth corridors (Whitefield in Bengaluru, Gachibowli in Hyderabad, Wakad in Pune): 6 to 8% average annual appreciation

- Established central areas (South Mumbai, South Delhi, central Chennai): 3 to 6% appreciation, with significantly higher entry prices and lower yields

- Tier-2 cities (Coimbatore, Jaipur, Indore, Ahmedabad): Higher gross yields of 4 to 5%, moderate appreciation of 5 to 7%, but less liquidity

Continuing the example: if the Bengaluru flat appreciates at 6% per year, total ROI = 1.67% (net yield) + 6% (appreciation) = 7.67% total annual return.

Compare this against alternatives available to Indian investors: equity mutual funds have delivered 12 to 14% CAGR over 10-year horizons, PPF offers 7.1% fully tax-free, and NPS equity funds have averaged 13 to 17% over the long run. Use CalcPhi's SIP Calculator to model your equity returns for a direct, numbers-based comparison.

The real estate advantage comes from leverage. If you bought the property with a 20% down payment (₹17 lakh on an ₹85 lakh flat), at 6% appreciation the property gains ₹5.1 lakh in value in year one — on a ₹17 lakh investment, that is 30% return on equity before even counting net rent.

The Impact of a Home Loan on ROI

Most people buy rental property with a home loan. This changes the ROI calculation in two important ways.

First, the EMI cash outflow typically exceeds the rental income — especially in the first few years. On an ₹85 lakh property with a ₹68 lakh home loan at 8.75% for 20 years, the EMI is approximately ₹60,200 per month. Rental income of ₹24,000 covers less than 40% of the EMI. This negative cash flow must be funded from other income.

Second, the home loan interest becomes a major tax deduction. Under Section 24(b), all interest paid on a loan for a let-out property is deductible from rental income with no annual cap. In the early years of a home loan, interest forms the bulk of the EMI, so this deduction can bring taxable rental income to near zero, or even create a loss that offsets other income.

Use CalcPhi's Home Loan Tax Benefit Calculator to see exactly how much Section 24(b) can reduce your tax burden based on your specific loan amount, interest rate, and tenure.

TDS on Rental Income — When It Applies

If your tenant pays more than ₹50,000 per month in rent, they are required under Section 194-IB of the Income Tax Act to deduct TDS at 2% before paying you. This is not an additional cost to you — it is simply advance tax collected at source — but it does affect your cash flow and requires you to file an ITR to claim credit for it.

For most residential rentals under ₹50,000 per month, TDS does not apply and the landlord self-reports rental income in their annual ITR filing. CalcPhi's TDS Calculator covers both tenant and landlord scenarios clearly.

Capital Gains Tax When You Sell

The ROI calculation is incomplete without factoring in the tax you will pay when you eventually sell. As of AY 2026-27, long-term capital gains (property held for more than 24 months) from real estate are taxed at 12.5% without indexation. Short-term gains (held 24 months or less) are added to your income and taxed at your applicable slab rate.

For an ₹85 lakh property sold after 10 years at ₹1.7 crore (approximately 7.2% CAGR), the capital gain is ₹85 lakh. At 12.5%, the LTCG tax is ₹10.625 lakh. CalcPhi's Capital Gains Tax Calculator lets you model exactly this scenario with the current tax rules.

You can also avoid LTCG tax by reinvesting the gains in another residential property under Section 54, or in capital gains bonds under Section 54EC — but those options come with their own constraints and timelines.

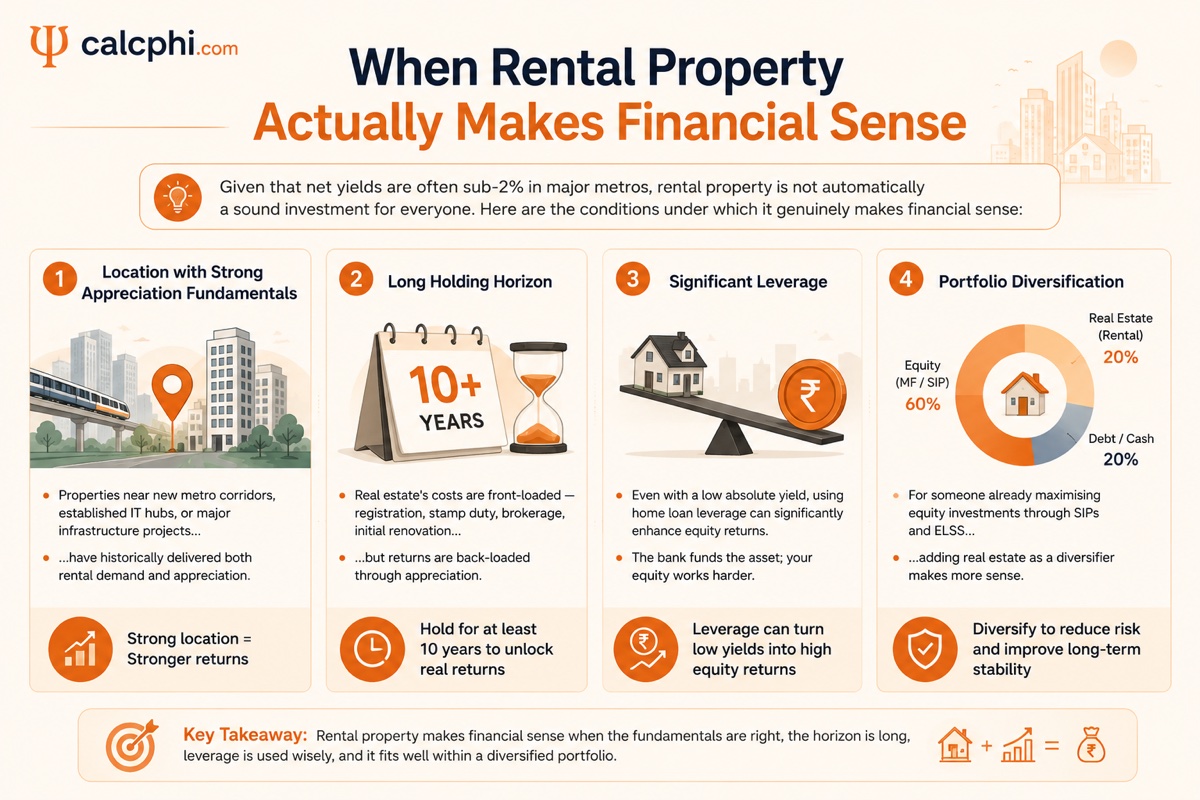

When Rental Property Actually Makes Financial Sense

Given that net yields are often sub-2% in major metros, rental property is not automatically a sound investment for everyone. Here are the conditions under which it genuinely makes financial sense:

- Location with strong appreciation fundamentals: Properties near new metro corridors, established IT hubs, or major infrastructure projects have historically delivered both rental demand and appreciation.

- Long holding horizon: Real estate's costs are front-loaded — registration, stamp duty, brokerage, initial renovation — but returns are back-loaded through appreciation. A holding period of at least 10 years is typically needed to recover entry costs.

- Significant leverage: The equity return on a leveraged purchase can be compelling even when absolute yield is low.

- Portfolio diversification: For someone already maximising equity investments through SIPs and ELSS, adding real estate as a diversifier makes more sense than for someone whose only investment is the rental flat.

Calculate your rental property returns:

Real Estate ROI Calculator → Rental Yield Calculator → Tax Benefit Calculator →

Frequently Asked Questions

What is a realistic net rental yield in India's major cities?

In metros like Mumbai, Delhi NCR, and Bengaluru, net rental yields after all costs and taxes typically fall between 1.5% and 2.5%. Tier-2 cities like Coimbatore, Jaipur, Nashik, and Ahmedabad can offer gross yields of 4 to 5%, but net yields after costs are still closer to 2.5 to 3.5%. The headline gross yield is almost always higher than what you actually receive.

Is rental income from property taxable in India?

Yes. Rental income is taxed under "Income from House Property" as per the Income Tax Act. After claiming the 30% standard deduction on Net Annual Value and deducting property tax paid, the remaining income is taxed at your applicable income tax slab rate. If you have a home loan on the property, all the interest paid is deductible under Section 24(b) for let-out property.

What expenses can I deduct against rental income in India?

You can deduct municipal/property tax actually paid, and then claim a flat 30% standard deduction on the Net Annual Value — no bills required. If the property has a home loan, the full interest is deductible under Section 24(b) for let-out property. Unlike some other countries, you cannot separately claim depreciation, maintenance bills, or brokerage costs — the 30% standard deduction is a composite allowance covering all of those.

How does a home loan affect the ROI on a rental property?

A home loan creates a negative cash flow situation in the early years — the EMI is almost always higher than the rent collected. However, the interest component of the EMI is fully deductible under Section 24(b) for let-out property, often reducing the taxable rental income to zero or even creating a loss. The leverage from the loan also amplifies your return on invested equity, since you are earning appreciation on the full property value while having put in only 20% as a down payment.

What is the LTCG tax rate on selling a residential property in India in 2026?

Under the current rules for AY 2026-27, long-term capital gains on property held for more than 24 months are taxed at a flat 12.5% without indexation. Short-term gains (under 24 months) are taxed as per your income slab. Reinvestment in another residential property under Section 54 can exempt the gains, subject to conditions and timelines.

How do I compare rental property returns with mutual funds or PPF?

The fairest comparison is total return: net rental yield plus capital appreciation for property, versus CAGR for mutual funds or the effective post-tax return for PPF. On a pure return basis, equity mutual funds with a 12 to 13% CAGR over 10+ years often outperform property. However, property's leverage effect — buying an ₹85L asset with ₹17L equity — means the return on invested capital can be much higher than the headline numbers suggest. Use CalcPhi's SIP Calculator and Real Estate ROI Calculator together to run a side-by-side comparison.

Disclaimer: The calculations and examples in this article are for educational and estimation purposes only. They do not constitute financial, tax, or investment advice. Tax rules are based on the Income Tax Act provisions applicable for AY 2026-27 and are subject to change. Please consult a SEBI-registered investment advisor or qualified Chartered Accountant for personalised guidance on property investment and tax planning.