FD vs Debt Mutual Fund: Where to Park Your Short-Term Money in 2026?

Until 2023, this question was easy to answer for anyone in the higher tax brackets — debt funds won, almost every time, because of their LTCG benefit and indexation advantage. Then the Finance Act 2023 changed the rules completely. Today, debt funds are taxed the same way FDs are — at your income slab rate, regardless of how long you hold them. So has the FD vs debt fund debate been settled? Not quite. The right answer in 2026 depends on your tax bracket, your timeline, your need for certainty, and a few nuances most investors still overlook.

What the 2023 Tax Change Actually Did

Before April 1, 2023, debt mutual funds held for more than 36 months qualified for Long-Term Capital Gains (LTCG) tax at 20% with indexation. Indexation adjusts your purchase price for inflation, which drastically reduces taxable gains. For someone in the 30% tax bracket, this was a massive advantage. An FD earning 7% would effectively earn around 4.9% post-tax. A debt fund with the same 7% return, after indexation, could leave you with 6%–6.5% post-tax.

After April 1, 2023, all that changed. Debt fund gains — whether you hold for 1 month or 10 years — are now added to your total income and taxed at your applicable slab rate. No LTCG. No indexation. The playing field between FDs and debt funds is now much closer. But "much closer" is not the same as "identical."

Head-to-Head: FD vs Debt Mutual Fund in 2026

| Feature | Bank FD | Debt Mutual Fund |

|---|---|---|

| Typical return (1–3 years) | 6.5%–7.5% p.a. | 6.5%–8.0% p.a. |

| Tax on gains | Slab rate (same as income) | Slab rate (same as income) |

| TDS | 10% if interest >₹40,000/year | No TDS at source |

| Liquidity | Penalty on premature withdrawal | Exit load (often nil after 7–30 days) |

| Capital safety | DICGC-insured up to ₹5 lakh | Market-linked (low, not zero risk) |

| Tax timing | Interest accrues and is taxed annually | Tax only at redemption |

| Compounding | Quarterly (most banks) | Daily NAV (continuous) |

| Inflation sensitivity | Fixed rate — locked at booking | Can benefit from rate-cut cycles |

The Hidden Advantage Debt Funds Still Have: Tax Timing

This is the one advantage that survived the 2023 tax change, and most people still underestimate it. When you hold a cumulative FD, the interest accrues every year — and the Income Tax Act requires you to pay tax on that interest annually, even though you don't receive the cash until maturity. This is accrual-based taxation.

With a debt mutual fund, you pay tax only when you redeem. The entire corpus grows untouched by tax until the day you sell. This deferral can be surprisingly powerful.

Real-money example: ₹10 lakh invested for 3 years at 7.5%, 30% tax bracket.

- FD (cumulative): Tax paid in Years 1, 2, and 3. Effective post-tax maturity — ₹12.03 lakh

- Debt fund (same return): Tax paid only at redemption. Effective post-tax maturity — ₹12.21 lakh

The difference: approximately ₹18,000 simply from deferring tax to Year 3. This number grows significantly for larger amounts and longer durations.

The FD Advantage: Certainty, Insurance, and Zero Effort

Debt funds are not for everyone, and there are genuinely good reasons to prefer FDs.

Predictability is priceless for specific goals. If you're saving ₹8 lakh for a wedding in 18 months, you need to know exactly how much you'll have. A bank FD locks in the rate on the day you book — you'll know your maturity amount to the rupee. A debt fund's return is not guaranteed. A sudden spike in interest rates can cause bond prices to fall, which means your debt fund NAV could dip. It recovers over time, but "over time" is not reassuring when you have a fixed deadline.

DICGC insurance matters below ₹5 lakh. Bank deposits are insured by DICGC up to ₹5 lakh per depositor per bank. If your short-term corpus is under ₹5 lakh and it represents money you truly cannot afford to lose even 1%, the FD gives you government-backed safety that no mutual fund can match.

Simplicity wins for first-time investors. Opening an FD requires nothing more than a bank account. Debt mutual funds require a KYC-compliant account, understanding of fund categories, and at least some awareness of duration risk. If you're parking money for a few months and don't want to think about it, an FD is perfectly rational.

Which Debt Fund Category Matches Your Timeline?

Not all debt funds behave the same way. Matching the fund category to your investment horizon is critical.

- Overnight and Liquid Funds (1 day–3 months): Returns around 6.5%–7.2%, virtually no interest rate sensitivity. Right choice for an emergency fund or money you might need within the quarter.

- Low-Duration and Money Market Funds (3–12 months): Portfolio maturity of 6–12 months. Returns around 7%–7.5%, very low NAV volatility. Well-suited for a 6-to-12-month parking requirement.

- Short-Duration Funds (1–3 years): The direct FD competitor for the 1–3 year horizon. Returns can be 7.5%–8%, with moderate interest rate risk. If the RBI cuts rates, bond prices rise and these funds can deliver returns above locked-in FD rates.

- Corporate Bond and Banking & PSU Funds (2–4 years): Higher potential returns (7.5%–8.5%) but include credit risk. Stick to funds with AAA-rated portfolios to keep default risk minimal.

The SWP Strategy: Where Debt Funds Pull Far Ahead

Here is a scenario where debt funds are clearly superior to FDs: when you want regular monthly income from a lump sum.

If you put ₹25 lakh in a bank FD and opt for monthly interest payouts, the bank pays you interest and deducts TDS. Every rupee of interest is added to your taxable income that year. If you're in the 30% bracket, you keep only 70 paise of every rupee earned.

With a debt mutual fund, you can set up a Systematic Withdrawal Plan (SWP) — withdrawing a fixed amount every month. Each withdrawal is partly return of principal and partly gain. Only the gain portion is taxed, not the entire withdrawal. This makes SWPs dramatically more tax-efficient than FD interest payouts for anyone in the 20% or 30% bracket. For retirees or anyone living off accumulated savings, this distinction can mean lakhs saved in tax over a decade.

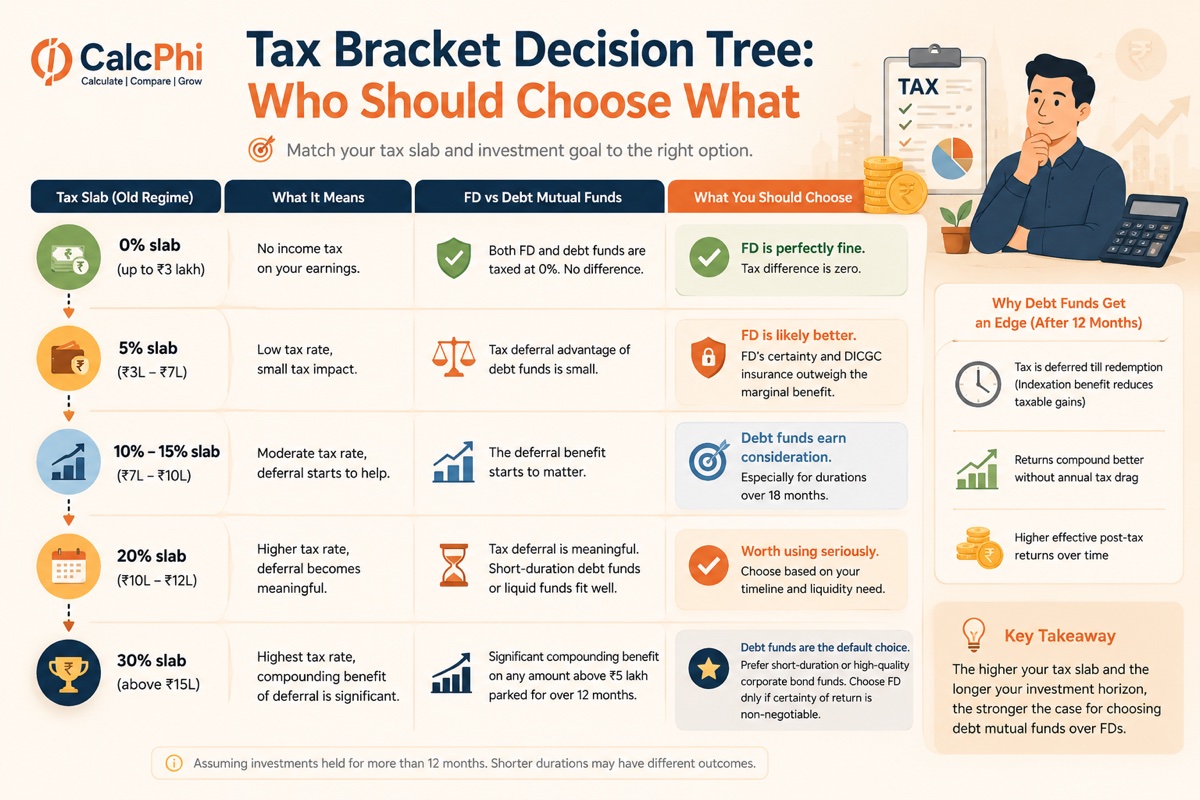

Tax Bracket Decision Tree: Who Should Choose What

- 0% slab (up to ₹3 lakh): FD is perfectly fine. Tax difference is zero.

- 5% slab (₹3L–₹7L): Tax deferral advantage of debt funds is small. FD's certainty and DICGC insurance likely outweigh the marginal benefit.

- 10%–15% slab (₹7L–₹10L): The deferral benefit starts to matter. For durations over 18 months, debt funds earn consideration.

- 20% slab (₹10L–₹12L): Tax deferral is meaningful. Short-duration debt funds or liquid funds depending on your timeline are worth using seriously.

- 30% slab (above ₹15L): The compounding benefit of deferred tax is significant on any amount above ₹5 lakh parked for over 12 months. Debt funds — particularly short-duration or corporate bond funds with high credit quality — are the default choice, unless certainty of return is non-negotiable.

What About the RBI Rate Cycle?

When rates fall, existing bonds in a debt fund portfolio become more valuable — this pushes NAV up, giving debt fund investors a capital appreciation bonus that FD holders completely miss. If the RBI continues its rate-cutting cycle into 2026, short-duration and medium-duration debt fund investors could earn 8%–9% annualised returns — noticeably above the 7%–7.5% FD rates available today.

The flip side: if rates rise unexpectedly, debt fund NAVs can fall in the short term. For money you need within 6 months, this risk is real. For money you can leave for 18–36 months, the mean-reversion of bond prices makes this manageable.

The Liquid Fund Case for Your Emergency Corpus

Most Indians keep their 3–6 month emergency corpus in a savings account earning 3%–4%. A better option — if you're comfortable with the basics of mutual funds — is a liquid fund. Liquid funds invest in instruments maturing within 91 days (government T-bills, commercial paper, bank certificates of deposit). Returns are typically 6.5%–7.2%, they have no exit load after 7 days, and redemptions usually reach your bank account within the same business day.

For a ₹3 lakh emergency fund, even a 3% return improvement means ₹9,000 extra per year — for zero additional work.

Calculate your exact FD maturity value and TDS impact:

FD Calculator →Frequently Asked Questions

-

After the 2023 tax change, is there still any benefit of debt funds over FDs?

Yes — the tax deferral benefit remains. With an FD, interest is taxed every year as it accrues, even if you don't receive it. With a debt fund, you pay tax only when you redeem. For anyone in the 20% or 30% bracket parking money for 2–3 years, this deferral can make a material difference — typically ₹15,000–₹30,000 on every ₹10 lakh depending on the rate and tenure.

-

Can I lose money in a debt mutual fund?

It is uncommon but possible in two scenarios. First, a credit event — when a bond issuer in the portfolio defaults. This mostly affects credit risk funds; liquid and overnight funds carry negligible credit risk. Second, a sharp interest rate spike — which causes existing bond prices to fall. Choosing high-credit-quality, short-duration funds minimises both risks significantly.

-

What is TDS on FD and can I avoid it?

TDS is the bank's obligation to deduct 10% tax on your FD interest if it exceeds ₹40,000 in a financial year (₹50,000 for senior citizens). If your total annual income is below the basic exemption limit, you can submit Form 15G (for those under 60) or Form 15H (for senior citizens) to your bank at the start of the year to stop TDS deduction. Note that TDS is not the final tax — if your slab is 30%, you'll owe the remaining 20% at filing.

-

What is the best debt fund type for 1–2 years?

For a 1–2 year horizon, low-duration funds and money market funds are generally the right fit. They target portfolio maturities of 6–12 months, which minimises NAV sensitivity to interest rate changes while still offering better yields than liquid funds. Short-duration funds work well too but carry slightly more interest rate risk.

-

Is FD interest fully taxable in India?

Yes. Every rupee of FD interest is added to your total income and taxed at your applicable income slab rate. There is no exemption for FD interest under the new tax regime, except for the ₹50,000 deduction available to senior citizens under Section 80TTB under the old regime.

-

What if I need the money back early — FD or debt fund?

Breaking an FD before maturity typically costs 0.5%–1% as a penalty. Debt mutual funds (except ELSS or close-ended funds) can be redeemed anytime. Liquid and overnight funds have no exit load at all. Short-duration and most other categories charge 0.25%–1% only for the first 7–30 days. After that window, debt funds are generally more liquid and penalty-free than FDs.

Disclaimer: The information in this article is for educational and estimation purposes only. All figures are illustrative and based on publicly available data as of May 2026. Nothing in this article constitutes financial advice. Mutual fund investments are subject to market risks. Fixed deposit returns depend on the bank and prevailing rates at the time of booking. Please consult a SEBI-registered investment advisor or qualified financial planner for advice tailored to your personal situation.