NSC vs KVP vs Post Office TD: Which Government Scheme Wins in 2026?

If you want a sovereign-backed savings instrument that beats most bank FDs and fully protects your principal, three names sit at the top of the list: the National Savings Certificate (NSC), Kisan Vikas Patra (KVP), and Post Office Time Deposit (TD). All three are operated by India Post, all carry the Government of India's full backing, and all are popular with conservative investors who prize certainty over chasing returns. But they are not interchangeable — choose the wrong one and you could lose ₹15,000 to ₹40,000 on a ₹5 lakh investment over five years, purely through foregone returns and tax inefficiency.

The Quick Verdict First

For a 5-year horizon with tax saving as a goal, NSC at 7.7% is the clear winner — highest rate among the three plus 80C eligibility. For a 9–10 year horizon with no tax-saving requirement, KVP at 7.5% gives you the comfort of a guaranteed doubling in 115 months. For shorter horizons of 1, 2, or 3 years, only Post Office TD applies, since NSC and KVP both lock you in for at least five years.

Current Interest Rates: Q1 FY 2026-27

The Ministry of Finance kept all small savings rates unchanged for the April–June 2026 quarter — the eighth consecutive quarter without a change, which makes planning easier.

| Feature | NSC | KVP | PO-TD (5 yr) |

|---|---|---|---|

| Current rate | 7.7% p.a. | 7.5% p.a. | 7.5% p.a. |

| Compounding | Annual (paid at maturity) | Annual (paid at maturity) | Quarterly (interest paid annually) |

| Tenure | 5 years (fixed) | 9 years 7 months | 1, 2, 3, or 5 years |

| Section 80C | Yes (investment + accrued interest) | No | Yes (5-year only) |

| Tax on interest | Taxable on accrual; 80C offset applies | Fully taxable; no offset | Taxable annually as credited |

| Maximum investment | No limit | No limit | No limit |

| Premature withdrawal | Not allowed (except death/court) | Allowed after 2.5 years | After 6 months (with penalty) |

| Loan collateral | Yes | Yes | Yes |

You can run live numbers on each through the NSC Calculator, the KVP Calculator, and the Post Office TD Calculator for exact maturity values.

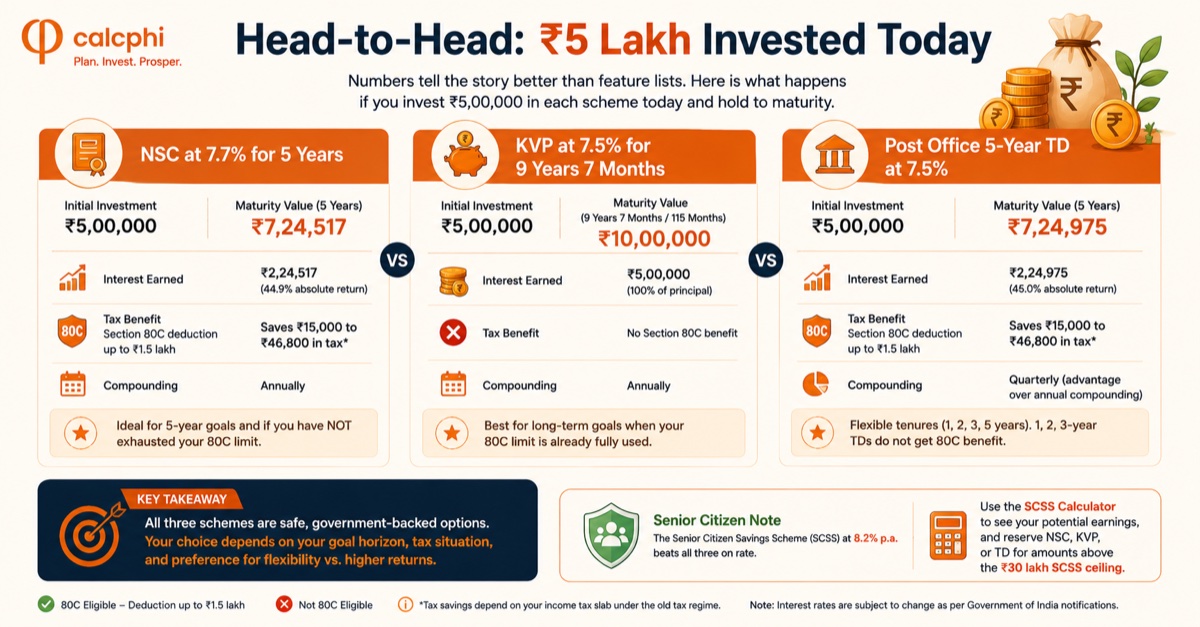

Head-to-Head: ₹5 Lakh Invested Today

Numbers tell the story better than feature lists. Here is what happens if you invest ₹5,00,000 in each scheme today and hold to maturity.

NSC at 7.7% for 5 Years

NSC compounds annually. ₹5,00,000 grows to approximately ₹7,24,517 at the end of 5 years — interest income of ₹2,24,517, or 44.9% absolute return. Crucially, the investment also fetches a Section 80C deduction of up to ₹1.5 lakh in the year of investment, which can save ₹15,000 to ₹46,800 in tax depending on your slab under the old regime.

KVP at 7.5% for 9 Years 7 Months

KVP also compounds annually but runs longer. ₹5,00,000 doubles to ₹10,00,000 at maturity, which arrives 115 months after the deposit date. There is no Section 80C benefit, but the longer compounding window means absolute interest earned equals ₹5,00,000 — exactly your principal.

Post Office 5-Year TD at 7.5%

Post Office TD compounds quarterly, giving it a slight edge over a simple annual compound at the same headline rate. ₹5,00,000 in a 5-year TD grows to approximately ₹7,24,975 at maturity — marginally above NSC in absolute terms despite the lower nominal rate, because of the quarterly compounding. The 5-year TD also qualifies for 80C deduction, putting it on equal footing with NSC for tax planning. The 1, 2, and 3-year TDs do not get any 80C benefit.

Tax Treatment: Where the Real Difference Hides

Headline rates are easy to compare. Tax treatment is where investors lose money without realising it.

NSC interest is taxable as per your income tax slab and accrues annually, even though it is paid only at maturity. The key advantage: this annually accrued interest is itself eligible for 80C deduction in the year of accrual (within the overall ₹1.5 lakh cap). For most investors, this effectively neutralises the tax on accrued interest for the first four years, with only the fifth year's interest being fully taxable.

KVP interest is fully taxable on an accrual basis with no 80C offset. The Post Office does not deduct TDS on KVP, but that does not exempt you from declaring the interest in your return. KVP suits investors who have already exhausted their 80C limit elsewhere and simply want a long-duration sovereign-backed product.

Post Office TD interest is taxable each year as it is credited. The 5-year TD is the only TD tenure that qualifies for 80C, and only under the old tax regime. If you have moved to the new regime — which is now the default — the 80C benefit on 5-year TD becomes irrelevant, and you should compare returns purely on a post-tax interest basis. Run your numbers through the TDS on FD Calculator to see what you actually take home.

Liquidity and Premature Withdrawal

All three schemes have lock-ins, but the rules around early exit vary significantly.

NSC has a hard 5-year lock-in. Premature withdrawal is allowed only on death of the holder, court-ordered forfeiture, or court-directed refund. There is no liquidity for personal emergencies. If you might need this money in less than five years, NSC is not the right scheme.

KVP allows premature withdrawal after 2 years and 6 months from the deposit date, with interest paid at the rate applicable at the time of withdrawal — typically lower than the contracted rate. So while KVP is technically more liquid than NSC in years 3 to 9, you sacrifice yield to access it.

Post Office TD is the most flexible of the three. No withdrawal is permitted in the first 6 months. Between 6 months and 1 year, only the savings account rate of 4% applies. After 1 year, premature closure of the 2/3/5-year TD attracts an interest rate 2 percentage points below the contracted rate — so closing a 5-year TD at 7.5% after 18 months earns roughly 5.5% on the holding period.

Want to see the exact maturity value for your investment amount? Use CalcPhi's free NSC Calculator, KVP Calculator, or Post Office TD Calculator. Each runs in your browser, no sign-up needed.

Eligibility, Limits, and Account Rules

NSC is open to any resident Indian individual, including minors above 10 in their own name. Joint accounts are allowed (up to three holders), and there is no maximum investment cap. The minimum is ₹1,000 with subsequent investments in multiples of ₹100. NRIs cannot invest.

KVP follows similar rules — open to all resident individuals with no upper limit, ₹1,000 minimum, and minors above 10 can hold in their own name. KVPs are also transferable from one person to another, which neither NSC nor TD allows in the same straightforward way.

Post Office TD is open to resident individuals with the same ₹1,000 minimum and no maximum. You can hold multiple TD accounts across tenures simultaneously — useful if you want to ladder deposits maturing at different times.

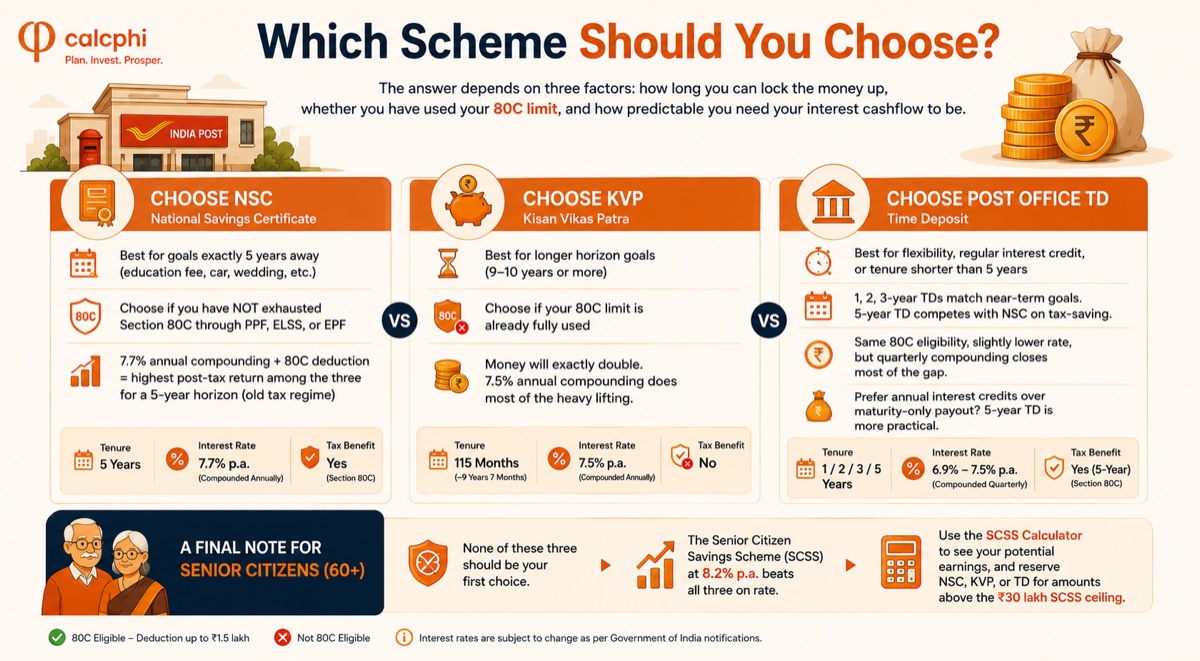

Which Scheme Should You Choose?

The answer depends on three factors: how long you can lock the money up, whether you have used your 80C limit, and how predictable you need your interest cashflow to be.

Choose NSC if you are saving for a goal exactly five years away — a child's higher-education fee, a planned car upgrade, a wedding fund — and you have not exhausted Section 80C through PPF, ELSS, or EPF contributions. The 7.7% annual compounding combined with the 80C deduction makes it the highest post-tax return among the three for a 5-year horizon under the old tax regime.

Choose KVP if you have a longer horizon — saving for a child's college education that begins in 9 to 10 years, or simply setting aside a corpus and forgetting about it — and your 80C is already filled. The mental simplicity of "your money will exactly double" is genuinely useful, and the 7.5% annual compounding does most of the heavy lifting.

Choose Post Office TD if you want flexibility, regular interest credit, or a tenure shorter than 5 years. The 1, 2, and 3-year TDs let you match a deposit to a near-term goal. The 5-year TD competes directly with NSC on tax-saving — same 80C eligibility, slightly lower headline rate, but quarterly compounding closes most of the gap. If you prefer annual interest credits over a maturity-only payout, the 5-year TD is more practical.

A final note: if you are a senior citizen above 60, none of these three should be your first choice. The Senior Citizen Savings Scheme at 8.2% beats all three on rate. Use the SCSS Calculator to see your potential earnings, and reserve NSC, KVP, or TD for amounts above the ₹30 lakh SCSS ceiling.

Common Mistakes to Avoid

Three mistakes show up repeatedly. The first is choosing KVP for a 5-year goal because "it sounds safe" — KVP cannot be cleanly redeemed at 5 years without losing yield, so you either commit for 9.5 years or accept reduced returns. The second is buying NSC under the new tax regime expecting 80C benefits — those deductions don't apply, which strips away its main advantage over Post Office TD. The third is treating Post Office TD interest as tax-free because no TDS is deducted — it is fully taxable, and underdeclaring it is a notice waiting to happen.

Frequently Asked Questions

Which is better in 2026: NSC or 5-year Post Office TD?

NSC is marginally better for tax-saving investors under the old regime — 7.7% annual compounding plus 80C benefit on accrued interest gives a slightly higher post-tax return than the 7.5% TD. For investors on the new tax regime, the 5-year Post Office TD is more practical: near-identical returns, annual interest credit, and slightly easier premature withdrawal terms.

Does KVP qualify for Section 80C deduction?

No. KVP does not qualify for any Section 80C tax deduction, and the interest earned is fully taxable as per your income tax slab. KVP is purely a wealth-doubling instrument with sovereign safety, not a tax-saving product. If you need 80C benefits, choose NSC or 5-year Post Office TD instead.

Is TDS deducted on NSC, KVP, or Post Office TD interest?

The Post Office does not deduct TDS on any of these three schemes — but the interest is still fully taxable and you are required to declare it in your income tax return. This is the opposite of bank FDs, where TDS is deducted at source once interest crosses ₹40,000 (₹50,000 for seniors) in a year. Self-declaration discipline is essential here.

Can I prematurely close my NSC, KVP, or Post Office TD?

NSC cannot be closed prematurely except on the holder's death or court order. KVP can be closed after 2 years and 6 months at the prevailing rate, which is lower than the contracted rate. Post Office TD allows premature closure after 6 months, with reduced interest applied based on the holding period — roughly 2 percentage points below the contracted rate after the first year.

What is the minimum and maximum investment in each scheme?

The minimum for NSC, KVP, and Post Office TD is ₹1,000 each, with additional deposits in multiples of ₹100. There is no maximum investment cap on any of the three — you can deposit ₹50 lakh or more — though large amounts should be split across multiple certificates or accounts for easier administration and partial liquidity later.

Are NSC, KVP, and Post Office TD safe investments in 2026?

Yes. All three are backed by the full faith and credit of the Government of India, making them effectively zero-credit-risk investments. Bank FDs, by comparison, are insured only up to ₹5 lakh per depositor per bank under DICGC. For amounts above ₹5 lakh, post office schemes carry a higher safety profile than any non-PSU bank FD.

The Bottom Line

NSC remains the highest-yielding 5-year sovereign-backed instrument in 2026, with the added bonus of 80C deduction for those still on the old tax regime. KVP is the right pick for a longer 9–10 year horizon when you simply want to double your money safely with no tax-saving requirement. Post Office TD is the most flexible across tenures, and the 5-year TD is a practical alternative to NSC for new-regime taxpayers.

There is no single "best" — the right answer depends on your time horizon, your tax regime, and how much liquidity you might need before maturity.

Calculate your returns on government schemes:

NSC Calculator → KVP Calculator → Post Office TD Calculator → SCSS Calculator →Disclaimer: This article is for educational and estimation purposes only. CalcPhi calculators help you understand financial concepts and project outcomes — they do not constitute financial advice. Small savings interest rates are revised quarterly by the Ministry of Finance and may change. Tax treatment depends on your individual circumstances and the prevailing tax regime. For personalised guidance, please consult a SEBI-registered investment advisor or a qualified Chartered Accountant.