ESOPs in India: How to Calculate Your Real Gains and Minimise Tax (2026 Guide)

Getting ESOPs — Employee Stock Option Plans — as part of your salary package feels like winning the jackpot. And it can be, if you understand how they work. The problem is that most employees only look at the paper value of their options without ever accounting for the tax that eats into those gains at two separate stages. Miss either stage, and you could end up with a far smaller payout than you expected — or worse, a surprise tax bill with no cash to pay it. This guide breaks down exactly how ESOP gains are calculated in India, what you owe at each stage, and the legal strategies you can use to keep more of what you earn. All figures reflect the rules under the Income-tax Act, 2025, which took effect from Tax Year 2026-27 (1 April 2026).

What Is an ESOP and How Does the Lifecycle Work?

An ESOP gives you the right — not the obligation — to buy shares in your company at a fixed price, called the exercise price or strike price, at a future date. The price is usually set below the market value at the time of the grant, which is what makes ESOPs valuable.

Grant date: The company awards you a certain number of options. No tax is due here. You do not own shares yet — just the right to buy them later.

Vesting period: Options typically vest over three to four years. A common schedule is 25% per year. No tax is triggered at vesting.

Exercise date: You convert your vested options into actual shares by paying the exercise price. This is the first tax event.

Sale date: You sell the shares in the open market or in a secondary transaction. This is the second tax event.

Understanding this lifecycle is crucial because India taxes ESOPs twice — once at exercise and once at sale. Missing either event in your tax planning is one of the most expensive mistakes salaried employees make.

Stage 1: Tax at Exercise — The Perquisite

When you exercise your options, the government treats the discount you received as a salary benefit, or "perquisite." In plain terms, if your company's share is worth ₹500 in the market and you buy it for ₹50, you have effectively received ₹450 per share as compensation. That ₹450 is taxable salary income.

The formula is straightforward:

Perquisite Value = (Fair Market Value on exercise date − Exercise Price) × Number of shares exercised

For listed companies, the FMV is the stock price on the exchange on the date of exercise. For unlisted companies — including most startups — the FMV must be certified by a SEBI-registered Category I Merchant Banker. This valuation is done using methods like the Discounted Cash Flow (DCF) approach and must reflect the actual economic value of the share.

The total perquisite value is added to your salary income for the year and taxed at your applicable slab rate. If you are in the 30% bracket, you pay 30% (plus surcharge and 4% cess) on the entire perquisite amount. Your employer is required to deduct TDS on this amount under Section 192 and report it in your Form 16. The key point: this tax is due even if you have not sold a single share. Use CalcPhi's free Income Tax Calculator to estimate how much income tax you would owe after adding the ESOP perquisite to your salary — it supports both old and new regime calculations for AY 2026-27.

Stage 2: Tax at Sale — Capital Gains

When you eventually sell the shares, you pay capital gains tax on the profit made between the time you exercised and the time you sold. Crucially, your cost of acquisition is not the exercise price you paid — it is the FMV on the date of exercise. This is because you already paid tax (in Stage 1) on the gain up to FMV. You only owe tax on gains above that.

Capital Gain = Sale Price − FMV at Exercise

Tax Rates for Listed ESOP Shares (Companies on NSE/BSE)

If you hold listed shares for 12 months or less after exercise, the gain is a Short-Term Capital Gain (STCG), taxed at 20% (applicable where Securities Transaction Tax is paid). If you hold listed shares for more than 12 months, the gain is a Long-Term Capital Gain (LTCG), taxed at 12.5%. The first ₹1.25 lakh of LTCG from listed equity in a financial year is exempt from tax under the current rules.

Tax Rates for Unlisted ESOP Shares (Startups and Private Companies)

For unlisted shares, the holding period bar for long-term treatment is higher. You need to hold shares for more than 24 months to qualify for LTCG at 12.5% (no indexation benefit). If you sell within 24 months, the gain is classified as STCG and taxed at your income tax slab rate — which can be as high as 30% plus cess. This distinction matters enormously: a startup employee who sells two weeks before the 24-month mark pays slab rate tax; one who waits just a little longer pays 12.5%.

Use CalcPhi's Capital Gains Tax Calculator to estimate your capital gains tax from an ESOP sale — it handles both STCG and LTCG scenarios for listed and unlisted equity.

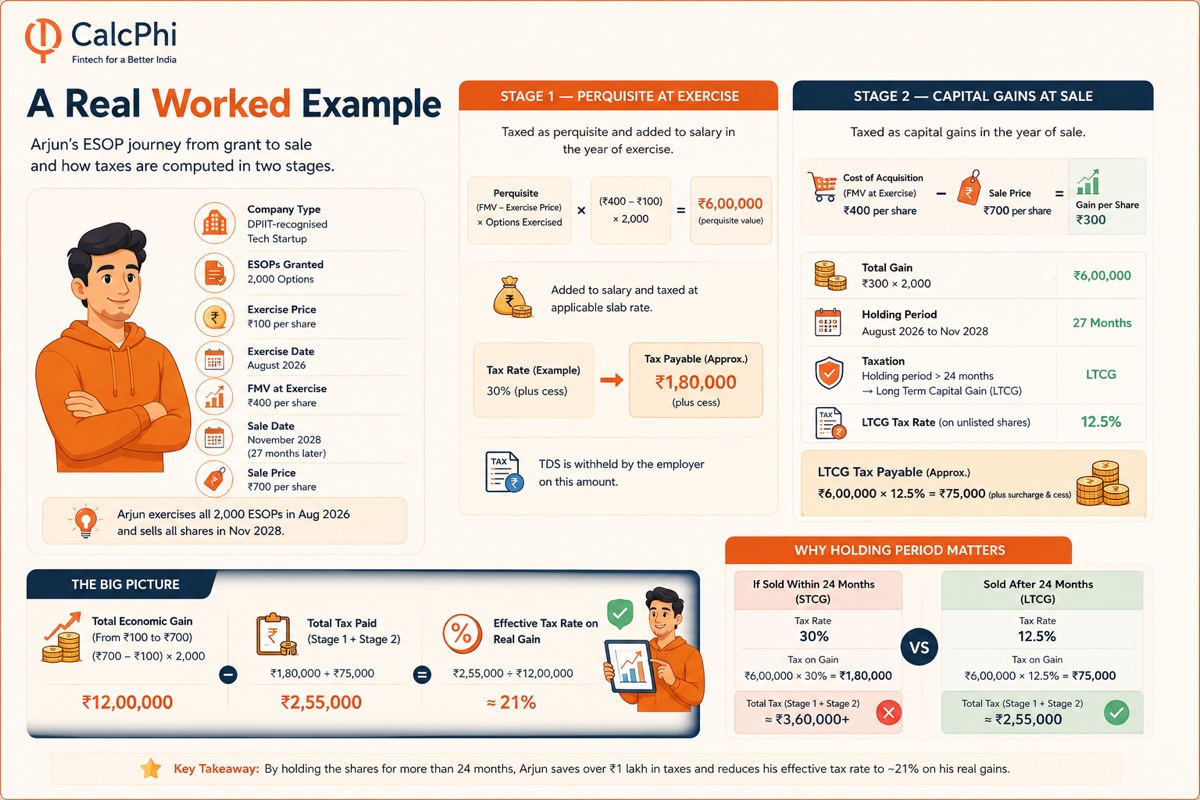

A Real Worked Example

Arjun works at a DPIIT-recognised tech startup. He was granted 2,000 ESOPs with an exercise price of ₹100 per share. He exercises all of them in August 2026, when the merchant banker FMV is ₹400 per share. He then sells all shares in November 2028 — 27 months later — at ₹700 per share.

Stage 1 — Perquisite at exercise:

Perquisite = (₹400 − ₹100) × 2,000 = ₹6,00,000

This ₹6 lakh is added to Arjun's salary and taxed at his applicable slab rate. In the 30% bracket, he owes approximately ₹1,80,000 in tax (plus cess), withheld by his employer as TDS.

Stage 2 — Capital gains at sale:

Cost of acquisition = FMV at exercise = ₹400 per share

Gain per share = ₹700 − ₹400 = ₹300

Total gain = ₹300 × 2,000 = ₹6,00,000

Holding period = 27 months (exceeds 24 months — LTCG for unlisted shares)

LTCG tax = ₹6,00,000 × 12.5% = ₹75,000 (plus surcharge and cess)

On a total economic gain of ₹12,00,000 (₹700 − ₹100 × 2,000), Arjun pays roughly ₹2.55 lakh in total taxes — about 21% effective tax on his real gains. This is considerably better than the outcome if he had sold within 24 months, when the Stage 2 gain would have been taxed at 30%, pushing his total tax bill above ₹3.6 lakh.

The Startup Deferral — A Key Relief for ESOP Holders

Employees of eligible startups face a specific problem: they receive a large tax bill at exercise on shares they cannot easily sell because there is no active market. To address this, the government introduced a tax deferral provision for employees of DPIIT-recognised startups that also hold a Section 80-IAC certificate.

Under the Income-tax Act, 2025, perquisite tax on ESOPs in eligible startups can be deferred until the earliest of three events: 60 months from the end of the tax year in which the shares were allotted (for shares allotted on or after 1 April 2026), the date the employee sells or transfers the shares, or the date the employee ceases employment with that startup.

This means employees at qualifying startups do not have to pay tax at exercise if they plan to hold. They report the perquisite in their ITR but defer the actual payment — removing the painful cash-flow crunch of paying tax on illiquid paper. It is important to note that this deferral does not reduce the tax — it only delays it. And it only applies to startups that meet both the DPIIT recognition criteria and the Section 80-IAC certification. Not every startup qualifies, so always verify your company's eligibility before assuming this benefit applies to you.

Practical Strategies to Minimise Your ESOP Tax

Exercise early, when FMV is low. The perquisite tax is calculated at the time of exercise. If you exercise options when your company's FMV is still relatively modest — earlier in the company's growth curve — the perquisite amount is smaller, and your Stage 1 tax bill is lower. This is a powerful lever for startup employees who have discretion over timing.

Wait for the long-term threshold before selling. For listed shares, waiting beyond 12 months from the exercise date slashes the capital gains rate from 20% to 12.5%. For unlisted shares, the same logic applies at the 24-month mark. On a gain of ₹10 lakh, that difference is ₹75,000 saved — just by waiting.

Spread large sales across financial years. If you hold listed shares and plan to sell a large position, spreading sales across two financial years lets you use the ₹1.25 lakh LTCG exemption twice. This can result in a saving of up to ₹15,625 per financial year at the 12.5% LTCG rate.

Offset capital gains with capital losses. If you have losses from other investments in the same financial year, you can set them off against your ESOP capital gains before calculating the tax. Short-term capital losses can be set off against both STCG and LTCG. Keep this in mind when reviewing your broader portfolio alongside your ESOP position.

Use the new vs old tax regime comparison for Stage 1. Since the perquisite is added to your salary, switching between the old and new tax regimes can sometimes reduce your overall tax burden in the year of exercise — especially if you have deductions under Section 80C, 80D, or HRA. Use CalcPhi's New vs Old Tax Regime Calculator to compare both options and see which regime saves you more in the year you plan to exercise.

Plan your advance tax. If you sell ESOP shares mid-year and make a capital gain, you are required to pay advance tax in instalments. Failing to do so leads to interest penalties. Use CalcPhi's Advance Tax Calculator to estimate your quarterly instalments and stay compliant throughout the year.

How to Report ESOPs in Your Income Tax Return

The perquisite at exercise should already appear in your Form 16 under "Salary Perquisites," along with the TDS withheld. You report this in your ITR under the salary income head. Use ITR-2 or ITR-3 — not ITR-1, which does not support capital gains or perquisite reporting.

For capital gains at sale, report under the Capital Gains schedule. Your cost of acquisition is the FMV at exercise — not the exercise price. Enter the allotment date, sale date, FMV at exercise, and sale consideration. The ITR utility will compute the tax automatically. If your company's shares are foreign-listed, you additionally need to declare them under Schedule FA (Foreign Assets) and may need to file Form 67 if foreign taxes were paid.

If you are a startup employee using the deferral provision, the perquisite may not appear in Form 16 in the year of allotment. You still need to disclose it in your return for that year. Keep all documentation — the grant letter, merchant banker FMV certificate, exercise confirmation, and sale contract — since these may be requested during scrutiny.

Frequently Asked Questions

When exactly is ESOP tax triggered — at grant, vesting, exercise, or sale?

ESOPs are not taxed at grant or vesting. The first tax event is at exercise, when the perquisite (FMV minus exercise price) is treated as salary income. The second tax event is at sale, when capital gains tax applies on profits above the FMV at exercise. Many employees mistakenly assume tax applies only when they sell shares, which leads to unexpected bills at exercise time.

What is FMV for ESOP purposes, and who determines it?

For listed company shares, FMV is the stock exchange price on the exercise date. For unlisted company shares, FMV must be certified by a SEBI-registered Category I Merchant Banker. The merchant banker typically uses the Discounted Cash Flow (DCF) or Net Asset Value method. The FMV certified at exercise becomes your cost of acquisition for computing capital gains at the time of sale.

Can I defer ESOP perquisite tax if I work at a startup?

Yes, but only if your startup is DPIIT-recognised and also holds a Section 80-IAC certificate. If both conditions are met, the perquisite tax can be deferred until the earliest of: 60 months from the tax year of allotment (for shares allotted from 1 April 2026), the date of sale, or the date you leave the company. This deferral helps with cash flow but does not reduce the actual tax owed.

What is the difference in capital gains tax for listed vs unlisted ESOP shares?

For listed shares, the holding period for LTCG is 12 months; LTCG is taxed at 12.5% and STCG at 20%. For unlisted shares, the holding period is 24 months; LTCG is taxed at 12.5% (without indexation) and STCG is taxed at your income slab rate. Because unlisted STCG is taxed at slab rates that can reach 30%, the 24-month holding threshold is especially important for startup employees.

My employer deducted TDS at exercise — do I still need to pay advance tax?

The TDS your employer deducts covers the perquisite portion. But if you also sell shares and make a capital gain during the same year, that gain is separate from salary and not covered by the employer's TDS. You will need to pay advance tax on that capital gain if the total tax liability (after TDS credit) exceeds ₹10,000 for the year. Missing advance tax instalments leads to interest under Sections 234B and 234C.

Can I carry forward ESOP capital losses if I sell at a loss?

Yes. If you sell ESOP shares at a loss, you can carry the capital loss forward for up to eight assessment years. Short-term capital losses can be set off against both STCG and LTCG, while long-term capital losses can only be set off against LTCG. This makes ESOP loss planning a useful tool if you have gains from other equity investments in the same or future years.

Disclaimer: The information in this article is for educational and estimation purposes only. Tax laws are complex and subject to change; specific provisions under the Income-tax Act, 2025 should be verified against the gazetted text. Nothing in this article constitutes personalised financial or tax advice. Please consult a qualified Chartered Accountant or tax advisor for guidance specific to your situation.