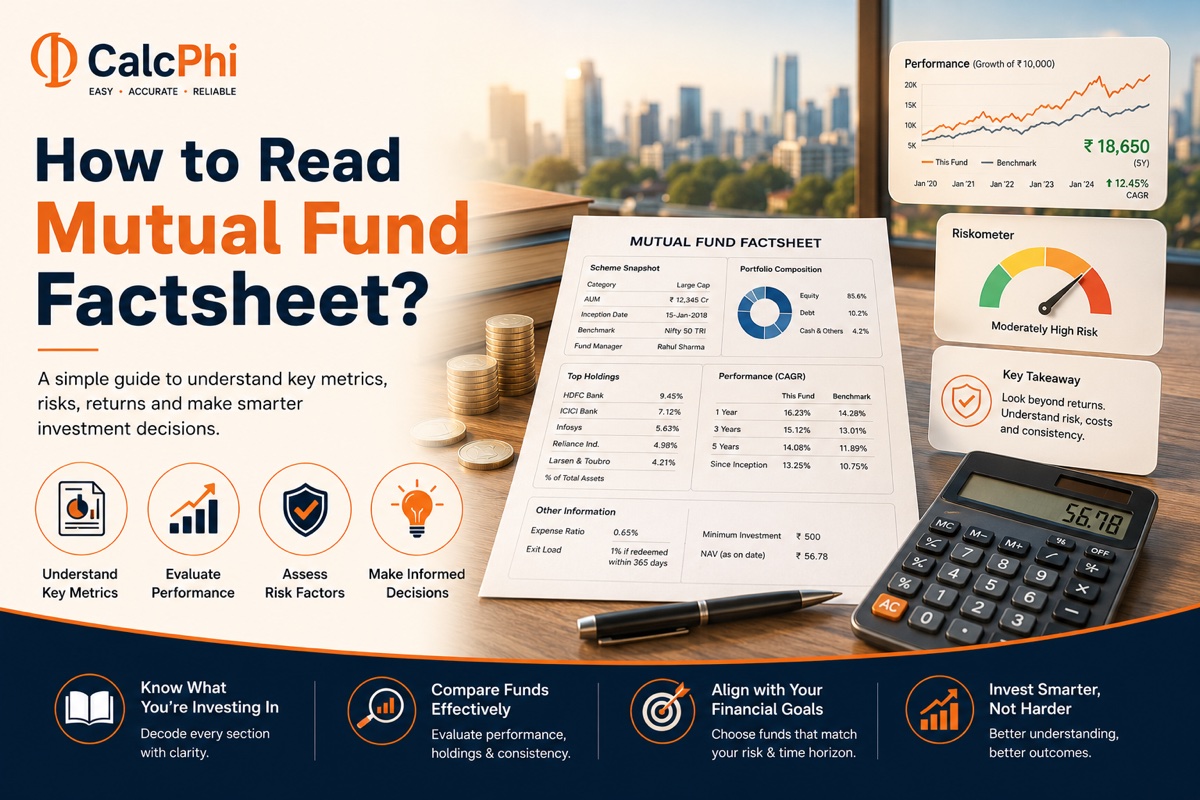

How to Read a Mutual Fund Factsheet: Every Number Decoded

You have shortlisted a mutual fund, and someone tells you to "check the factsheet before investing." You open it and see a wall of numbers — NAV, AUM, Sharpe Ratio, Standard Deviation, Portfolio Turnover Ratio. It looks like a research report written for finance professors, not regular investors. The truth is that a mutual fund factsheet is one of the most powerful tools available to an Indian investor — but only if you know how to read it. Once you understand what each number means, the factsheet stops being intimidating and starts being genuinely useful.

What Is a Mutual Fund Factsheet?

A mutual fund factsheet is a standardised document that every Asset Management Company (AMC) in India must publish each month. SEBI (Securities and Exchange Board of India) mandates its disclosure so investors can make informed decisions. Think of it as the report card of a mutual fund — it tells you what the fund owns, how it has performed, how risky it is, and how much it costs to stay invested.

Factsheets are typically published on the 10th of every month and are available on the AMC's website, the AMFI (Association of Mutual Funds in India) website, and most investment platforms.

Section 1: Fund Basics — The Identity Card

Before diving into numbers, the top section of every factsheet carries basic information that tells you what kind of fund this is.

Fund Category and Type — SEBI has defined categories like Large Cap, Mid Cap, Flexi Cap, ELSS, Hybrid, and Debt. This tells you where the fund invests and who it is meant for. A large-cap fund invests in the top 100 companies by market capitalisation; a mid-cap fund invests in companies ranked 101 to 250. Knowing the category helps you compare the fund with others in the same peer group — never compare a mid-cap fund's returns with a large-cap fund's returns.

Benchmark Index — This is the index the fund measures itself against. If a large-cap fund's benchmark is the Nifty 50, you need to ask: is the fund doing better than the Nifty 50? If not, you might as well invest in an index fund at a much lower cost.

Fund Manager — This is the person making investment decisions on your behalf. Check how long they have managed this particular fund. A fund with an excellent 10-year track record but a new fund manager hired six months ago requires a closer look.

Date of Inception — Funds with at least five years of history give you more meaningful data to evaluate. A fund launched in 2021 has only seen one phase of the market; a fund from 2010 has seen multiple market cycles.

Section 2: NAV and AUM — The Two Numbers Everyone Knows (But Often Misreads)

NAV (Net Asset Value) is the price of one unit of the fund on a given day. It is calculated by dividing the total value of all the fund's assets by the number of units outstanding. A fund with NAV of ₹250 is not "expensive" compared to a fund at ₹15. A higher NAV simply means the fund has been running longer or has grown more — it says nothing about future returns. Avoid the common mistake of preferring funds with low NAVs thinking they are "cheaper to buy."

AUM (Assets Under Management) is the total amount of money all investors have put into the fund. It is expressed in crores of rupees. A large AUM (say, ₹50,000 crore for an equity fund) can be a double-edged sword. On the positive side, it signals investor trust and keeps the fund's expense ratio lower. On the negative side, very large equity funds can struggle to take meaningful positions in smaller companies without moving the market. For mid-cap and small-cap funds specifically, look for AUM that is large enough to be stable but not so large that it becomes difficult to manage.

Section 3: Expense Ratio — The Silent Return Killer

The expense ratio is the annual fee the AMC charges to manage the fund, expressed as a percentage of your invested amount. If a fund has an expense ratio of 1.5%, that 1.5% is deducted from your returns every year automatically — you never see a separate bill.

Over long periods, this seemingly small number can cost you significantly. A fund returning 12% per year with an expense ratio of 1.5% nets you only 10.5%. On a ₹10 lakh investment over 20 years, that 1.5% difference in annual return translates to roughly ₹20–25 lakh less in final corpus.

SEBI caps expense ratios — for equity funds, the maximum is around 2.25% for direct plans. Direct plans always have lower expense ratios than regular plans because there is no distributor commission involved. Curious how much your expense ratio is actually costing you over time? Use CalcPhi's Direct vs Regular Mutual Fund Calculator to see the real rupee cost of your fund's fees across any investment horizon.

Section 4: Returns — Reading Past Performance the Right Way

The returns section is usually what investors look at first. Factsheets show returns across multiple periods: 1 month, 3 months, 6 months, 1 year, 3 years, 5 years, and since inception. They are usually shown as both absolute returns and CAGR (Compounded Annual Growth Rate).

CAGR is the single most useful return figure in the factsheet. It tells you the average annual rate at which your investment would have grown if returns were compounded smoothly. A CAGR of 15% over 5 years means ₹1 lakh became ₹2.01 lakh. You can verify any such calculation using CalcPhi's CAGR Calculator.

Always compare the fund's returns against its benchmark and against the category average — both are shown in the factsheet. A fund that returned 14% looks impressive until you see its benchmark returned 16%. At that point, the fund has underperformed, and you would have been better off in a passive index fund.

Do not rely on 1-year returns to judge a fund. Short-term returns are heavily influenced by market timing. Use 5-year and 10-year CAGR to assess how the fund has navigated different market cycles.

Section 5: Risk Metrics — The Numbers Most Investors Skip

This is the section that separates informed investors from those who just chase returns. Risk metrics tell you how much volatility you are accepting to earn those returns.

Standard Deviation measures how much the fund's monthly or annual returns have fluctuated around their average. A fund with a standard deviation of 18% is more volatile than one with 12%. Higher standard deviation is not automatically bad — it depends on whether you are being rewarded for that extra risk with better returns.

Sharpe Ratio answers the question: "Am I being compensated for the risk I am taking?" It divides the fund's excess return (above the risk-free rate, typically the 91-day T-bill rate) by its standard deviation. A Sharpe Ratio above 1.0 is generally considered good. A fund with a higher Sharpe Ratio delivers more return per unit of risk — which is exactly what you want.

Beta measures how much the fund moves relative to the market. A beta of 1.0 means the fund moves exactly with the index. A beta of 1.2 means if the market falls 10%, the fund is likely to fall 12%. Aggressive equity funds tend to have higher betas. Conservative investors should look for funds with beta closer to or below 1.

Alpha is the fund's return above and beyond what its beta-adjusted benchmark return predicted. A positive alpha means the fund manager has genuinely added value through stock selection. Alpha is rare and hard to sustain — so treat consistent positive alpha as a strong green flag.

Sortino Ratio is a more refined version of the Sharpe Ratio. Instead of penalising all volatility, it only penalises downside volatility — the kind that actually hurts investors. A higher Sortino Ratio means the fund has done a better job of protecting you in falling markets while still participating in the upswings.

| Sharpe Ratio | Interpretation |

|---|---|

| Below 0.5 | Poor — returns do not justify the volatility |

| 0.5–1.0 | Acceptable — moderate risk-adjusted performance |

| 1.0–2.0 | Good — solid risk-adjusted returns |

| Above 2.0 | Excellent — high return for risk taken |

Section 6: Portfolio Composition — What the Fund Actually Owns

Top 10 Holdings — Every factsheet shows the fund's largest positions with their percentage allocation. If the top 10 holdings account for 70–80% of the portfolio, the fund is highly concentrated. This can be a strength if those bets pay off, or a significant risk if they do not. Compare these holdings across quarters to understand the manager's conviction and trading style.

Sector Allocation — This shows which industries the fund is heavily invested in — financials, technology, healthcare, consumer goods, and so on. If you already hold a fund heavily weighted in banking and are considering a second fund that is also 35% banking, your portfolio is not as diversified as you think.

Market Capitalisation Split — For equity funds, the factsheet shows what percentage is in large-cap, mid-cap, and small-cap stocks. This is particularly useful for flexi-cap and multi-cap funds where the manager has discretion to shift the allocation.

Portfolio Turnover Ratio — This number tells you how frequently the fund manager buys and sells stocks. A ratio of 100% means the entire portfolio was replaced once during the year. High turnover leads to higher transaction costs, which eat into returns. A low-turnover fund (below 50%) typically has a more disciplined, long-term investment style.

Section 7: SIP Performance Data

Many factsheets now include an SIP return table showing what a monthly SIP of ₹10,000 invested over 1, 3, 5, and 10 years would have grown to, along with the XIRR (Extended Internal Rate of Return). XIRR is the correct way to measure SIP returns because it accounts for the timing of each cash flow.

Want to model your own SIP projections before you invest? CalcPhi's SIP Calculator lets you enter your monthly amount, expected return rate, and tenure to see your potential corpus — no sign-up needed, and results are instant. If you plan to increase your SIP amount each year as your income grows, use the Step-Up SIP Calculator to see how even a 10% annual increase can significantly boost your final wealth.

Section 8: Dividend History

If you hold the dividend (now called IDCW — Income Distribution cum Capital Withdrawal) option, the factsheet shows the dividend history with amounts and dates. Remember that dividends from mutual funds are not free money — they are paid out of the fund's NAV, which falls by the dividend amount on the ex-dividend date. For most long-term investors, the growth option is more efficient because it avoids a dividend distribution tax event and keeps your corpus compounding.

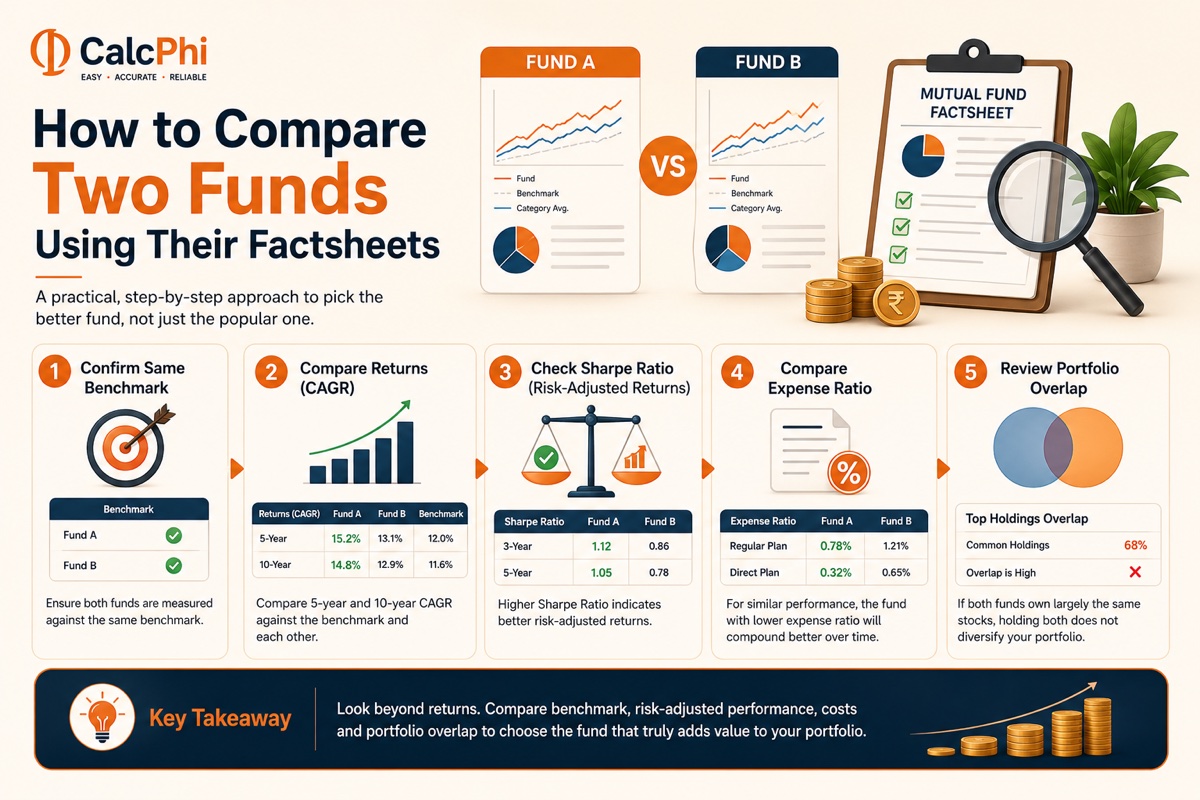

How to Compare Two Funds Using Their Factsheets

When you are choosing between two funds in the same category, here is a practical approach. First, confirm both have the same benchmark. Then compare their 5-year and 10-year CAGR against that benchmark and against each other. Next, check the Sharpe Ratio — the fund with a higher Sharpe Ratio is delivering better risk-adjusted returns. After that, compare the expense ratio; for two funds with similar performance, the one with a lower expense ratio will compound better over time. Finally, look at the sector allocation and top holdings — if both funds own largely the same stocks, holding both does not diversify you.

Frequently Asked Questions

-

What is the difference between absolute return and CAGR in a factsheet?

Absolute return is the total percentage gain from the day you invested to today, without adjusting for time. CAGR (Compounded Annual Growth Rate) expresses that gain as an annualised figure, making it comparable across different time periods. For any investment held more than one year, CAGR is the more meaningful metric to use.

-

A fund has a high Sharpe Ratio but a low 5-year return. Should I invest?

Not necessarily. A high Sharpe Ratio means the fund manages risk well relative to the returns it generates, but if the absolute return is below the category average or its benchmark, the fund may simply be too conservative for a long-term equity investor. Compare it with a passive index fund before deciding.

-

How often should I check a mutual fund factsheet?

Once a quarter is generally sufficient for long-term equity investors. You are looking for significant changes in fund manager, a sudden spike in expense ratio, major shifts in sector allocation, or sustained underperformance against the benchmark across three or more quarters. Monthly reviews can lead to unnecessary reactions to short-term noise.

-

Is a low Portfolio Turnover Ratio always better?

For most equity funds, a lower Portfolio Turnover Ratio is preferable because it signals disciplined investing and keeps transaction costs low. However, in certain market conditions — such as a sector rotation or economic shift — a fund manager may justifiably increase turnover to reposition the portfolio. Look at the context, not just the number in isolation.

-

What does it mean when a fund's alpha is negative?

Negative alpha means the fund has underperformed its benchmark after adjusting for market risk. Over one or two years, a negative alpha can be explained by market conditions. If the alpha has been negative for three or more consecutive years, the fund manager is consistently failing to add value, and you should consider switching to a passive alternative or a better-performing fund in the same category.

-

Where can I find the factsheet for a mutual fund?

Every AMC is required to publish factsheets on their official website. You can also find them on the AMFI website at amfiindia.com. Most investment platforms like Zerodha, Groww, and Kuvera also display key factsheet data on each fund's page.

Disclaimer: The information in this article is for educational and estimation purposes only. CalcPhi's calculators are tools to help you understand financial concepts and model scenarios — they do not constitute financial advice. Mutual fund investments are subject to market risk. Past performance is not a guarantee of future returns. Please consult a SEBI-registered financial advisor or certified financial planner before making any investment decisions.