Expense Ratio Explained: How Fund Charges Silently Eat Your Mutual Fund Returns

You invest ₹10 lakh in a mutual fund, wait patiently for 20 years, and expect a handsome corpus in return. But when you finally check your statement, something feels off — the number is lower than what you calculated. No one stole your money. No market crash wiped it out. The quiet culprit is the expense ratio, a small percentage that gets deducted from your fund's value every single year, without you ever writing a cheque or seeing a deduction notice. Most investors in India know the expense ratio exists. Very few understand how deeply it can shrink their final wealth over time.

What Is an Expense Ratio in a Mutual Fund?

The expense ratio is the annual fee that a mutual fund charges to manage your investment. It covers everything the fund house spends to run the scheme — the fund manager's salary, administrative costs, marketing expenses, distributor commissions (in regular plans), registrar fees, and more. This total cost, expressed as a percentage of the fund's average daily net assets, is called the Total Expense Ratio (TER).

You never see this fee being deducted from your bank account. Instead, it is silently subtracted from the fund's Net Asset Value (NAV) every single day on a pro-rata basis. If a fund's gross return is 12% but its expense ratio is 1.5%, your net return is only 10.5%. That gap — year after year, compounding — is where the real damage happens. Think of it like a treadmill that is always tilted slightly against you: you are still running (investing), but you are working harder than you realise just to make up for the slope.

How SEBI Regulates Expense Ratios in India

SEBI has set strict caps on how much a mutual fund can charge as its expense ratio. These limits depend on the fund's size (AUM) and whether it is an equity or debt fund.

| AUM Slab | Equity Funds Max TER | Debt Funds Max TER |

|---|---|---|

| First ₹500 crore | 2.25% | 2.00% |

| ₹500–₹750 crore | 2.00% | 1.75% |

| ₹750–₹2,000 crore | 1.75% | 1.50% |

| ₹2,000–₹5,000 crore | 1.60% | 1.35% |

| Above ₹50,000 crore | 1.05% | 0.80% |

Index funds and ETFs, which are passively managed and require no active stock-picking, are capped at 1% but in practice charge as little as 0.05% to 0.20%. Just because a fund is within the legal limit does not mean its expense ratio is acceptable for your portfolio.

Direct Plans vs Regular Plans: The Expense Ratio Gap You Cannot Ignore

When you invest through a distributor, broker, or financial advisor, you are usually buying the regular plan. The fund pays a trail commission to that distributor out of the fund's expense ratio, which means regular plans cost you 0.5% to 1.5% more per year than the identical direct plan of the same fund. In a direct plan, there is no intermediary, so the charge is lower and more of your money stays invested.

On a ₹10 lakh investment over 20 years at 12% gross returns, the difference between a regular plan with 1.5% TER and a direct plan with 0.5% TER can add up to over ₹15 to ₹20 lakh in lost wealth. That is not a rounding error — that is a car, a renovation, or years of retirement income simply handed over in fees.

The Real Cost of Expense Ratio: A Number-by-Number Breakdown

Consider two investors — Arjun and Meera — who both invest ₹10 lakh as a one-time lumpsum in equity mutual funds with the same gross return of 12% per year. Arjun picks a regular plan with a 1.5% expense ratio. Meera goes with a direct index fund at 0.2%.

| Investor | TER | Net Return | Corpus After 20 Years |

|---|---|---|---|

| Arjun (regular active fund) | 1.5% | 10.5% | ₹71.8 lakh |

| Meera (direct index fund) | 0.2% | 11.8% | ₹90.4 lakh |

That 1.3% difference in annual charges has cost Arjun nearly ₹18.6 lakh over 20 years — almost twice the original investment in lost wealth. And this is before accounting for the compounding drag on SIP investments, where the effect runs across every instalment over the entire tenure.

Active Funds vs Index Funds: Is the Higher Expense Ratio Worth It?

Actively managed funds charge more — sometimes 10 to 20 times more than an index fund — because they employ professional fund managers to research stocks, time entries and exits, and (theoretically) outperform the benchmark. Index funds simply replicate the Nifty 50 or Sensex, requiring minimal management and charging very little.

The data, both globally and increasingly within India, shows that the majority of actively managed equity funds do not consistently beat their benchmark after expenses. The expense ratio is the primary reason. A fund manager may generate 13% gross returns, but after a 1.8% TER, you receive only 11.2% — which may not be significantly better than an index fund earning 11.8% net.

This does not mean active funds are always bad. In small-cap, mid-cap, or flexi-cap categories, skilled fund managers have historically added genuine alpha. But in large-cap equity — heavily researched and liquid — consistently beating the index after fees is extremely difficult. The higher the expense ratio, the higher the bar the fund manager must clear just to match an index fund's net return.

How to Find the Expense Ratio of Any Mutual Fund in India

Every mutual fund in India is required by SEBI to disclose its TER transparently. The simplest method is to visit the AMFI website (amfiindia.com), where all funds publish their monthly TER disclosures. You can also find the expense ratio on the fund's own fact sheet, published monthly on the fund house's website. Most platforms — Zerodha Coin, Groww, MF Central, Kuvera — display the expense ratio on each fund's detail page.

Always look at the TER of the specific plan (direct or regular) you are investing in, as the two figures are meaningfully different. Check whether the ratio disclosed is the current one — fund houses do revise expense ratios periodically as their AUM grows.

Expense Ratio by Fund Category: What Is Low, Fair, or High?

Equity index funds and ETFs typically charge between 0.05% and 0.20% for direct plans. Anything above 0.30% in this category is high, given that there is no active management involved.

Large-cap active funds in direct plans generally range from 0.80% to 1.25%. A well-run large-cap direct fund at under 1% is reasonably priced, especially if it has a strong long-term record of alpha generation.

Mid-cap and small-cap active funds can justify slightly higher charges — typically 1.0% to 1.5% in direct plans — because researching smaller companies requires more resources and the alpha opportunity is genuinely higher.

Debt funds and liquid funds should have low expense ratios since returns in this category are already modest. A debt fund charging above 0.50% in a direct plan deserves scrutiny.

ELSS funds, which offer Section 80C deductions of up to ₹1.5 lakh per year, often charge between 1.0% and 1.5% in direct plans. Use CalcPhi's ELSS Calculator to evaluate whether the tax savings make the higher expense ratio worth it for your income bracket.

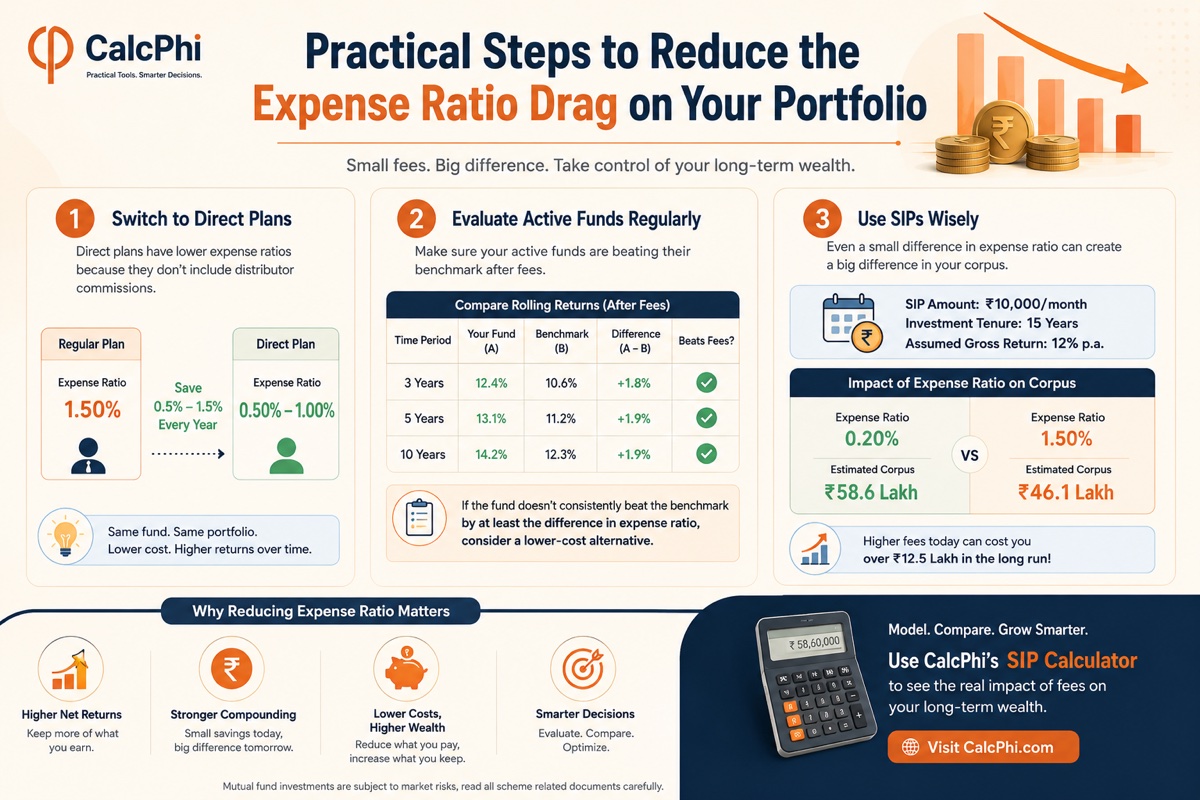

Practical Steps to Reduce the Expense Ratio Drag on Your Portfolio

The first and most impactful step is to switch from regular plans to direct plans wherever possible. This single change can reduce your annual expense ratio by 0.5% to 1.5% depending on the fund, with no change in the underlying portfolio.

The second step is to evaluate whether your active funds are actually delivering returns above their benchmark after fees. Pull up the fund's rolling returns over 3, 5, and 10 years and compare them to the Nifty 50 TRI (Total Return Index) or the relevant category index. If the fund has not consistently beaten its benchmark by at least the difference in expense ratio, it may be worth considering a switch to a lower-cost option.

The third step is to use SIP investments wisely. A ₹10,000 monthly SIP over 15 years can result in a meaningfully different corpus depending on whether your fund charges 0.2% or 1.5%. See the impact in real time using CalcPhi's SIP Calculator, which lets you model different net return assumptions based on your fund's expense ratio.

A Common Misconception: Expense Ratio Is Not the Same as Exit Load

Many first-time investors confuse expense ratio with exit load. They are two different charges. The expense ratio is an ongoing annual fee embedded in the NAV — it applies every day you hold the fund. Exit load is a one-time penalty charged when you redeem your units before a specified holding period, typically one year for equity funds.

Most equity funds charge a 1% exit load if you sell within 12 months. After that, redemption is generally free. The expense ratio, however, continues regardless of how long you hold. Both charges reduce your returns, but the expense ratio has a far larger cumulative impact over the long run because it compounds year after year.

See exactly how much your fund's expense ratio is costing you:

Expense Ratio Calculator → Direct vs Regular Calculator →Frequently Asked Questions

-

What is a good expense ratio for a mutual fund in India?

For index funds and ETFs, a good expense ratio is anything under 0.20% in a direct plan. For actively managed equity funds, a direct plan charging under 1% is considered competitive. Regular plans will always be higher due to distributor commissions, so comparing direct plan TERs is the more meaningful benchmark when evaluating funds.

-

Does a lower expense ratio always mean a better fund?

Not necessarily. A fund with a lower expense ratio is not automatically superior — the fund must also deliver consistent returns and manage risk well. However, all else being equal, a lower expense ratio means more of the fund's gross return flows to you. It is always a positive factor, but it should not be the only factor in your fund selection decision.

-

How is the expense ratio deducted from my investment?

The expense ratio is never deducted as a visible line item from your account. Instead, it is accounted for daily in the fund's NAV calculation. The fund's assets are reduced by the pro-rata daily expense amount before the NAV is published. So if a fund's gross NAV would have been ₹100.10 on a given day, and the daily expense equivalent reduces it by ₹0.03, the published NAV is ₹100.07. You never see the deduction — it simply results in a slightly lower NAV each day.

-

Can the expense ratio change after I invest?

Yes, mutual fund houses can and do revise their expense ratios from time to time, subject to SEBI's maximum limits. As a fund's AUM grows, SEBI's slab structure requires the TER to reduce. Conversely, funds can also increase their TER up to the regulatory cap if AUM falls. SEBI mandates that fund houses notify investors before any upward revision in expense ratio.

-

Is the expense ratio tax deductible?

No, the expense ratio is not separately tax deductible in India. Since it is already embedded in the NAV and reduces your effective return, it indirectly reduces the capital gains you make on the investment — but there is no separate tax benefit or deduction available for the expense ratio itself.

-

What is the difference between expense ratio in direct vs regular plans of the same fund?

The only structural difference between a direct and regular plan of the same mutual fund is the expense ratio. The portfolio, fund manager, and investment strategy are identical. The regular plan includes a distributor commission (trail commission) in its TER, making it more expensive by 0.5% to 1.5% annually. The direct plan has no distributor commission, resulting in a lower TER and better long-term returns for the investor.

Disclaimer: All CalcPhi calculators and articles are for educational and estimation purposes only. Expense ratios, returns, and tax rules are subject to change. Nothing in this article constitutes financial or investment advice. Please consult a SEBI-registered investment advisor or qualified financial planner before making investment decisions.