FIRE in India: The Complete Math Behind Retiring at 40

Retiring at 40 in India is not a fantasy reserved for tech entrepreneurs or stock market prodigies. It is a mathematical problem — and like all math problems, it has a solution. The question is not whether it is possible. The question is: what does the math actually look like, and are you willing to work the numbers?

This article breaks down every piece of the FIRE (Financial Independence, Retire Early) puzzle specifically for the Indian context — inflation, tax laws, investment instruments, and the real corpus you need to never work again by the time you turn 40.

What FIRE at 40 Actually Means in the Indian Context

FIRE stands for Financial Independence, Retire Early. The "retire early" part does not necessarily mean doing nothing for the rest of your life. For most people who pursue FIRE in India, it means reaching a point where work becomes optional — where your investment returns cover your living expenses permanently, whether you keep working or not.

Retiring at 40 is the most aggressive version of FIRE. If you are an average Indian professional who started working at 22 or 23, you have roughly 17 to 18 years to build a corpus large enough to last 45 or more years. That is a long retirement — longer than most careers. And that is precisely why the math needs to be exact, not approximate.

India adds specific complexity to the FIRE formula. Our inflation averages 6 to 7 percent annually, compared to 2 to 3 percent in the United States where most FIRE literature originates. Our healthcare system is largely out-of-pocket. Tax rules around capital gains and withdrawals affect how much of your corpus you actually get to keep. All of this has to be factored into your number.

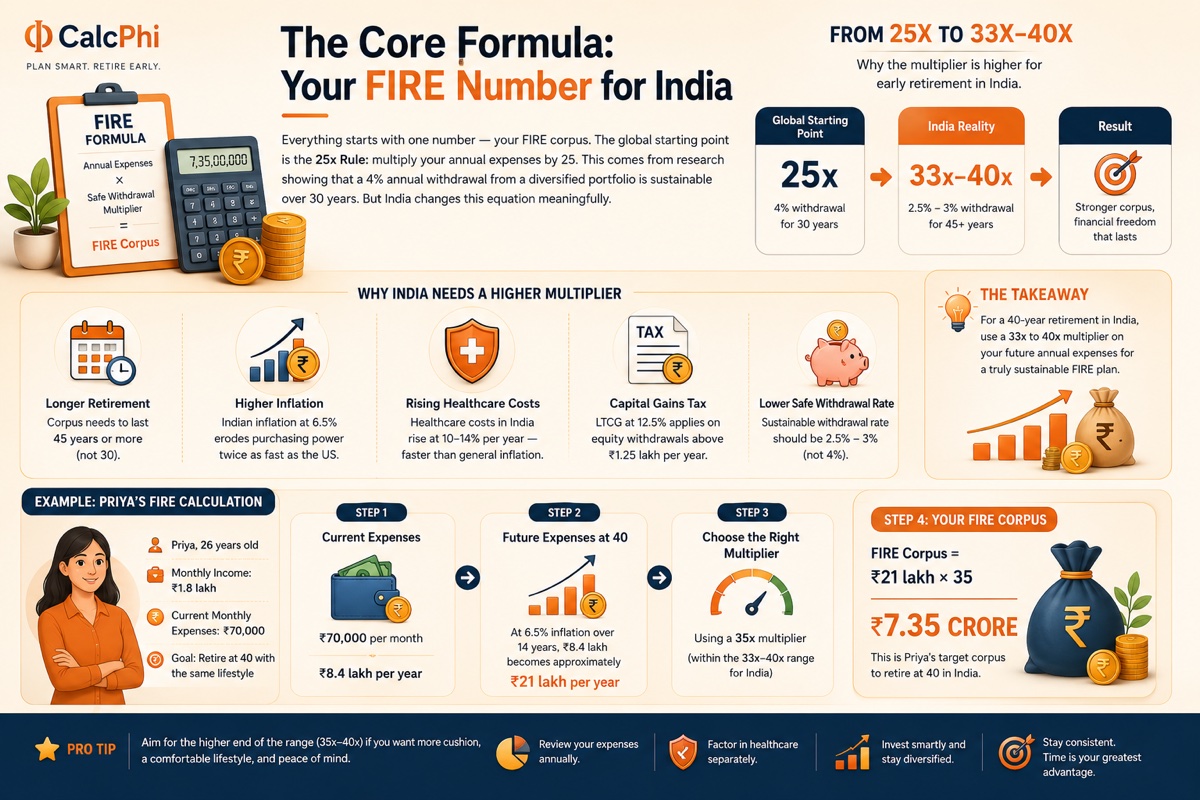

The Core Formula: Your FIRE Number for India

Everything starts with one number — your FIRE corpus. The global starting point is the 25x Rule: multiply your annual expenses by 25. This comes from research showing that a 4% annual withdrawal from a diversified portfolio is sustainable over 30 years. But India changes this equation meaningfully.

For someone retiring at 40 in India, the safe withdrawal rate should be closer to 2.5 to 3 percent, because:

- Your corpus needs to last 45 or more years (not 30)

- Indian inflation at 6.5% erodes purchasing power twice as fast as the US

- Healthcare costs in India rise at 10 to 14 percent per year — faster than general inflation

- Capital gains tax on equity withdrawals applies above ₹1.25 lakh per year (LTCG at 12.5% post-2024 Budget)

This means the multiplier jumps from 25x to 33x to 40x annual expenses for a 40-year retirement target.

Let's work through a realistic example. Priya is 26, earns ₹1.8 lakh a month, and currently spends ₹70,000 a month. She wants to retire at 40 with the same lifestyle.

- Current monthly expenses: ₹70,000 → Annual: ₹8.4 lakh

- At 6.5% inflation over 14 years, ₹8.4 lakh becomes approximately ₹21 lakh per year by age 40

- Using a 35x multiplier: FIRE Corpus = ₹21 lakh × 35 = ₹7.35 crore

That is the target. Want to calculate your own FIRE number based on your current expenses and retirement age? Use CalcPhi's free Goal-Based SIP Calculator to find out exactly how much you need to invest every month to hit your target corpus in 14 years.

The Accumulation Phase: Building ₹7+ Crore in 14 Years

The accumulation phase is the period between now and your retirement date — the years when you are earning, saving aggressively, and investing systematically. For a 40-year FIRE target, this window is typically 14 to 18 years depending on when you start.

Equity Mutual Funds via Step-Up SIP

The engine of any early retirement plan in India is equity mutual funds, specifically through a Systematic Investment Plan (SIP) that increases every year as your income grows. A flat SIP is good. A step-up SIP — where you increase the monthly amount by 10 to 15 percent annually — is transformational.

Returning to Priya's example: she needs ₹7.35 crore in 14 years. At an assumed 12% CAGR (reasonable for diversified equity funds over a 12 to 15 year horizon), here is what different SIP strategies look like:

| Strategy | Monthly SIP (Starting) | Annual Step-Up | Corpus at Year 14 |

|---|---|---|---|

| Flat SIP | ₹2,00,000/month | 0% | ~₹6.8 crore |

| Step-Up SIP | ₹1,20,000/month | 10%/year | ~₹7.1 crore |

| Aggressive Step-Up | ₹90,000/month | 15%/year | ~₹7.4 crore |

The step-up approach lets you start at a more manageable amount and increase contributions as your salary grows — which is exactly how most careers work. Use CalcPhi's Step-Up SIP Calculator to model your exact numbers and see precisely which combination hits your FIRE corpus.

The 50-30-20 Savings Rate for FIRE at 40

Standard financial advice suggests saving 20 percent of your income. FIRE at 40 requires something more aggressive — typically a 50 to 60 percent savings rate for most of the accumulation phase. That sounds extreme until you run the numbers and realise how little time you are giving compound interest to work.

The reason savings rate matters so much is dual: a higher savings rate both grows your corpus faster AND signals that your lifestyle is cheaper to sustain, which lowers your FIRE number. Someone spending ₹50,000 a month instead of ₹1 lakh a month needs roughly half the corpus AND accumulates wealth twice as fast. This is the central tension of FIRE at 40 in India: aggressive lifestyle optimisation now in exchange for complete freedom later.

Tax Efficiency: Keeping More of What You Earn

Taxes are the silent killer of FIRE plans. Every rupee lost to inefficient taxation is a rupee that cannot compound for the next 14 years. Getting your tax structure right during the accumulation phase can add 10 to 20 percent to your final corpus — without any additional investing.

Section 80C: Use Every Rupee

The ₹1.5 lakh annual deduction under Section 80C is non-negotiable for anyone building toward FIRE. The most efficient way to use it for a FIRE goal:

- ELSS (Equity Linked Savings Schemes): Three-year lock-in, equity exposure, and tax deduction combined. The best 80C instrument for wealth building. Use CalcPhi's ELSS Calculator to model the post-tax return versus a regular equity fund.

- PPF: ₹1.5 lakh per year at 7.1%, fully tax-free on maturity. Zero credit risk. Ideal as your debt allocation within the 80C bucket.

New vs Old Tax Regime: Which Works for FIRE Builders?

This decision significantly affects how much you keep from each paycheck and route to investments. At incomes above ₹15 lakh with significant deductions (80C + 80D + HRA), the old regime typically saves more tax. Below ₹10 lakh, the new regime is often better. Use CalcPhi's New vs Old Tax Regime Calculator to compare both regimes at your exact income level — the difference can easily be ₹30,000 to ₹80,000 per year, which is ₹30,000 to ₹80,000 more that can go into your SIP.

Capital Gains Tax in the Withdrawal Phase

Once you retire at 40, your income will primarily come from selling equity mutual fund units. Under current rules (post-2024 Budget), Long-Term Capital Gains (LTCG) on equity above ₹1.25 lakh per year are taxed at 12.5% without indexation. Short-Term Capital Gains (STCG, held less than one year) are taxed at 20%. Smart early retirees structure withdrawals to stay below the LTCG threshold where possible, using a combination of instruments to minimise the tax bite.

The Withdrawal Phase: Making Your Corpus Last 45 Years

Building the corpus is only half the problem. The second half — making ₹7+ crore sustain you from age 40 to 85 or beyond — requires its own strategy.

The Bucket System for Indian Early Retirees

A proven approach for managing a FIRE portfolio in India is the three-bucket system, where you segment your corpus by time horizon:

Bucket 1 — Short-term (0 to 3 years): Keep 2 to 3 years of living expenses in liquid funds or short-duration debt funds. This is your buffer that you draw from month to month, so equity market downturns never force you to sell equities at a loss.

Bucket 2 — Medium-term (3 to 10 years): PPF, corporate bond funds, and balanced advantage funds sit here. They generate moderate returns with lower volatility than pure equity.

Bucket 3 — Long-term growth (10+ years): The bulk of your corpus stays in diversified equity mutual funds — large-cap, flexi-cap, or index funds. This is your engine against inflation over the remaining decades.

When equity markets fall, you live off Bucket 1. When markets recover, you rebalance and refill Bucket 1. You never sell equity in a panic.

Inflation Is the Biggest Risk in a 45-Year Retirement

At 6.5% inflation, your expenses double every 11 years. The ₹1 lakh a month you retire on at 40 becomes ₹2 lakh by 51, ₹4 lakh by 62, and ₹8 lakh by 73. Your corpus and its returns must keep pace with this escalation across four-plus decades.

This is why the equity component cannot be eliminated even after retirement. A portfolio that shifts entirely to fixed deposits or debt funds at 40 will likely run out of money by the early 60s, because FD returns (currently 7 to 7.5%) barely keep pace with inflation and are fully taxable. Use CalcPhi's Inflation-Adjusted Returns Calculator to see what your current SIP corpus will actually be worth in today's rupees at your retirement date.

The FIRE at 40 Roadmap: Ages 26 to 40

Ages 26 to 30 — Build the foundation. Start your SIP (even ₹20,000 to ₹30,000 monthly), maximise 80C deductions, open a PPF account, and build an emergency fund equal to 6 months of expenses. Get a term insurance policy — the earlier you buy it, the cheaper it is, and it protects your family if anything happens before you hit your FIRE number.

Ages 30 to 35 — Scale aggressively. Your income should be meaningfully higher. Increase your SIP by 15 percent or more annually. Explore ELSS for tax-efficient equity exposure. Consider NPS for the additional ₹50,000 deduction under Section 80CCD(1B) — this is free tax saving that most people leave on the table.

Ages 35 to 40 — Fine-tune and protect. Your corpus is now large enough that you are also managing concentration and sequence-of-returns risk. Start shifting a portion into debt instruments (Bucket 1 and 2) so you are not 100% in equity right before retirement. Lock in your healthcare plan — private health insurance well before age 40, because premiums and eligibility get complicated as you age.

Healthcare: The Wildcard in Every Indian FIRE Plan

No Indian FIRE plan is complete without a serious healthcare provision. Medical inflation at 10 to 14 percent annually means healthcare costs double every 5 to 7 years. A 40-year-old retiring in 2026 will face healthcare costs in their 70s that are 15 to 20 times higher in nominal terms than today.

Practical steps: Get a comprehensive family health insurance policy with a ₹1 crore cover. Top it up with a super top-up plan for catastrophic events. And separately, allocate a dedicated healthcare corpus within your FIRE number — typically 15 to 20 percent of the total corpus earmarked specifically for medical costs that insurance will not cover. This is one of the most overlooked parts of Indian FIRE planning, and it is one of the most dangerous gaps to have.

City-by-City FIRE Numbers: Mumbai vs Bengaluru vs Hyderabad

Your FIRE corpus is not a universal number — it is determined by where you live. Monthly expenses vary by ₹40,000–₹80,000 between India's major metros, translating to a ₹1.2–2.4 crore difference in required corpus at a 4% withdrawal rate. For a couple with two children retiring at 40 in 2026:

Mumbai (Andheri West, 2BHK): Rent ₹65,000 + groceries ₹18,000 + school fees ₹30,000 + utilities ₹12,000 + lifestyle ₹20,000 + health insurance ₹18,000 = ₹1,63,000/month = ₹19.56 lakh/year. At 4% SWR: ₹4.89 crore required. With 6% inflation buffer over 30 years: ₹6.5–7 crore.

Bengaluru (Whitefield, 3BHK): ₹1,29,000/month = ₹15.48 lakh/year. At 4% SWR: ₹3.87 crore required. Real corpus with inflation buffer: ₹5–5.5 crore.

Hyderabad (Kondapur, 3BHK): ₹1,07,000/month = ₹12.84 lakh/year. At 4% SWR: ₹3.21 crore required. Real corpus with inflation buffer: ₹4–4.5 crore.

The ₹56,000/month gap between Mumbai and Hyderabad represents a ₹1.68 crore difference in corpus at 4% SWR. Many FIRE practitioners accumulate in a high-income metro and retire to a lower-cost city — reducing the corpus needed by ₹1.5–2 crore, shaving 2–3 years off the accumulation timeline. Use the Retirement Corpus Calculator to model your specific city's cost assumptions.

Your Next Steps: How to Use These Numbers

Here is what to do after reading this article. First, calculate your own FIRE number: take your current monthly household spend, add 30% for lifestyle inflation, and multiply by 300 (the 25x rule on annual spend, adjusted for Indian inflation). That is your starting corpus target. Next step: open the SIP Calculator, enter your target corpus, your current savings rate, and your expected FIRE age, and find the monthly investment required. If the number feels too high, run it again with a 15-year horizon instead of 14 — the monthly SIP required drops significantly because of an extra year of compounding. The goal of this exercise is not a perfect plan — it is a first number you can react to and refine.

Frequently Asked Questions

-

How much corpus do I need to retire at 40 in India?

The answer depends on your monthly expenses, but as a rule of thumb, plan for 33 to 40 times your annual expenses at retirement (in inflation-adjusted terms). For someone spending ₹1 lakh a month today and retiring in 14 years, the target corpus is roughly ₹7 to 9 crore, depending on inflation assumptions and the safe withdrawal rate you use.

-

Can I use the 4% rule for FIRE in India?

Not safely, especially if you are retiring at 40. The 4% rule was designed for 30-year retirements in the United States, where inflation averages 3%. In India, with 6 to 7% inflation and a 45-year retirement horizon, a 2.5 to 3% withdrawal rate is more appropriate. This means a higher corpus target, but it is the honest number.

-

Which investment instruments are best for FIRE at 40 in India?

Equity mutual funds (via Step-Up SIP) are the primary growth engine. PPF provides a tax-free, risk-free debt anchor. ELSS gives you equity exposure with 80C benefits. NPS adds further tax-efficient retirement savings. In the withdrawal phase, the three-bucket strategy — liquid funds, balanced funds, and equity funds — helps manage sequence-of-returns risk across a long retirement.

-

How do I handle taxes after I retire at 40 in India?

Your primary income source will be redemptions from mutual funds. LTCG on equity above ₹1.25 lakh per year is taxed at 12.5%. Structure your withdrawals to maximise the ₹1.25 lakh exemption each year. Use debt fund withdrawals for additional cash needs to spread the tax impact. Your total taxable income in early retirement may also fall below the basic exemption limit (₹3 lakh under the new regime), making your tax burden very low.

-

Is FIRE at 40 realistic on an average Indian salary?

It depends on your savings rate, career trajectory, and lifestyle. On a ₹1.5 lakh monthly salary with a 50% savings rate, hitting a ₹7 crore corpus in 14 years at 12% returns is achievable — but leaves very little room for large expenses (weddings, property, children's education). Most people who achieve FIRE at 40 either have high incomes, extremely lean lifestyles, or both. Starting early and maintaining a consistent step-up SIP makes a dramatic difference.

-

What happens if the stock market crashes right before I retire?

This is called sequence-of-returns risk — it is the biggest threat to early retirement. The solution is to start shifting 2 to 3 years of living expenses into liquid and debt funds starting 3 to 5 years before your target retirement date. That way, a market crash does not force you to sell equity at the worst time. Your equity portfolio gets time to recover while you live off the safer buckets.

Take the First Step Today

Retiring at 40 starts with knowing your number. Once you know your FIRE corpus target, everything else — your savings rate, investment instruments, and tax strategy — follows from it.

Use CalcPhi's free Goal-Based SIP Calculator to calculate exactly how much you need to invest each month to reach your FIRE corpus. Enter your target amount, time horizon, and expected return — the calculator does the rest in seconds, no sign-up required.

From there, model your step-up SIP using CalcPhi's Step-Up SIP Calculator to see the compounding impact of increasing your SIP by 10 to 15 percent each year as your income grows. The difference between a flat SIP and a step-up SIP over 14 years can easily amount to 2 to 3 crore rupees — which is the difference between a comfortable FIRE and a stressful one.

Calculate your FIRE number and SIP plan:

Goal-Based SIP Calculator → Step-Up SIP Calculator → ELSS Calculator → Inflation-Adjusted Returns →Disclaimer:The calculators and content on CalcPhi are for educational and estimation purposes only. The figures in this article are illustrative and based on assumed rates of return and inflation. Past market performance does not guarantee future results. Nothing in this article constitutes personalised financial advice. Please consult a SEBI-registered financial advisor or a Certified Financial Planner before making significant investment decisions.