HRA Exemption in 2026: How to Claim It, Even If You Pay Rent to Your Parents

If you live in your parents' home and pay them rent every month, you can legally claim HRA exemption on that rent — and potentially save tens of thousands of rupees in income tax each year. Most salaried employees either don't know this is allowed, or assume it sounds too good to be true and never try it. It is perfectly legal, explicitly permitted under the Income Tax Act, and used by millions of taxpayers across India.

This guide walks you through exactly how to do it: the legal basis, the calculation formula, a complete worked example, what documents you need, how to declare it, and the one scenario where the Income Tax Department will reject it outright.

What Is HRA and Why Does It Matter for Your Tax?

HRA stands for House Rent Allowance. It is a component of your salary that your employer pays to help cover your rental expenses. Under Section 10(13A) of the Income Tax Act, the HRA you receive is not fully taxable — a portion of it is exempt from tax, based on a formula we'll cover shortly.

For many salaried employees, HRA is one of the largest components in their pay structure. If your basic salary is ₹50,000 per month, your employer might be paying you ₹20,000 to ₹25,000 as HRA. Claiming the full exemption on that amount could reduce your taxable income by ₹2.4 to ₹3 lakhs per year — which translates directly into tax savings of ₹36,000 to ₹93,000 depending on your income bracket.

To claim HRA exemption, you must actually be paying rent for a place you live in. This is where paying rent to your parents becomes a powerful and often underused strategy.

Is Paying Rent to Your Parents Legal Under the Income Tax Act?

Yes — unconditionally. The Income Tax Act does not bar you from entering into a valid tenancy arrangement with your parents. The Supreme Court and various Income Tax Appellate Tribunals have consistently upheld this, provided the arrangement is genuine — meaning you are actually paying rent, there is documentation to support it, and your parent is declaring the income in their own ITR.

The key phrase there is "genuine arrangement." You cannot simply write on paper that you paid rent without any money actually moving. A formal rent agreement, monthly rent receipts, and ideally a bank transfer trail are the three things that keep this arrangement watertight in case of any scrutiny.

The one relationship the Income Tax Department explicitly disallows is rent paid to a spouse. The department treats spousal rent payments as a sham transaction with no arm's-length basis, and it has been rejected repeatedly in case law. Parents, however, are treated as independent parties.

The HRA Exemption Formula: Three Rules, Take the Minimum

Whether you are paying rent to your parents, a landlord, or a housing society, the formula to calculate your HRA exemption is the same. Your exemption is the lowest of these three amounts:

Rule 1: The actual HRA you receive from your employer in a year.

Rule 2: 50% of your basic salary if you live in a metro city, or 40% of your basic salary if you live in a non-metro city. Metro cities for HRA purposes are strictly Mumbai, Delhi, Kolkata, and Chennai. Every other city — including Bengaluru, Hyderabad, Pune, Ahmedabad, and Jaipur — is classified as non-metro regardless of its size or economic significance.

Rule 3: Actual rent paid in a year, minus 10% of your basic salary.

The exemption is whichever of these three figures is the smallest. The remaining HRA (after deducting the exemption) is added back to your taxable income.

Worked Example: Paying Rent to Parents in Delhi

Let us walk through a complete example. Priya is a marketing manager in Delhi. She lives with her parents in their own flat and has set up a rent arrangement.

| Detail | Monthly | Annual |

|---|---|---|

| Basic salary | ₹70,000 | ₹8,40,000 |

| HRA received from employer | ₹28,000 | ₹3,36,000 |

| Monthly rent paid to parents | ₹22,000 | ₹2,64,000 |

Rule 1 — Actual HRA received: ₹3,36,000

Rule 2 — 50% of basic (metro): 50% × ₹8,40,000 = ₹4,20,000

Rule 3 — Rent paid minus 10% of basic: ₹2,64,000 − (10% × ₹8,40,000) = ₹2,64,000 − ₹84,000 = ₹1,80,000

HRA exemption = minimum of ₹3,36,000, ₹4,20,000, and ₹1,80,000 = ₹1,80,000

Taxable HRA = ₹3,36,000 − ₹1,80,000 = ₹1,56,000

Now, if Priya increased her rent to ₹30,000 per month (₹3,60,000 per year), Rule 3 becomes ₹3,60,000 − ₹84,000 = ₹2,76,000 — which is still below Rules 1 and 2. Her exemption rises to ₹2,76,000, saving her roughly ₹28,000 more in tax if she is in the 30% bracket.

The takeaway: to maximise your exemption, you want Rule 3 to be as large as possible. That means paying a realistic market-rate rent to your parents — not a token amount. Want to run your own numbers instantly? Use CalcPhi's free HRA Calculator — enter your basic salary, HRA received, rent paid, and city type, and it gives you your exact exemption amount in seconds.

How to Set the Right Rent Amount

The rent you pay your parents should reflect a fair market rate for the property. This does not mean you need to pay the highest rent on the street, but it should be in a ballpark that a real tenant would pay for a similar space in the same locality.

If you pay ₹2,000 a month for a 3BHK in South Delhi, a tax officer reviewing your file will flag it immediately. A reasonable rent — even ₹15,000 to ₹25,000 for a room in a well-located home — is far more defensible and will clear any scrutiny without question.

From a family tax-planning perspective, the optimal rent amount is one where your HRA exemption is maximised and your parent's additional tax liability (from declaring this rent as income) is minimised. If your parents are retired and have no other income, or if they are senior citizens with a basic exemption limit of ₹3 lakh (₹5 lakh if they are super senior citizens above 80), the rent income may attract very little or no tax on their end. The family unit as a whole could come out significantly ahead.

Your Parents' Tax Obligation: What They Must Do

When your parents receive rent from you, that rental income is taxable in their hands. They must declare it under the head "Income from House Property" in their ITR. Here is the good news: the Income Tax Act allows a standard deduction of 30% on rental income, which automatically reduces their taxable rent income by nearly a third.

For example, if your parents receive ₹3 lakh per year in rent from you, they get a standard deduction of ₹90,000, making their taxable rental income ₹2,10,000. For a senior citizen parent with no other income, this falls well within the ₹3 lakh basic exemption limit — meaning they may owe zero tax on it.

This family-level tax arbitrage is completely legal and is precisely why this strategy works so well for joint families. You reduce your taxable income; your parent, who is in a lower bracket, picks up that income with minimal or no tax impact.

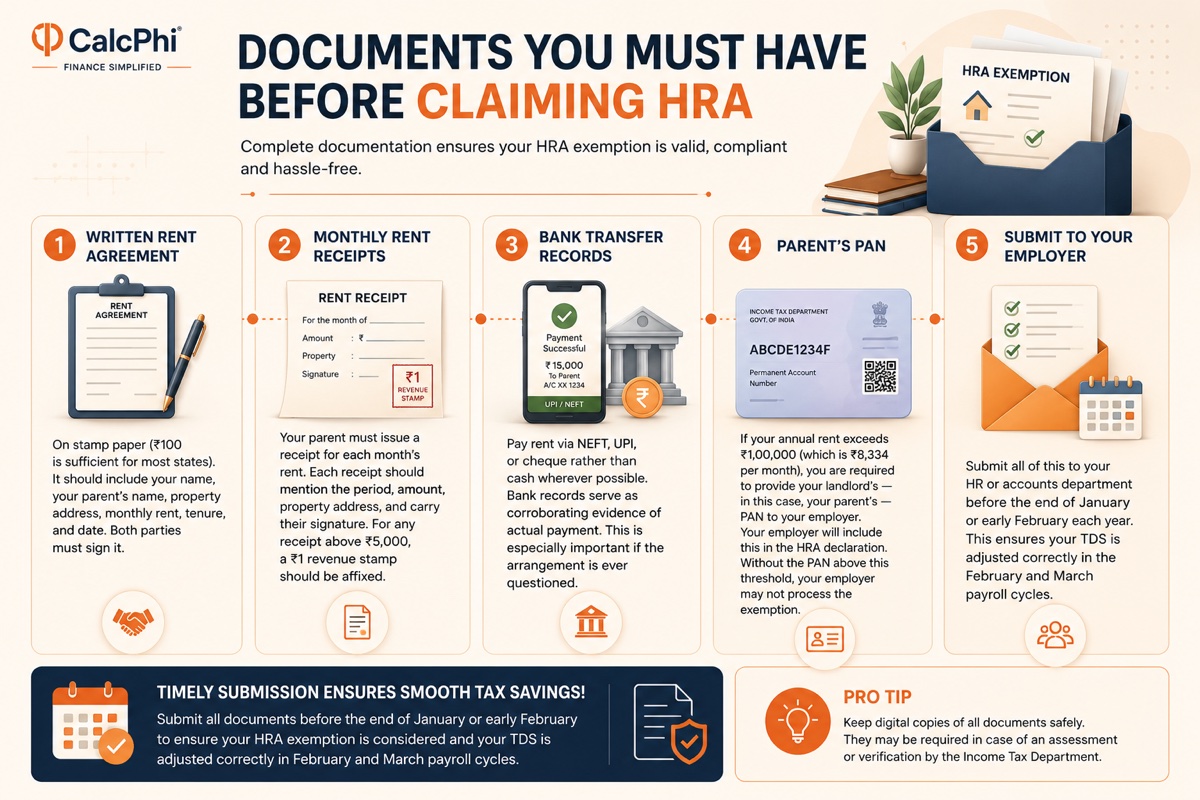

Documents You Must Have Before Claiming HRA

Claiming HRA exemption for rent paid to parents requires the same documentation as any other rental arrangement. Do not skip any of these.

A written rent agreement: This should be on a stamp paper (₹100 is sufficient for most states). It should clearly state your name, your parent's name, the address of the property, the monthly rent, the tenure, and the date. Both parties must sign it.

Monthly rent receipts: Your parent must issue a receipt for each month's rent. Each receipt should mention the period, the amount, the property address, and carry their signature. For any receipt above ₹5,000, a ₹1 revenue stamp should be affixed.

Bank transfer records: Pay rent via NEFT, UPI, or cheque rather than cash wherever possible. Bank records serve as corroborating evidence of actual payment. This is especially important if the arrangement is ever questioned.

Parent's PAN: If your annual rent exceeds ₹1,00,000 (which is ₹8,334 per month), you are required to provide your landlord's — in this case, your parent's — PAN to your employer. Your employer will include this in the HRA declaration. Without the PAN above this threshold, your employer may not process the exemption.

Submit all of this to your HR or accounts department before the end of January or early February each year. This ensures your TDS is adjusted correctly in the February and March payroll cycles.

HRA and the New Tax Regime: A Critical Decision Point

This is the most important caveat about HRA in 2026. HRA exemption under Section 10(13A) is not available if you opt for the new tax regime. The new regime, which became the default in FY 2023-24, offers lower tax slab rates but strips away most deductions and exemptions — including HRA, Section 80C, and Section 80D.

If your HRA exemption is significant — say, ₹2 to ₹3 lakhs per year — it may well make the old regime more beneficial for you, even though its slab rates are higher. The decision depends on the total value of all exemptions you can claim.

Use CalcPhi's New vs Old Tax Regime Calculator to compare both regimes with your actual numbers. Many salaried employees in the ₹8 lakh to ₹15 lakh income range find that claiming HRA and 80C deductions under the old regime saves them more than the rate benefit of the new regime.

What If You Own a Property Somewhere Else?

A common situation: you own a flat in your hometown but work in a different city and live in your parents' home there. Can you claim HRA exemption even though you own property?

Yes, you can — with one condition. The property you own must be in a different city from where you are actually living and working. If you own a flat in Jaipur but work and live in Pune (even in your parents' home), you can claim HRA exemption on the rent you pay in Pune.

However, if your own flat is in the same city where you work, the Income Tax Department takes the position that you should be living in your own property, and HRA exemption may be disallowed. This is an area where the facts of your specific situation matter, so consult a CA if you are in this scenario.

You can also claim HRA exemption and home loan interest deduction (under Section 24b) simultaneously if your owned property is in a different city. The combination of these two deductions can be very powerful for tax saving.

What If Your Employer Does Not Offer HRA? (Section 80GG)

Some employers — particularly startups, small businesses, or companies offering entirely flexible CTC structures — do not include HRA as a separate component. If you do not receive HRA from your employer but pay rent, you are not left without recourse. Section 80GG of the Income Tax Act provides a deduction for rent paid by individuals who do not receive HRA.

Under 80GG, your deduction is the minimum of: ₹5,000 per month (₹60,000 per year), 25% of your total income, or actual rent paid minus 10% of your income. This deduction is smaller than what most people claim under HRA exemption, but it is better than nothing. To claim 80GG, you must file Form 10BA declaring that you pay rent and do not own a property in your name, your spouse's name, or your minor child's name, in the city where you work.

Step-by-Step: How to Claim HRA When Filing Your ITR

If you have already submitted your documents to your employer and they have adjusted your TDS, you just need to verify the details in your Form 16 and carry them over to your ITR filing. Your Form 16 will show the HRA exemption amount separately under Part B.

If you are claiming HRA at the ITR stage, follow these steps. First, calculate your HRA exemption using the three-rule formula. Second, enter the exempt amount in Schedule S (Salary) of your ITR under "Allowances to the extent exempt under Section 10." Third, keep all supporting documents — rent agreement, receipts, PAN, bank records — on hand for at least six years in case the ITR is selected for scrutiny.

Also cross-check your TDS figure in Form 26AS and AIS (Annual Information Statement) before filing. If your employer deducted excess TDS (because the HRA exemption was not considered), the difference will be reflected as a refund after you file. Use CalcPhi's Income Tax Calculator to estimate your total tax liability for AY 2026-27 and check how much refund, if any, you are entitled to.

Common Mistakes That Get HRA Claims Rejected

Paying cash rent with no receipts and no bank trail is the most common reason HRA claims are questioned. Even if the arrangement is genuine, lack of documentary evidence makes it difficult to defend.

Setting an unrealistically low rent — ₹1,000 or ₹2,000 per month in a metro city — is a red flag. Officers comparing this against your income level and the property's market value will not accept it.

Forgetting that your parents need to declare the rent in their ITR is another major error. If you claim HRA on rental income but your parents show no corresponding rental income in their filing, and both filings are processed under linked PANs (which is increasingly common with AIS matching), it can trigger a mismatch notice for both of you.

Finally, continuing to claim HRA after shifting to the new tax regime is a mistake that leads to tax demands with interest. Always verify your regime election before filing.

Frequently Asked Questions

Can I pay rent to my parents and claim HRA exemption at the same time as claiming 80C deductions?

Yes. HRA exemption and Section 80C deductions are entirely separate provisions. You can claim both simultaneously under the old tax regime. However, neither HRA exemption nor 80C deductions are available under the new tax regime, so you must choose the old regime to benefit from both. Use CalcPhi's Section 80C Calculator to see how much you can deduct through EPF, PPF, ELSS, and life insurance combined.

What if my parents don't file an ITR — can I still claim HRA?

You can still claim the HRA exemption from your employer's perspective, but your parents are legally required to file an ITR and declare the rental income if it exceeds the basic exemption limit (₹2.5 lakh for those under 60). If they don't file, there's a mismatch risk under the AIS system. It is strongly advisable to ensure your parents file their ITR if they are receiving rent from you.

Does the amount of rent matter, or can I set any amount?

The rent must reflect a fair market rate for the property. There is no fixed rule, but a very low amount relative to property size and location will attract scrutiny. The goal is to set a rent that is both genuinely supportable and large enough to maximise your HRA exemption under Rule 3 of the formula.

My parents jointly own the house. Do both of them need to sign the rent agreement?

Ideally, yes — both owners should be parties to the rent agreement since the property is jointly owned. The rental income will then be split between them in proportion to their ownership share, and each will declare their share in their respective ITR. This can actually be more tax-efficient if both parents are in a low or nil tax bracket.

Can I claim HRA for a part of the year if I moved into my parents' home mid-year?

Yes. HRA exemption is calculated on a month-by-month basis. You claim the exemption only for the months during which you were actually paying rent and living in the rented accommodation. Months where you were in your own property or not paying rent do not qualify.

What is the difference between HRA exemption and Section 80GG? Which is better?

HRA exemption under Section 10(13A) applies only if your employer pays you HRA as part of your salary. It is typically larger because there is no upper cap — it is determined by your actual HRA received and rent paid. Section 80GG applies when you don't receive HRA, and is capped at ₹5,000 per month. If your employer offers HRA, that route is almost always more beneficial. If not, 80GG is the fallback.

Disclaimer: The information in this article is for educational and informational purposes only. HRA exemption calculations depend on individual salary structures, city classifications, and income tax regime choices. Nothing in this article constitutes personalised financial or tax advice. Tax laws are subject to changes in the Union Budget and CBDT circulars. Please consult a qualified Chartered Accountant or tax advisor for advice tailored to your specific situation.