Home Loan vs Renting in India: What the Real Numbers Say in 2026

Every Indian household has had this conversation. A parent insists that paying rent is a waste of money and that a home of your own is the only sensible goal. A younger sibling who just got a job in Bangalore wonders whether locking ₹20 lakh into a down payment makes any sense when they might switch cities in three years. Both of them are arguing without numbers.

In 2026, with home loan rates hovering between 7.50% and 8.70% p.a. at leading banks and rents rising 7–9% annually across major metros, this question deserves a proper answer — one built on rupees and percentages, not sentiment. This article breaks down the true cost of buying versus renting across India's major cities, city by city, so you can make the decision that actually fits your situation.

Why Comparing EMI to Rent Is the Wrong Starting Point

Most people settle this debate by comparing monthly EMI to monthly rent. If the EMI is ₹45,000 and comparable rent is ₹28,000, they conclude that renting is cheaper by ₹17,000 a month and move on. This comparison is dangerously incomplete.

It ignores the down payment you lock up, the one-time transaction costs of buying, the ongoing cost of maintenance and society charges, the property tax, and most importantly, the opportunity cost of every rupee tied up in the property rather than working for you elsewhere. When you factor all of these in, the true annual cost of owning a home in a metro can be 60–80% higher than what the EMI alone suggests.

Equally, the case for renting falls apart if you spend the difference rather than invest it. The numbers only work in the renter's favour when the savings are put to work systematically.

The True Annual Cost of Buying in 2026

What a Home Actually Costs You Each Year

Take a 2BHK flat in Bangalore's Whitefield area — a typical purchase for a tech professional. The property is priced at ₹90 lakh. You arrange a 20% down payment of ₹18 lakh and take a home loan of ₹72 lakh at 8.5% p.a. over 20 years from SBI or HDFC Bank. Your EMI comes to approximately ₹62,600 per month, or ₹7.51 lakh per year. But here is what the full annual cost looks like:

| Cost Item | Annual Amount (Approx.) |

|---|---|

| Home loan EMI (₹72L @ 8.5%, 20 yr) | ₹7,51,200 |

| Society maintenance charges | ₹48,000 |

| Property tax (BBMP, Whitefield zone) | ₹15,000 |

| Home insurance | ₹8,000 |

| Maintenance and repairs (avg. 0.5% of value) | ₹45,000 |

| Total Annual Ownership Cost | ₹8,67,200 |

The same 2BHK in Whitefield rents for ₹28,000–₹35,000 per month in 2026, or approximately ₹3.36–4.2 lakh per year. Buying costs you ₹4.5–5.3 lakh more per year than renting the same flat — and that is before factoring in the opportunity cost of your ₹18 lakh down payment.

If that ₹18 lakh were invested in an equity mutual fund earning 12% p.a. (the long-term historical CAGR of diversified Indian equity funds), it would generate ₹2.16 lakh in year one alone. Over 10 years, the same ₹18 lakh grows to approximately ₹55.8 lakh at 12% CAGR. That is a real cost of buying that never appears in any bank brochure.

Want to see how these numbers look for your specific loan amount and interest rate? Use CalcPhi's free EMI Calculator — enter your loan amount, rate, and tenure to instantly see your EMI, total interest payable, and year-by-year breakdown.

The One-Time Costs of Buying Nobody Talks About

Beyond the annual running costs, buying a home in India involves significant upfront transaction expenses that most buyers underestimate. For the ₹90 lakh Bangalore flat, here is what you pay before moving in:

Stamp duty in Karnataka is 5% for properties above ₹45 lakh — that is ₹4.5 lakh. Registration charges add another 1% (₹90,000). Legal fees, franking charges, and loan processing fees add ₹30,000–₹50,000. If you are buying through a broker, add another 1–2% of the property value (₹90,000–₹1.8 lakh). Total transaction costs can easily reach ₹6–7 lakh before you receive your keys.

These costs must be recovered through capital appreciation before you even start building wealth from the purchase. In a market appreciating at 7–8% annually, it takes roughly 12–18 months of appreciation just to recover your entry costs. If you sell within 3–4 years, there is a strong chance you exit at a net loss after accounting for transaction costs in both directions.

City-by-City: Where Buying Makes More or Less Sense

India is not one property market. The rent-versus-buy equation looks completely different in Mumbai than it does in Ahmedabad. The key metric to watch is the price-to-rent ratio — the purchase price divided by annual rent for the same property. The lower this number, the more financially attractive buying becomes.

Mumbai: The Hardest City to Justify Buying

In Mumbai, the price-to-rent ratio ranges from 30–45x, making it one of the toughest cities in the world to make a financial case for buying. Mumbai's gross rental yield is approximately 3.84% — meaning if you buy a ₹1.5 crore flat, the annual rent it generates (or saves you) is only ₹5.76 lakh, while the interest cost alone on a ₹1.2 crore loan at 8.5% is over ₹10 lakh in year one.

A 2BHK in Andheri or Goregaon costs ₹1.4–1.8 crore. The same flat rents for ₹35,000–₹50,000 per month. If you buy at ₹1.6 crore with 20% down and borrow ₹1.28 crore at 8.5% over 20 years, your EMI alone is ₹1.11 lakh/month. The renter of the same flat pays ₹42,000/month and has ₹69,000 per month extra to invest. Over 20 years, that ₹69,000/month invested at 10% annual returns grows to over ₹5.3 crore.

For Mumbai, the financial mathematics almost always favour renting and investing the difference — unless you are buying with a large down payment (40%+) or your investment discipline is poor and you need the forced savings mechanism of a home loan.

Bangalore: Reasonable Ratios in Tech Corridors

Bangalore presents a more balanced picture. Bangalore's rental yield stands at 3–3.5% and the tech corridors of Whitefield, Electronic City, and Sarjapur Road have seen 15% property appreciation in recent years. At that appreciation rate, a ₹90 lakh flat gains ₹13.5 lakh in value in year one — partially offsetting the higher annual cost of ownership versus renting.

The break-even in Bangalore's IT zones, assuming 10–12% annual appreciation, falls around 7–9 years. For a software professional planning to stay in Bangalore long-term, buying in an established tech corridor is a defensible financial decision. For someone on a 3-year project or exploring a startup, renting is clearly smarter.

Delhi NCR: Varies Wildly by Micro-Market

Delhi yields an estimated 5.81% gross rental yield — significantly higher than Mumbai — which makes parts of Delhi NCR more amenable to buying. Property in Gurugram appreciated 10% while Noida maintained 6–7% steady increases.

In Noida and Greater Noida, 2BHK flats are priced at ₹50–70 lakh with rents of ₹18,000–₹25,000/month. At a price-to-rent ratio of 20–25x, the financial case for buying is much closer to neutral, and with good capital appreciation history, buying in well-connected Noida sectors can make sense for 5+ year horizons. In South Delhi and Gurugram prime localities, prices are significantly higher and the ratio tilts toward renting again.

Tier-2 Cities: Where Buying Often Wins

In cities like Pune, Hyderabad, Ahmedabad, Coimbatore, Jaipur, and Indore, the rent-versus-buy equation shifts noticeably in favour of buying. Price-to-rent ratios in these markets frequently fall in the 12–18x range. A 2BHK in Pune's Kharadi might cost ₹65 lakh and rent for ₹22,000–₹26,000/month (₹2.64–3.12 lakh/year) — a ratio of roughly 20x at most. With Pune appreciating at 7–9% annually and rental yields at 4–5%, the annual cost gap between owning and renting narrows sharply. In many pockets, break-even arrives within 4–6 years.

| City / Market | Approx. Price-to-Rent Ratio | Verdict |

|---|---|---|

| Mumbai (Andheri, Goregaon) | 30–45x | Strongly favours renting |

| Delhi (South Delhi, prime Gurugram) | 25–35x | Favours renting |

| Bangalore (Whitefield, Electronic City) | 22–28x | Neutral to renting; break-even ~7–9 yr |

| Delhi NCR (Noida, Greater Noida) | 20–25x | Neutral; consider for 5+ yr horizon |

| Pune (Kharadi, Hinjawadi) | 15–20x | Favours buying for 5+ yr |

| Hyderabad, Ahmedabad, Indore | 12–18x | Clearly favours buying for 5+ yr |

The Renter's Advantage — And Its Biggest Risk

If you rent a 2BHK in Bangalore for ₹30,000/month instead of buying the same flat with an EMI of ₹63,000/month, you free up ₹33,000/month. Over 20 years, that ₹33,000/month invested through a monthly SIP in a diversified equity mutual fund at 12% CAGR would grow to approximately ₹3.3 crore.

The property you didn't buy might be worth ₹2.5–3.5 crore in 20 years (at 5–7% CAGR). Factor in the equity you would have built through EMI repayments, and the two outcomes are broadly comparable — with the property giving you a tangible asset and the SIP giving you liquidity and flexibility.

But this only works if you actually invest the ₹33,000 every month without fail. In practice, many renters spend the difference. A lifestyle upgrade, a new car, vacations, gadgets — the savings evaporate. Homeownership forces the savings discipline that renting requires you to impose on yourself. If you know your financial willpower is limited, the forced savings mechanism of a home loan has real value that a spreadsheet cannot capture.

Curious what a monthly SIP of ₹33,000 would grow to over your own time horizon? Try CalcPhi's SIP Calculator and see your projected corpus in seconds — no sign-up needed.

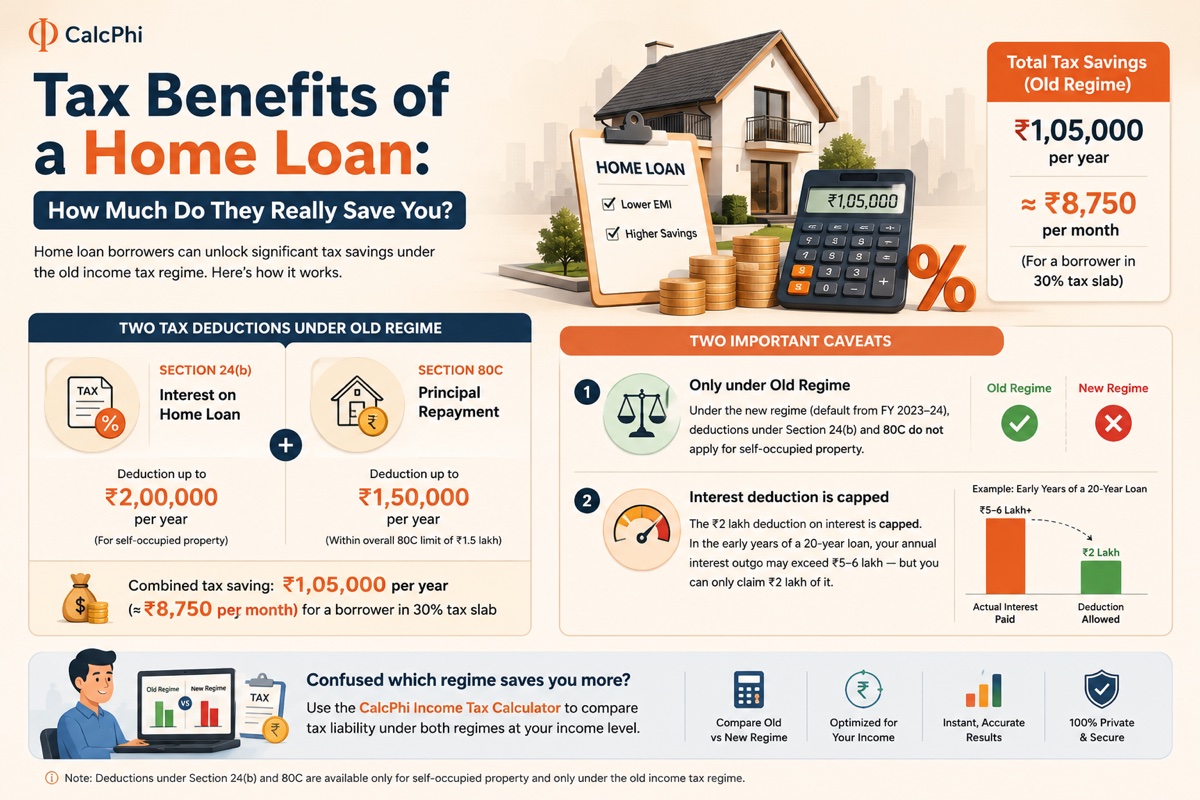

Tax Benefits of a Home Loan: How Much Do They Really Save You?

Indian home loan borrowers get two meaningful tax deductions under the old income tax regime. Under Section 24(b) of the Income Tax Act, you can deduct up to ₹2 lakh per year on interest paid on a home loan for a self-occupied property. Under Section 80C, principal repayment qualifies for deduction up to ₹1.5 lakh per year as part of the combined 80C ceiling. Combined, a borrower in the 30% tax slab saves approximately ₹1.05 lakh annually in tax — roughly ₹8,750 per month.

Two important caveats apply. First, these deductions are only available under the old tax regime. Under the new regime — now the default from FY 2023–24 — home loan deductions under Section 24(b) and 80C do not apply for self-occupied property. If you are already in the new regime for the lower slab rates, you lose these benefits. Second, the ₹2 lakh deduction on interest is capped. In the early years of a 20-year loan, your annual interest outgo may well exceed ₹5–6 lakh — but you can only claim ₹2 lakh of it. The tax benefit covers only a fraction of your actual interest cost.

If you are planning to buy and want to see which tax regime saves you more after accounting for home loan deductions, check the CalcPhi Income Tax Calculator — it compares both regimes side by side at your income level.

The Break-Even Period: How Long Before Buying Beats Renting?

The break-even period is the number of years you need to hold a property before the financial benefits of ownership — mainly capital appreciation and principal build-up — outweigh the higher annual cost of owning versus renting. This is the single most useful number in this entire debate, and it is specific to your city and property.

A simple rule of thumb: divide the property price by the annual rent it would otherwise cost you. If that ratio is below 15, buying is likely to break even within 5–7 years. If the ratio is between 15 and 25, break-even takes 7–12 years. If it exceeds 25 (as it does in most of Mumbai and parts of Delhi and Bangalore), you need to hold the property for 12–20 years before buying clearly beats renting on a pure wealth basis.

The transaction costs of buying and selling compound this. Stamp duty, registration, legal fees, and brokerage on both ends of the transaction can easily total 8–10% of the property value. On a ₹90 lakh flat, that is ₹7.2–9 lakh in irreversible sunk costs. These costs need to be amortised across your holding period. The shorter you hold, the heavier the burden per year.

If you are planning to stay in your current city for at least 7–10 years, have a stable income, and can comfortably manage the EMI without stretching beyond 40% of your take-home salary, buying is worth a serious financial analysis. If any of those three conditions are uncertain, renting gives you options that buying does not.

When Buying Is Clearly the Right Answer

Buying makes strong financial sense in India when you meet a clear set of conditions: you plan to stay in the same city for at least 7 years; your combined EMI across all loans does not exceed 40–45% of your net monthly take-home pay; you have a 20% down payment ready without liquidating emergency funds or retirement savings; your credit score is 750 or above, qualifying you for the sharpest rates from SBI or HDFC; and you are buying in a city or corridor with genuine long-term demand — a strong employment base, infrastructure investment, and population inflow.

Under these conditions, and especially in Tier-2 cities where price-to-rent ratios are reasonable, buying builds wealth in a structured, predictable way that most renters struggle to match through voluntary investing.

When Renting Is the Smarter Financial Move

Renting wins — financially — when your price-to-rent ratio is above 25x, your expected stay is under five years, your income is variable or you are between jobs, your down payment would need to come from savings earmarked for other goals, or you are early in your career and your city of work is likely to change.

Renting also gives you something buying cannot: optionality. If your company shifts you to another city, if a better job comes up in a different metro, or if you simply decide you want more space or a different neighbourhood, renting allows you to act on those changes within weeks. Selling a property takes months, involves significant transaction costs, and can go wrong in a slow market.

Run Your Own Numbers Before You Decide

Every scenario in this article is based on typical figures for each city, but your decision depends on your specific loan amount, your exact interest rate, the property you are considering, and the alternative you would pursue with the money you save by renting.

CalcPhi's EMI Calculator will show you your exact monthly EMI, the total interest you pay over the tenure, and the full amortisation schedule — so you can see how much of your early repayments are interest versus principal. For a ₹72 lakh loan at 8.5% over 20 years, you pay ₹77.5 lakh in interest alone. That is more than the original loan — and knowing it upfront helps you plan a prepayment strategy.

If you are weighing the renting-and-investing alternative, CalcPhi's SIP Calculator lets you enter any monthly amount and return assumption to see what your corpus would be at 10, 15, or 20 years. Running both numbers side by side is the only honest way to compare.

FAQs: Home Loan vs Renting in India 2026

-

Is buying a home always better than renting in India?

No. In high price-to-rent ratio cities like Mumbai (30–45x) and large parts of Bangalore and Delhi, renting and systematically investing the difference in equity mutual funds can build more wealth over 15–20 years than buying. In Tier-2 cities where price-to-rent ratios are 12–20x, buying often makes clearer financial sense for those with a 7+ year horizon and a stable income.

-

What is the current home loan interest rate in India in 2026?

As of May 2026, home loan rates start from 7.50% p.a. at SBI (ranging up to 8.70% based on CIBIL score) and from 7.75% p.a. at HDFC Bank. The RBI repo rate is 5.25% (held steady at the April 2026 MPC meeting), keeping floating-rate EMIs broadly stable. Public sector banks like SBI and Bank of Baroda generally offer the sharpest rates for borrowers with CIBIL scores above 750.

-

How much down payment do I need to buy a home in India?

Most banks finance up to 75–80% of the property value, requiring a down payment of 20–25%. For a ₹80 lakh property, that means ₹16–20 lakh upfront — before stamp duty, registration, and other transaction costs, which can add another ₹5–7 lakh. Arranging a full 20% down payment plus transaction costs without dipping into emergency funds is the baseline financial readiness test before buying.

-

What tax benefits do I get on a home loan in India in 2026?

Under the old income tax regime, Section 24(b) allows a deduction of up to ₹2 lakh per year on interest paid for a self-occupied property, and Section 80C allows deduction of principal repayment up to ₹1.5 lakh per year. At the 30% tax bracket, this saves approximately ₹1.05 lakh annually. These deductions are not available under the new tax regime for self-occupied property, so borrowers must evaluate which regime is more beneficial at their income level.

-

How do I calculate whether buying or renting is cheaper in my city?

Use the price-to-rent ratio: divide the purchase price of a property by its annual rent. A ratio below 15 generally favours buying, 15–20 is neutral, and above 20 generally favours renting. Mumbai typically sits at 30–45x (strongly favour renting), while Tier-2 cities often sit at 12–18x (favour buying). Factor in your planned holding period — transaction costs mean buying only makes mathematical sense if you hold for at least 5–7 years.

-

Can I use a home loan to buy a house and also invest in SIPs simultaneously?

Yes, and many financial planners recommend this approach for moderate-income buyers. If your EMI is manageable at 35–40% of take-home pay, the remaining income can be allocated to SIPs in equity mutual funds. This builds a liquid investment corpus in parallel with the home equity you are building through EMI repayments — a diversified approach to long-term wealth creation. Use CalcPhi's SIP Calculator to see how a parallel SIP grows alongside your property.

The Bottom Line

The home loan versus renting decision in India in 2026 does not have one universal answer. In Mumbai and other high-ratio metros, renting is often the sharper financial move — but only if you have the discipline to invest the difference. In Tier-2 cities with reasonable price-to-rent ratios and strong appreciation, buying for the long term builds wealth in a reliable, structured way.

The honest framework is simple: calculate your true annual cost of ownership (not just the EMI), compare it to rent, work out how long you plan to stay, and model what you would do with the difference if you rented instead. If those numbers work in favour of buying and you are financially prepared, buy. If they don't, renting is not throwing money away — it is keeping your options open while you build wealth another way.

Disclaimer:All figures in this article are for educational and estimation purposes only and do not constitute financial or investment advice. Home loan interest rates, tax rules, property prices, and rental values are subject to change. Consult a SEBI-registered financial adviser or qualified CA before making any property purchase or borrowing decision.