How to Build an Emergency Fund in India 2026 — The Complete Guide

Most personal finance advice jumps straight to SIPs, tax saving, and stock portfolios. But there is one step that comes before all of that — one that most Indians skip entirely — and it is the reason why a single medical bill or a sudden job loss can unravel years of careful investing. That step is building an emergency fund: a dedicated pool of liquid money held outside your regular investments, accessible within 24 to 48 hours, and used exclusively for genuine financial emergencies. It exists so that when a real crisis hits, you do not have to break a long-term SIP, withdraw from your PPF prematurely, or take a personal loan at 14% interest to survive the month.

What Counts as a True Emergency?

Before you build one, you need to understand what an emergency fund is actually for. This is where most people go wrong — they treat it as a general savings buffer and keep dipping into it for non-emergencies.

A genuine financial emergency is an unexpected, urgent event that threatens your ability to meet your essential obligations. Job loss or sudden income disruption qualifies. A major medical expense not fully covered by insurance qualifies. An urgent home repair — a burst pipe, a failing water pump — qualifies. A car breakdown that prevents you from getting to work qualifies.

A planned home renovation, a scheduled vacation, a wedding three months away, or a new laptop for work do not qualify. These are foreseeable expenses that should be funded from a separate sinking fund, not from your emergency reserve. The cleaner you keep this boundary, the more reliably your emergency fund will be there when it truly matters.

How Much Emergency Fund Do You Need in India in 2026?

The globally accepted baseline is three to six months of essential monthly expenses. Essential expenses are not your total spending — they are the non-negotiable obligations you must meet regardless of circumstances: rent or home loan EMI, groceries, utility bills, school or college fees, insurance premiums, and minimum loan payments.

The right target for you depends on your personal risk profile:

Three months is appropriate if you are in a stable salaried role at a large MNC, government organisation, or PSU, and you have a dual-income household where a partner's salary can partly cover costs in a crisis.

Six months is the right target for most salaried employees in the private sector — particularly those in startups, mid-size companies, or industries prone to layoffs. Single-income households with dependants also fall in this bracket.

Nine to twelve months is the standard for freelancers, self-employed professionals, and business owners. Income irregularity is a structural feature of these setups — clients delay payments, projects end unexpectedly, and business cash flow can dry up for weeks.

| Monthly Essential Expenses | 3-Month Fund | 6-Month Fund | 9-Month Fund |

|---|---|---|---|

| ₹20,000 | ₹60,000 | ₹1,20,000 | ₹1,80,000 |

| ₹35,000 | ₹1,05,000 | ₹2,10,000 | ₹3,15,000 |

| ₹50,000 | ₹1,50,000 | ₹3,00,000 | ₹4,50,000 |

| ₹75,000 | ₹2,25,000 | ₹4,50,000 | ₹6,75,000 |

| ₹1,00,000 | ₹3,00,000 | ₹6,00,000 | ₹9,00,000 |

| ₹1,50,000 | ₹4,50,000 | ₹9,00,000 | ₹13,50,000 |

Essential expenses in Mumbai, Bengaluru, or Delhi are structurally higher than in Tier 2 cities, which means the rupee target for the same "3-month fund" can differ dramatically. A salaried employee in Pune might spend ₹35,000 per month on essentials, while someone in a similar role in Mumbai might spend ₹60,000. Calculate your own number — do not rely on averages.

Where to Keep Your Emergency Fund in India

Your emergency fund must satisfy three conditions at once: it must be instantly or near-instantly accessible, it must carry zero market risk, and it should earn a reasonable return so inflation does not erode its value over years. Here is how the main options compare in 2026.

High-Yield Savings Accounts at Small Finance Banks

Small Finance Banks (SFBs) like AU Small Finance Bank, Ujjivan Small Finance Bank, and Jana Small Finance Bank currently offer savings account interest rates between 5.5% and 7.5% per annum — significantly higher than the 2.7% to 3.5% offered by PSU banks. Deposits up to ₹5 lakh per account are covered under the DICGC scheme, making them as safe as any nationalised bank. Accessibility is instant — IMPS and UPI transfers work around the clock. For most people, this is the best place to hold the primary, immediately accessible portion of the emergency fund.

Liquid Mutual Funds

Liquid mutual funds invest in short-term government securities and money market instruments with maturities of up to 91 days. They are not equity funds — they have negligible volatility and are designed precisely for short-term parking of money. As of 2026, well-managed liquid funds are returning approximately 6.5% to 7.5% per annum. The redemption process is T+1: if you submit a redemption request before 1:30 PM on a business day, the money hits your bank account the next business day. Liquid funds work best for the larger portion of a sizeable emergency corpus (₹2 lakh and above).

Note that liquid fund gains are taxed as per your income tax slab under the new tax regime for AY 2026-27. For most people in the 20% or 30% tax slab, the post-tax return on a liquid fund yielding 7% is approximately 5.6% or 4.9% respectively — still better than a PSU savings account.

Fixed Deposits with Premature Withdrawal Facility

Short-duration FDs (3 to 12 months) at good rates work well as a second-tier emergency buffer. Most banks allow premature withdrawal with a penalty of 0.5% to 1%. FD rates at major private banks in 2026 range from 6.5% to 7.5% for short tenures. Use CalcPhi's FD Calculator to model exactly what your FD will earn, and the TDS on FD Calculator to estimate your after-tax maturity value if your interest crosses ₹40,000 per year.

The Recommended Split

A practical allocation for a ₹4,50,000 emergency fund (six months at ₹75,000/month expenses) might look like this:

- ₹75,000 in a high-yield savings account (SFB at 6–7%) — first line of defence for immediate needs, accessible via UPI within seconds

- ₹2,50,000 in a liquid mutual fund — accessible next business day, earns meaningfully more over time

- ₹1,25,000 in a short-term FD — second-tier buffer, slightly higher rate, redeemable within a day with a small penalty

What NOT to Use as an Emergency Fund

Equity Mutual Funds should never form part of your emergency fund. Markets are most likely to fall sharply during the same economic shocks that cause job losses and income disruptions. If your emergency fund lost 35% of its value precisely when you needed it most, it has failed its core purpose.

PPF and EPF are not accessible in a genuine emergency. PPF has a 15-year lock-in period, with partial withdrawals only allowed after the seventh financial year. EPF partial withdrawals require a documented reason and EPFO approval that can take several weeks. Neither is suitable.

NPS is a retirement vehicle with very limited withdrawal provisions before age 60. It has no role whatsoever in emergency planning.

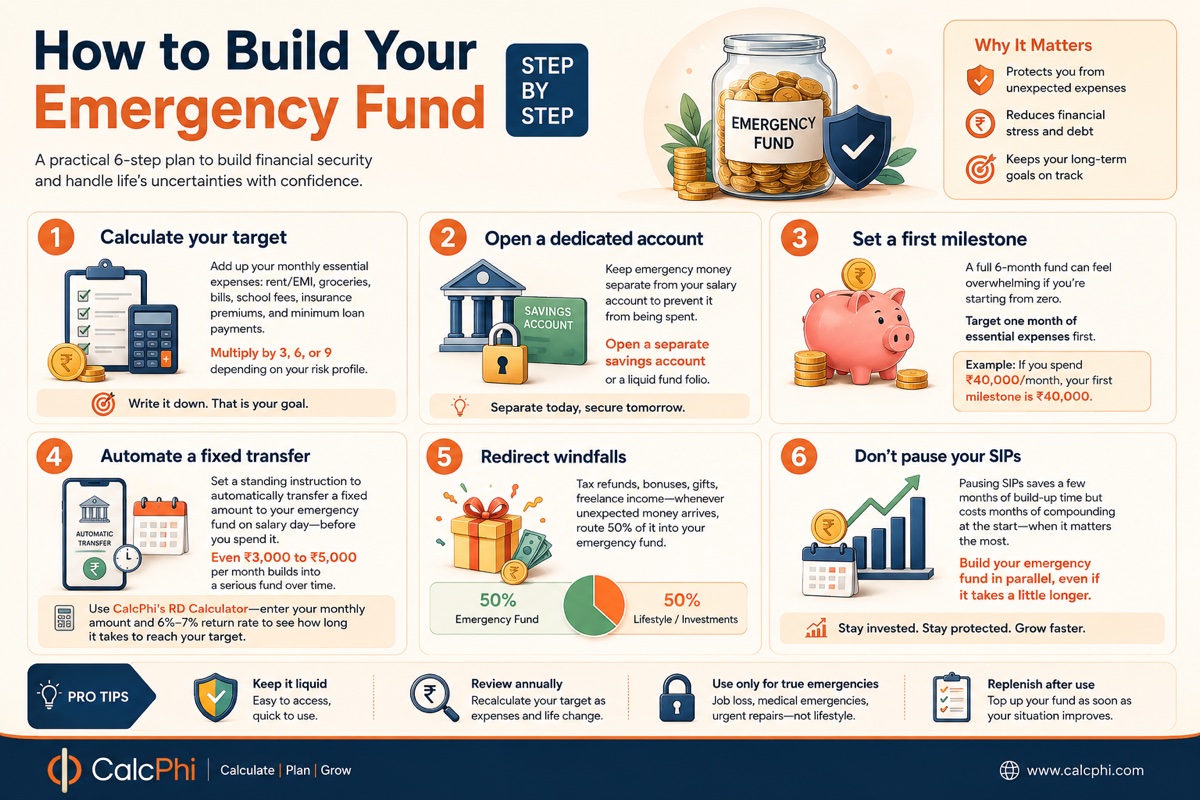

How to Build Your Emergency Fund Step by Step

Step 1 — Calculate your target. Add up your monthly essential expenses: rent or home loan EMI, groceries, electricity and water bills, children's school fees, health and term insurance premiums, and the minimum payment on any outstanding loans. Multiply by 3, 6, or 9 depending on your risk profile. Write down the number. That is your goal.

Step 2 — Open a dedicated account. The single most important behavioural trick is keeping emergency money in a separate account from your salary account. When they share a space, the emergency money tends to quietly disappear into ordinary spending. Open a separate savings account at a small finance bank, or create a separate liquid fund folio.

Step 3 — Set a first milestone of one month's expenses. A full six-month fund can feel like an impossible mountain if you are starting from zero. Break it down. Target one month of essential expenses first. For someone spending ₹40,000 per month, that is ₹40,000 — a reachable goal in two to three months for most salaries.

Step 4 — Automate a fixed transfer on salary day. Set a standing instruction with your bank to automatically transfer a fixed amount to your emergency fund account on the day your salary arrives — before you have a chance to spend it. Even ₹3,000 to ₹5,000 per month, transferred automatically, builds into a serious fund over time. Use CalcPhi's RD Calculator — enter your monthly contribution and a 6% to 7% return rate to see exactly how long it takes to reach your target.

Step 5 — Redirect windfalls. Tax refunds, annual bonuses, Diwali gifts, freelance income — whenever money arrives unexpectedly, route 50% of it into the emergency fund until the target is reached. The other 50% can go toward lifestyle or investments. This accelerates the build without requiring ongoing sacrifice.

Step 6 — Do not pause your SIPs to build it faster. Stopping a SIP to build an emergency fund faster saves a few months of build-up time but costs months of compounding at the beginning of your investment period — which is exactly when compounding matters most. Build the emergency fund in parallel, even if it takes a little longer.

How Long Will It Take? Real Salary Scenarios

| In-Hand Monthly Salary | Monthly Contribution to EF | Time to Build |

|---|---|---|

| ₹35,000 | ₹4,000/month | ~5 years (redirect windfalls) |

| ₹50,000 | ₹8,000/month | ~30 months |

| ₹70,000 | ₹12,000/month | ~20 months |

| ₹1,00,000 | ₹20,000/month | ~12 months |

| Any salary | Annual bonus of ₹2,40,000 | In one step |

For lower salary ranges, the build period is long — which is why redirecting windfalls matters so much. A single annual bonus or tax refund can cut years off the timeline.

The Emergency Fund and Your Tax Planning in 2026

Keeping your emergency fund in a high-yield savings account or liquid fund does generate taxable income. Interest earned in savings accounts is taxable as income from other sources. Under Section 80TTA, you can claim a deduction of up to ₹10,000 per year on savings account interest if you are below 60. Senior citizens can claim up to ₹50,000 under Section 80TTB (which also covers FD interest). For most people, the interest on an emergency fund of ₹3–5 lakh will fall well within these limits.

Liquid fund returns are taxed as short-term capital gains if redeemed within three years, at your applicable income tax slab rate. There is no special tax rate for debt fund gains following the Finance Act 2023 amendment. Use CalcPhi's Income Tax Calculator to factor emergency fund returns into your overall tax picture for the year.

Common Emergency Fund Mistakes to Avoid

Treating it as an investment. An emergency fund has a job: to be available in full, instantly, when disaster strikes. It is not trying to beat inflation. Putting it in a three-year FD or an equity fund to chase returns is a category error.

Not adjusting the target as life changes. An emergency fund that was right when you were single and renting may be woefully inadequate three years later when you have a home loan, a child, and an elderly parent financially dependent on you. Review your target at least once a year.

Using it for planned expenses. A vacation you planned six months ago is not an emergency. Dipping into the emergency fund for planned spending is the surest way to never actually have one. Build separate sinking funds for predictable large expenses.

Failing to replenish after a genuine withdrawal. If you do draw down the emergency fund for a real emergency, restoring it becomes the single highest financial priority once the crisis passes — above additional SIP investments, above discretionary saving, above everything except essential expenses and loan obligations.

Frequently Asked Questions

-

How much emergency fund is enough for a salaried person in India?

For a stable salaried employee in a large company or PSU, three months of essential expenses is adequate. For private sector employees, especially at startups or in volatile industries, six months is the right target. If you are the sole earner with dependants — including elderly parents or children — extend this to nine months. Calculate your essential monthly expenses (rent, EMI, food, utilities, insurance, loan minimums) and multiply accordingly.

-

Where is the best place to keep an emergency fund in India in 2026?

The best setup is a two-part structure: keep 15–20% of the fund in a high-yield savings account at a small finance bank (earning 6–7%, instantly accessible via UPI) and the remaining 80–85% in a liquid mutual fund (earning 6.5–7.5%, accessible within one business day). Avoid equity mutual funds, PPF, NPS, and long-duration FDs — none of these meet the liquidity and stability criteria an emergency fund requires.

-

Should I start a SIP or build an emergency fund first?

Do both simultaneously, but start with a starter emergency fund. Build a one-month expense buffer first — this takes two to four months for most salaries. Then start your SIP while continuing to grow the emergency fund in parallel. Do not delay SIP investments entirely, as the compounding benefit of starting early is very significant over a 10–20 year horizon. The right allocation is roughly 30–40% of monthly savings toward the emergency fund until it reaches your target, then redirect that portion to investments.

-

Is a liquid fund better than a savings account for an emergency fund?

For amounts above ₹1–2 lakh, yes. Liquid funds earn meaningfully more (6.5–7.5%) with T+1 redemption — money arrives the next business day. For truly immediate needs, keep a smaller portion in a high-yield savings account. The limitation of liquid funds is the one-day delay and the fact that redemptions on weekends or holidays take longer. For most non-immediate emergencies, T+1 is entirely adequate.

-

Can I count my EPF or PPF as part of my emergency fund?

No. EPF partial withdrawals require documented reasons and EPFO approval, which typically takes several weeks. PPF allows partial withdrawal only after the seventh financial year and only up to 50% of the balance at the end of the fourth year preceding the withdrawal year. Neither is accessible quickly enough to serve as an emergency fund, and both are earmarked for retirement. Treat them as completely separate pools of money.

-

What is the ideal emergency fund size for a freelancer or self-employed person in India?

Twelve months of essential expenses is the standard recommendation for freelancers and self-employed professionals in India. Income irregularity, delayed client payments, project droughts, and the absence of an employer's PF contribution all increase financial exposure. Some financial planners recommend splitting this: maintain six months in liquid instruments and keep a separate business contingency fund of three months for business expenses like subscriptions, tools, and vendor payments.

Disclaimer: The information in this article is for educational and general informational purposes only. CalcPhi calculators are estimation tools and do not constitute personalised financial advice. Emergency fund targets, interest rates, and tax rules mentioned reflect general market conditions as of May 2026 and may change. Please consult a SEBI-registered financial advisor or qualified Certified Financial Planner (CFP) for advice tailored to your individual financial situation.