RD vs FD: Which Is Better for Savers in 2026?

Every month, millions of Indians face the same question at their bank counter or on their banking app: should I open a Recurring Deposit or a Fixed Deposit? The two products look almost identical on paper — same bank, often the same interest rate, same government backing. But how they work underneath is quite different, and picking the wrong one can cost you thousands of rupees in interest over just a year or two. This guide breaks down how each product calculates interest, who should use which, what the tax implications are, and how to decide based on your actual financial situation.

What Is a Fixed Deposit (FD)?

A Fixed Deposit is a one-time investment product where you deposit a lump sum with a bank or post office for a fixed period at a predetermined interest rate. Once the money is in, it stays locked until maturity — and the interest clock starts ticking on the full amount from Day 1.

For example, if you place ₹1,20,000 in an FD at 7% per annum for one year, the bank calculates interest on the entire ₹1,20,000 for the full 12 months. That is the fundamental strength of an FD: your entire principal is working for you from the very first day. Banks compound FD interest quarterly in India, which gives you slightly more than the simple annual rate.

Use CalcPhi's FD Calculator to compute the exact maturity amount at any bank rate, tenure, and compounding frequency — including the impact of TDS if your interest crosses ₹40,000 in a year.

What Is a Recurring Deposit (RD)?

A Recurring Deposit is a monthly savings scheme where you commit to depositing a fixed amount — say ₹5,000 or ₹10,000 — every month for a chosen tenure. At the end of the tenure, the bank returns your total deposits plus the accumulated interest.

The key difference from an FD is in when each rupee starts earning interest. The first instalment earns interest for the full 12 months (in a one-year RD). The second instalment earns interest for only 11 months. The third for 10 months, and so on until the final instalment, which earns interest for just one month. Because of this staggered structure, the effective yield on your total investment is roughly half the stated rate — even though the advertised rate looks identical to an FD rate.

This is not a trick by banks. It is simply a reflection of the fact that your money enters the account gradually, not all at once. CalcPhi's RD Calculator shows the exact month-by-month breakdown so you can see precisely how each instalment grows.

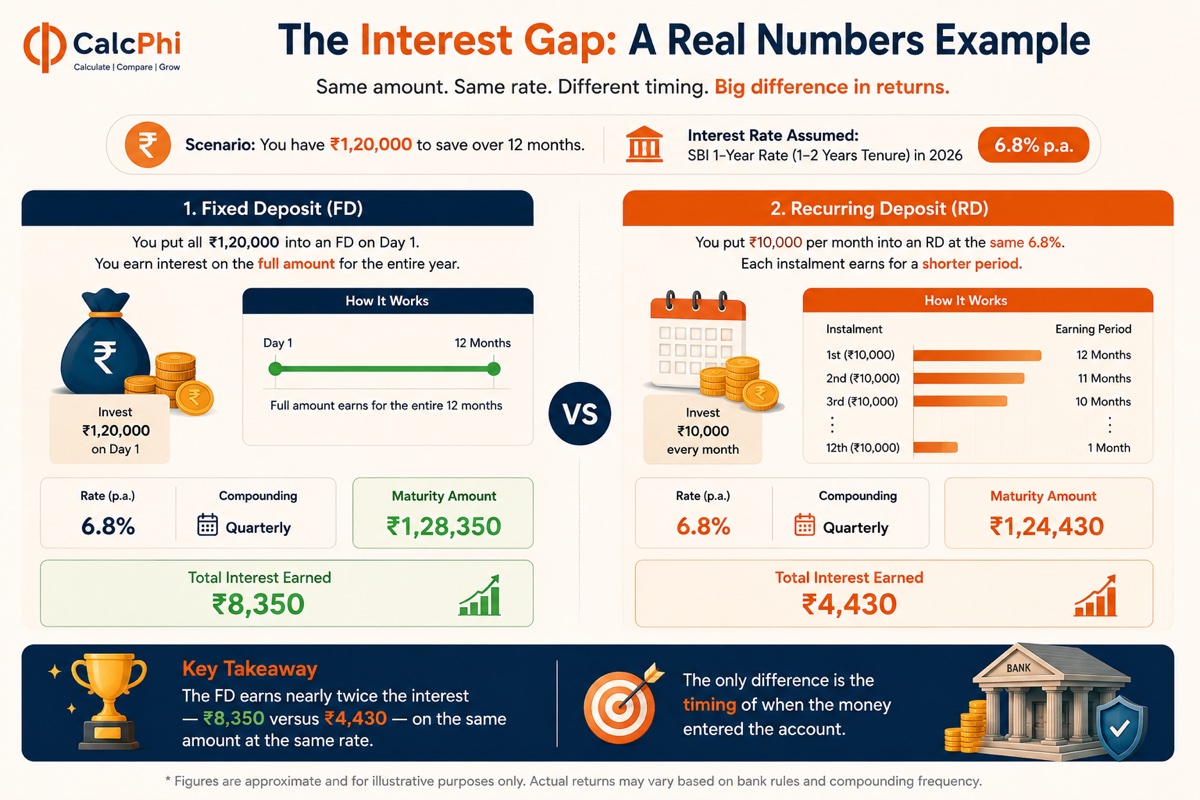

The Interest Gap: A Real Numbers Example

Let's settle the returns question with actual numbers. Assume SBI's current one-year rate of approximately 6.8% per annum (the rate applicable for tenures between 1 and 2 years in 2026).

Scenario: You have ₹1,20,000 to save over 12 months.

If you put all ₹1,20,000 into an FD on Day 1, you earn interest on the full amount for the entire year. At 6.8% compounded quarterly, your maturity amount works out to approximately ₹1,28,350 — a gain of around ₹8,350.

If you put ₹10,000 per month into an RD at the same 6.8%, only the first instalment earns for 12 months, the second for 11, and so on. Your maturity amount is approximately ₹1,24,430 — a gain of around ₹4,430.

The FD earns nearly twice the interest — ₹8,350 versus ₹4,430 — on the same amount of money at the same rate. The only difference is the timing of when the money entered the account.

| Instrument | How money enters | Maturity amount | Interest earned |

|---|---|---|---|

| FD (lump sum on Day 1) | ₹1,20,000 upfront | ₹1,28,350 | ₹8,350 |

| RD (₹10,000 / month × 12) | Monthly instalments | ₹1,24,430 | ₹4,430 |

You can run this comparison yourself using CalcPhi's FD vs RD Comparison Calculator, which lets you plug in any amount, rate, and tenure to see both outcomes side by side.

So Why Does Anyone Open an RD?

If FD always earns more at the same rate, why is RD one of the most popular savings products in India? The answer is simple: most people do not have ₹1,20,000 sitting in their savings account waiting to be invested. They are earning ₹40,000–₹60,000 a month in salary and trying to save a portion of that each month.

For that person, the real comparison is not RD versus FD. It is RD versus a savings account. And on that comparison, RD wins easily. A standard savings account pays 2.5–3.5% interest (2.7% at SBI as of 2026), while an RD at the same bank gives 6.5–7%. That is more than double the return for money you were going to park somewhere anyway.

The RD exists for exactly this type of saver — someone who earns monthly, saves monthly, and needs a product that accepts monthly contributions instead of demanding a lump sum upfront.

When FD Is Clearly the Better Choice

There are situations where FD is almost always the right answer:

You have received a bonus, a gratuity payout, proceeds from selling an asset, or an inheritance — any kind of lump sum that you do not need immediately. Putting that into an FD ensures the entire amount earns interest from Day 1 instead of sitting in a low-yield savings account while you decide what to do with it.

You are a retiree or senior citizen managing a corpus. Banks offer an additional 0.25–0.50% interest on FDs for senior citizens (60+), making the effective rate even more attractive. CalcPhi's Senior Citizen FD Calculator computes the exact maturity amount including the senior rate boost.

You want to claim the Section 80C deduction. A 5-year Tax Saver FD qualifies for deduction up to ₹1.5 lakh under Section 80C of the Income Tax Act. Recurring Deposits do not qualify for any such deduction, regardless of tenure.

Want to know your exact FD maturity amount after tax? Use CalcPhi's TDS on FD Calculator to see how much TDS the bank will deduct and what you actually take home.

When RD Is the Right Tool

RD is the right choice when you are building savings discipline from a monthly income, when you do not have a lump sum available, and when the alternative is leaving money in a low-interest savings account.

It is also useful for goal-based saving with a fixed deadline — say, you need ₹60,000 for a vacation in six months and plan to save ₹10,000 a month. An RD gives you a structured vehicle for exactly that purpose, with a better rate than a savings account and a clear maturity date matching your goal.

RD is also a good option for first-time savers who need the discipline of an automatic monthly debit. The standing instruction feature that most banks offer for RDs means the money moves out of your account before you can spend it — which is a valuable behavioural nudge for anyone building a savings habit.

Post Office RD: The Often-Overlooked Option

The Post Office Recurring Deposit scheme currently offers 6.7% per annum, compounded quarterly. It comes with sovereign guarantee (backed by the Government of India rather than just DICGC bank insurance), and premature withdrawal is allowed after 3 years without a full penalty.

For conservative savers who want a government-backed product, the Post Office RD is worth comparing alongside bank RDs. CalcPhi's Post Office RD Calculator gives you the exact maturity value under this scheme.

Tax Treatment: RD and FD Are Identical

This is a common misconception worth clearing up. Interest earned on both RDs and FDs is treated as "Income from Other Sources" under the Income Tax Act and is fully taxable at your applicable slab rate.

Banks deduct TDS (Tax Deducted at Source) at 10% on interest if the total interest from a single branch crosses ₹40,000 in a financial year (₹50,000 for senior citizens). This threshold applies to the combined interest from all deposits at that branch — so having multiple FDs or RDs at the same branch still triggers TDS once you cross ₹40,000 collectively.

If your total income is below the basic exemption limit, you can submit Form 15G (or Form 15H for seniors) to the bank to prevent TDS deduction. This does not exempt the interest from tax — it simply means the bank will not deduct TDS upfront, and you declare and pay the tax at filing time if applicable.

There is no special exemption for RDs and no additional tax benefit for any tenure of RD. If someone has told you that long-tenure RDs have a tax advantage, that information is incorrect under current law for AY 2026-27.

A Quick Decision Framework

The choice between RD and FD really comes down to one question: do you have the money now, or will you accumulate it over time?

If you have the full amount today, FD is the better financial decision — same rate, nearly double the interest earned. If you are saving from monthly income, RD is the appropriate product — not because it beats FD mathematically, but because it beats the savings account you would otherwise use, and it builds a disciplined saving habit at the same time.

If you are comfortable with digital platforms, a SIP in a liquid mutual fund is also worth considering as an alternative to RD. Liquid funds have historically delivered 6.5–7.5% returns (not guaranteed), allow same-day redemption (T+0 settlement on most platforms), and do not carry premature withdrawal penalties. For tax purposes, gains are taxed at your slab rate — the same as RD and FD interest. CalcPhi's SIP Calculator can help you model liquid fund SIP growth alongside your RD projections.

RD vs FD: A Summary Comparison

| Feature | Fixed Deposit (FD) | Recurring Deposit (RD) |

|---|---|---|

| Investment style | One-time lump sum | Monthly instalments |

| Interest on full amount from Day 1? | Yes | No — staggered |

| Effective yield vs stated rate | Equal | Lower (~half for 1 year) |

| Minimum deposit | ₹1,000 (varies by bank) | ₹100/month (varies) |

| Section 80C eligible? | Yes (5-year Tax Saver FD only) | No |

| Senior citizen rate benefit? | Yes (+0.25–0.50%) | Yes (same benefit applies) |

| Premature withdrawal penalty? | Yes (0.5–1% rate reduction) | Yes (1–2% rate reduction) |

| Post Office version available? | Yes (Post Office TD) | Yes (Post Office RD) |

| Best suited for | Lump sum savers | Monthly income savers |

Frequently Asked Questions

Does an RD give better returns than an FD if the RD rate is higher?

Not necessarily. Even if an RD offers a slightly higher interest rate, the FD at a lower rate can still produce more interest because the entire principal earns interest from Day 1. The effective yield on an RD is always lower than its stated rate due to the monthly deposit structure. Always compare actual maturity amounts using a calculator, not just headline rates.

Is RD interest taxed differently from FD interest?

No. Both RD interest and FD interest are taxed identically under "Income from Other Sources" at your applicable income tax slab rate for AY 2026-27. TDS at 10% applies when interest from a branch exceeds ₹40,000 in a year for both products. There is no preferential tax treatment for either.

Can I convert my RD into an FD midway?

Most banks do not allow a direct conversion. You would need to close the RD (with a premature withdrawal penalty of 1–2% on the rate) and then open a new FD with the proceeds. It is generally better to let an existing RD run to maturity unless there is a compelling reason to switch.

What happens if I miss an RD instalment?

Banks charge a small penalty for missed RD instalments — typically ₹1–₹2 per ₹100 of the missed amount per month of delay. If you miss too many instalments consecutively, the bank may discontinue the RD and return your deposits at a reduced interest rate. Setting up a standing instruction from your salary account to your RD avoids this entirely.

Which banks offer the best RD rates in 2026?

Small finance banks — including AU Small Finance Bank, Ujjivan Small Finance Bank, ESAF, and Jana Small Finance Bank — typically offer RD rates in the range of 7.5–9%, significantly higher than large PSBs like SBI (6.5–6.8%) or HDFC Bank (6.6–7%). Keep in mind that DICGC insurance covers deposits up to ₹5 lakh per depositor per bank — amounts above this threshold carry risk if the institution fails.

Should I close my RD early to open an FD?

Generally, no. The premature withdrawal penalty on an RD (usually 1–2% rate reduction) plus the administrative hassle rarely justifies switching unless there is a substantial rate difference between your RD rate and available FD rates. Run the actual numbers using CalcPhi's FD vs RD Calculator before making that decision.

Disclaimer: This article is for educational and informational purposes only. The interest rates mentioned reflect publicly available rates as of May 2026 and are subject to change by individual banks at any time. CalcPhi calculators are estimation tools — they do not constitute financial advice. Please consult a qualified financial advisor or SEBI-registered investment advisor before making investment decisions.