Personal Loan EMI at 11%: What It Really Costs You

Banks advertise personal loans at "interest rates starting from 10.5%." What they lead with is a number. What they don't lead with is the total interest you'll pay, the processing fee and GST layered on top, or the way amortisation front-loads interest charges in the early months. This guide runs the actual numbers on a ₹5 lakh loan at 11% — the rate most creditworthy salaried borrowers can realistically get — so you know exactly what you're signing up for.

What 11% Per Annum Actually Means in Rupees

Personal loans in India use the reducing balance method — interest is charged each month only on the outstanding principal, not the original loan amount. This is fairer than the flat rate method (still used by some small lenders) but it still adds up.

The EMI formula: EMI = P × r × (1+r)^n ÷ [(1+r)^n − 1], where P is principal, r is the monthly interest rate (annual rate ÷ 12), and n is number of monthly instalments.

For a ₹5 lakh loan at 11% for 3 years:

- Monthly rate r = 11% ÷ 12 = 0.9167%

- n = 36 months

- EMI = ₹16,370 per month

- Total repayment = ₹16,370 × 36 = ₹5,89,320

- Total interest = ₹5,89,320 − ₹5,00,000 = ₹89,320

| Item | Amount |

|---|---|

| Principal borrowed | ₹5,00,000 |

| Monthly EMI (3-year tenure) | ₹16,370 |

| Total repayment over 36 months | ₹5,89,320 |

| Total interest paid | ₹89,320 |

| Interest as % of principal | 17.9% |

How Tenure Changes Your EMI — and Your Total Cost

The single biggest lever you control when taking a personal loan is tenure. A shorter tenure means a higher monthly EMI but dramatically less total interest. A longer tenure eases monthly cash flow but costs you significantly more over time.

| Tenure | Monthly EMI | Total Interest Paid | Total Repayment |

|---|---|---|---|

| 1 year (12 months) | ₹44,216 | ₹30,592 | ₹5,30,592 |

| 2 years (24 months) | ₹23,305 | ₹59,320 | ₹5,59,320 |

| 3 years (36 months) | ₹16,370 | ₹89,320 | ₹5,89,320 |

| 5 years (60 months) | ₹10,871 | ₹1,52,260 | ₹6,52,260 |

Stretching from 3 years to 5 years cuts your monthly EMI by ₹5,499 — but costs you an additional ₹62,940 in interest. That is the price of the lower monthly payment. If you can comfortably service the 3-year EMI, do not choose 5 years.

The Amortisation Trap: Why Early EMIs Are Mostly Interest

On a reducing balance loan, early EMIs are heavily weighted toward interest. In Month 1 of your ₹5 lakh loan at 11%:

- Interest component = 11% ÷ 12 × ₹5,00,000 = ₹4,583

- Principal repaid = ₹16,370 − ₹4,583 = ₹11,787

- Outstanding balance after Month 1: ₹4,88,213

By Month 12, the principal repaid per EMI has grown to around ₹13,700 — but you have already paid ₹55,000 in interest just in the first year. This is why prepaying in the first half of the loan tenure saves far more than prepaying in the second half: when you reduce principal early, you eliminate the most interest-heavy months.

Your CIBIL Score Determines Your Rate

The 11% rate is not available to everyone — it is reserved for borrowers with strong credit profiles. Here is the typical rate range by CIBIL score bracket in 2026:

| CIBIL Score | Typical Rate Range | Interest on ₹5L (3 yr) |

|---|---|---|

| 750 and above | 10.5% – 12% | ₹84,000 – ₹97,200 |

| 700 – 749 | 13% – 16% | ₹1,06,600 – ₹1,33,200 |

| 650 – 699 | 18% – 22% | ₹1,51,200 – ₹1,88,400 |

| Below 650 | 24%+ or rejection | ₹2,00,000+ |

A 750 score versus a 720 score on the same ₹5 lakh loan can mean a ₹30,000–₹40,000 difference in total interest paid. Check your CIBIL score before applying — a free check every 12 months is available from CIBIL's website and does not affect your score.

Processing Fees, GST, and Prepayment Charges

The interest rate is only part of the cost. Every personal loan comes with additional charges that raise the true cost of borrowing:

- Processing fee: 1%–3% of loan amount, charged upfront. On a ₹5 lakh loan, that is ₹5,000–₹15,000 deducted before disbursement — you receive less but repay the full principal.

- GST on processing fee: 18% GST applies to the processing fee. A ₹10,000 fee becomes ₹11,800 effective.

- Prepayment charges: Most lenders lock in the loan for the first 6–12 months (no prepayment allowed). After that, prepayment charges of 2%–5% of the outstanding principal typically apply. Some lenders waive this after 24 months.

- Penal interest: Missing an EMI typically attracts 2%–3% penal interest per month on the overdue amount — on top of the regular interest.

Always ask for the full schedule of charges in writing before signing. The Annual Percentage Rate (APR) — which RBI now requires banks to disclose — captures all costs and is a more accurate comparison figure than the headline interest rate.

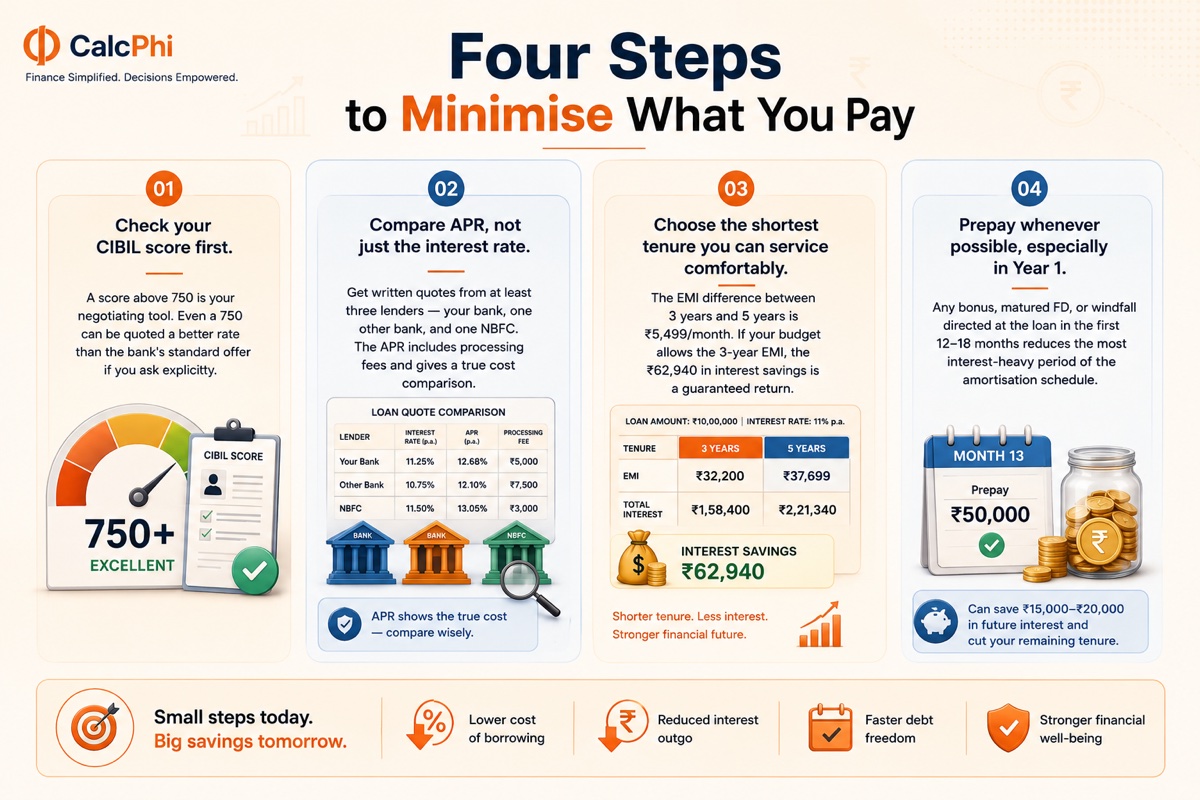

Four Steps to Minimise What You Pay

- Check your CIBIL score first. A score above 750 is your negotiating tool. Even a 750 can be quoted a better rate than the bank's standard offer if you ask explicitly.

- Compare APR, not just the interest rate. Get written quotes from at least three lenders — your bank, one other bank, and one NBFC. The APR includes processing fees and gives a true cost comparison.

- Choose the shortest tenure you can service comfortably. The EMI difference between 3 years and 5 years is ₹5,499/month. If your budget allows the 3-year EMI, the ₹62,940 in interest savings is a guaranteed return.

- Prepay whenever possible, especially in Year 1. Any bonus, matured FD, or windfall directed at the loan in the first 12–18 months reduces the most interest-heavy period of the amortisation schedule. Even ₹50,000 prepaid in Month 13 can save ₹15,000–₹20,000 in future interest and cut your remaining tenure.

Personal Loan vs Other Borrowing Options

Before committing to a personal loan, compare it against cheaper alternatives:

| Option | Typical Rate | Best For | Drawback |

|---|---|---|---|

| Personal loan | 10.5% – 24% | No collateral, quick disbursal | High rate for lower scores |

| Gold loan | 7% – 12% | Immediate cash, own gold | Gold pledged; repossession risk |

| Loan against FD | FD rate + 1–2% | Have existing FDs, low urgency | FD locked; limit = 90% of FD value |

| Loan against property (LAP) | 9% – 12% | Large amounts (₹20L+) | Property at risk; 2–3 week processing |

| Credit card EMI conversion | 13% – 18% | Already spent on card | Blocks credit limit; cancellation fees |

| Credit card revolving credit | 36% – 42% | Never use for more than 30 days | Most expensive credit available |

If you own gold or have an existing FD, exhaust those options first — you are borrowing against your own assets at near-cost rates. A personal loan makes most sense when you need funds quickly with no collateral available.

Calculate your personal loan EMI and total interest:

EMI Calculator →Frequently Asked Questions

-

What is the EMI on a ₹5 lakh personal loan at 11% for 3 years?

The EMI is ₹16,370 per month. Over 36 months you repay ₹5,89,320 in total — ₹89,320 of that is interest. In the first month alone, ₹4,583 of your EMI goes to interest and only ₹11,787 reduces the principal.

-

How is personal loan interest calculated in India?

Indian personal loans use the reducing balance method — each month's interest is calculated on the outstanding principal after deducting the previous month's principal repayment. The EMI formula is: EMI = P × r × (1+r)^n ÷ [(1+r)^n − 1], where P is the loan amount, r is the monthly interest rate (annual rate ÷ 12), and n is the number of monthly instalments.

-

Does a longer personal loan tenure save money on EMI?

A longer tenure lowers the monthly EMI but dramatically increases total interest. On a ₹5 lakh loan at 11%, a 5-year tenure reduces the EMI from ₹16,370 to ₹10,871 — but you pay ₹62,940 more in interest compared to a 3-year tenure. Unless cash flow is very tight, choose the shortest tenure you can comfortably service.

-

Can I reduce my personal loan interest after taking the loan?

Yes — through partial prepayment. Most lenders allow prepayment after 6–12 months (check your agreement for the lock-in period and prepayment charges, typically 2–5%). Prepaying a lump sum directly reduces outstanding principal, cutting all future interest calculated on that amount. Prepaying early in the loan's life saves the most because early months carry the heaviest interest burden.

-

What CIBIL score is needed to get a personal loan at 11%?

A CIBIL score of 750 or above typically qualifies you for rates in the 10.5%–12% range at major banks. Scores between 700–749 attract 13%–16%. The difference between a 720 and 780 score on a ₹5 lakh loan can mean ₹30,000–₹40,000 more in total interest. Check your score free once a year on the CIBIL website — a soft inquiry does not affect your score.

-

Is 11% a good interest rate for a personal loan in India in 2026?

Yes — 11% sits at the lower end of personal loan rates in India in 2026. Most banks advertise starting rates of 10.5%–11% but reserve them for borrowers with a CIBIL score above 750, stable salaried employment, and an existing banking relationship. Always compare the full APR (including processing fees and GST) across at least three lenders — the advertised rate and the effective rate can differ meaningfully once fees are included.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Loan rates, processing fees, and eligibility criteria change frequently. Verify current rates directly with lenders before making borrowing decisions.