ELSS vs PPF: Which Is Better for 80C Tax Saving in 2026?

Every year in March, millions of Indian salaried employees scramble to invest ₹1.5 lakh before the financial year closes — not because they planned to, but because their HR department sent a final investment proof reminder. Two names come up every single time: ELSS and PPF. Both qualify under Section 80C of the Income Tax Act. Both save you the same ₹46,800 in tax (for someone in the 30% bracket). Yet they are fundamentally different instruments, built for different types of investors, with vastly different outcomes over time.

This article breaks down exactly how ELSS and PPF compare on every dimension that actually matters — returns, tax treatment, liquidity, lock-in, and suitability by age and income. By the end, you'll know not just which one "wins," but which one is right for you.

What Is Section 80C and Why Does It Matter?

Section 80C of the Income Tax Act allows individual taxpayers (and HUFs) to claim a deduction of up to ₹1.5 lakh per financial year from their taxable income. This deduction is available only if you choose the old tax regime — under the new regime (which is now the default for AY 2026-27), 80C deductions are not applicable.

So if you're on the old regime and earn ₹12 lakh a year, a full ₹1.5 lakh 80C investment reduces your taxable income to ₹10.5 lakh. Depending on your slab, this saves you anywhere from ₹15,600 (20% bracket) to ₹46,800 (30% bracket) in tax. The deduction itself is the same regardless of whether you use ELSS, PPF, EPF, LIC, or a 5-year FD — what differs enormously is what happens to your money after you invest it.

You can check exactly how much tax you save under the old regime using CalcPhi's Section 80C Calculator — it maps every eligible instrument and shows your net tax liability before and after claiming deductions.

ELSS: The Market-Linked Tax Saver

ELSS stands for Equity Linked Savings Scheme. It is a category of mutual fund that invests at least 80% of its portfolio in equities — stocks of Indian companies. Since SEBI classifies ELSS as a diversified equity fund, it carries full market risk. But it also comes with the shortest lock-in period of any 80C investment: just 3 years.

The returns are market-linked, which means there is no guaranteed number. Historically, diversified ELSS funds have delivered 12–15% CAGR over 10-year periods, though individual fund performance varies significantly. Past returns are never a guarantee of future results.

After the 3-year lock-in, all gains are classified as Long-Term Capital Gains (LTCG). From AY 2026-27, LTCG on equity is taxed at 12.5% on gains exceeding ₹1.25 lakh per year — a rule introduced in the Union Budget 2024. Below that threshold, your gains are tax-free. There is no upper limit on how much you can invest in ELSS, but only the first ₹1.5 lakh counts towards your 80C deduction.

Want to see how your ELSS investment grows year by year, including the impact of LTCG? Use CalcPhi's free ELSS Calculator to model different return scenarios and get your projected maturity value in seconds.

PPF: The Government-Backed Tax-Free Compounder

PPF stands for Public Provident Fund. It is a government savings scheme administered by the Ministry of Finance and available through any post office or authorised bank. The current interest rate for Q1 FY 2026-27 is 7.1% per annum, compounded annually. This rate is reviewed every quarter by the Ministry of Finance, though it has remained unchanged since April 2020.

PPF has a mandatory lock-in of 15 years, after which the account can be extended in 5-year blocks — either with or without continued contributions. The maximum you can invest is ₹1.5 lakh per year.

What makes PPF genuinely special is its EEE (Exempt-Exempt-Exempt) tax status. The investment qualifies for 80C deduction. The interest earned every year is completely tax-free. And the full maturity amount — principal plus 15 years of compounded interest — is also tax-free on withdrawal. No LTCG, no TDS, nothing. You take home every rupee.

NRIs are not eligible to open a new PPF account. Existing accounts opened before becoming an NRI can continue until maturity. To see exactly how much your PPF account will be worth after 15 years, try CalcPhi's PPF Calculator. It shows year-by-year interest accrual and the final maturity value based on the current 7.1% rate.

The Numbers: 15-Year Wealth Comparison

Let's run the actual numbers for someone investing ₹1.5 lakh every year for 15 years — the standard PPF tenure — so we're comparing on equal footing.

| PPF at 7.1% | ELSS at 12% CAGR | ELSS at 15% CAGR | |

|---|---|---|---|

| Total Invested | ₹22.5 lakh | ₹22.5 lakh | ₹22.5 lakh |

| Gross Maturity Value | ₹40.7 lakh | ₹63.8 lakh | ₹82.1 lakh |

| Tax on Gains | Nil | ~₹3–5 lakh (LTCG) | ~₹6–8 lakh (LTCG) |

| Approximate Net Value | ₹40.7 lakh | ₹59–61 lakh | ₹74–76 lakh |

| Gain Over PPF | — | ₹18–20 lakh more | ₹33–36 lakh more |

Even at a conservative 12% CAGR assumption — lower than the 15-year average of most large-cap ELSS funds — ELSS beats PPF by roughly ₹18–20 lakh after accounting for LTCG. At 15% CAGR, the gap is over ₹33 lakh. That is not a rounding error. That is the difference between two different retirement outcomes.

The key caveat: ELSS returns at 12% or 15% are assumptions, not guarantees. Markets can disappoint, especially over shorter windows.

The Tax Treatment Deep-Dive

The tax comparison between ELSS and PPF is more nuanced than it first appears. PPF gives you a 7.1% guaranteed, fully tax-free return. For a 30% bracket taxpayer, the pre-tax equivalent of a 7.1% tax-free return is approximately 10.1%. That means PPF is effectively competing with a taxable investment yielding 10.1% — not a bad benchmark at all.

ELSS, on the other hand, gives market-linked returns but applies LTCG at 12.5% on gains above ₹1.25 lakh per year at redemption. For most investors redeeming ₹50–80 lakh after 15 years, the LTCG bill could range from ₹3 lakh to ₹8 lakh depending on total gains and the annual exemption already used. This still leaves ELSS well ahead, but the gap shrinks from the headline comparison.

One smart strategy: consider systematic redemptions after the lock-in — withdraw in tranches across multiple financial years rather than all at once. This way, each year's ₹1.25 lakh LTCG exemption absorbs more of your gains, reducing your total tax outflow. Use CalcPhi's Capital Gains Tax Calculator to estimate your actual LTCG liability before planning a large ELSS redemption.

Liquidity: How Trapped Is Your Money?

PPF has a 15-year lock-in, with a few relief valves. You can take a loan against your PPF balance from year 3 to year 6 (up to 25% of the balance two years prior). From year 7 onwards, partial withdrawals are allowed — you can withdraw up to 50% of the balance at the end of the 4th year preceding the withdrawal year. But you cannot close the account before 15 years except in exceptional circumstances like critical illness or higher education.

ELSS has a 3-year lock-in per investment instalment. If you invest via SIP, each monthly instalment has its own individual 3-year lock-in. An investment made in April 2023 is free from April 2026; one made in March 2026 is free only from March 2029. After the lock-in, you can redeem fully or partially at any time — no questions asked, no penalty.

For someone who might need funds in an emergency before 15 years, ELSS provides far more flexibility. PPF, despite its loan facility, is not a liquid instrument.

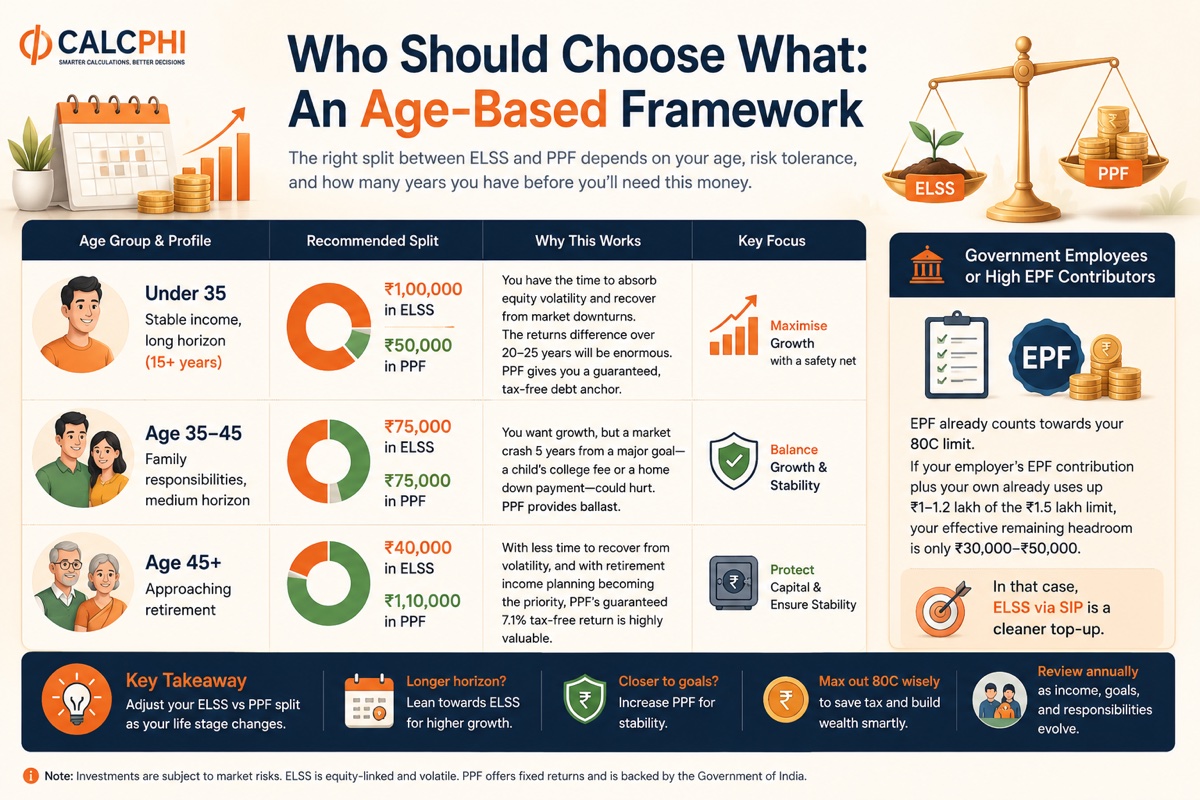

Who Should Choose What: An Age-Based Framework

The right split between ELSS and PPF depends heavily on your age, risk tolerance, and how many years you have before you'll need this money.

- Under 35, stable income, long horizon (15+ years): Put roughly ₹1 lakh in ELSS and ₹50,000 in PPF. You have the time to absorb equity volatility and recover from market downturns. The returns difference over 20–25 years will be enormous. The PPF allocation gives you a guaranteed, tax-free debt anchor.

- Age 35–45, family responsibilities, medium horizon: Split closer to ₹75,000 each. You want growth, but a market crash 5 years from a major goal — a child's college fee or a home down payment — could hurt. PPF provides ballast.

- Age 45+, approaching retirement: Shift the balance towards PPF. With less time to recover from volatility, and with retirement income planning becoming the priority, PPF's guaranteed 7.1% tax-free return is highly valuable. At this stage, capital preservation matters more than maximisation.

- Government employees or those with high EPF contributions: EPF already counts towards your 80C limit. If your employer's EPF contribution plus your own already uses up ₹1–1.2 lakh of the ₹1.5 lakh limit, your effective remaining headroom is only ₹30,000–₹50,000. In that case, ELSS via SIP is a cleaner top-up.

What About the Other 80C Options?

The ₹1.5 lakh 80C limit has over 15 eligible instruments — but most of them are not great investments.

Life insurance premiums (traditional endowment or money-back policies) should not be used for tax saving. The returns are typically 4–5% IRR over long tenures. Paying ₹1.5 lakh in premiums for a ₹46,800 tax saving while getting a poor investment in return is not a good trade. If you need life insurance, buy a pure term plan separately.

5-year bank tax-saver FDs currently yield around 6.5–7%, and interest is fully taxable at your slab rate. After tax, the post-tax yield for a 30% bracket taxpayer is approximately 4.5–4.9%. PPF at 7.1% tax-free beats this convincingly.

NPS (National Pension System) deserves a special mention: it qualifies for an additional ₹50,000 deduction under Section 80CCD(1B), over and above the ₹1.5 lakh 80C limit. This makes NPS complementary to ELSS and PPF, not a competitor. If you're on the old regime and want to reduce taxable income further, NPS is the next step after maxing out 80C. Run a side-by-side comparison of PPF, EPF, and NPS using CalcPhi's PPF vs EPF vs NPS Calculator.

The Practical Verdict

ELSS wins on returns over any horizon longer than 7 years, with reasonable confidence. PPF wins on safety, tax-free status, and psychological comfort — your money never goes down.

For most salaried Indians under 45 who are on the old tax regime, the ideal 80C allocation is not ELSS or PPF — it is a combination of both, weighted towards ELSS in your 20s and 30s and gradually rebalancing towards PPF as you approach retirement.

If you are on the new tax regime, Section 80C deductions are not available at all. Your investment decisions should then be driven purely by financial goals, not tax engineering.

Ready to see the exact numbers for your situation? Use CalcPhi's ELSS Calculator and PPF Calculator side by side to model your own corpus projections — no sign-up needed, all calculations run instantly in your browser.

Frequently Asked Questions

Can I invest in both ELSS and PPF in the same financial year?

Yes, absolutely. The ₹1.5 lakh 80C limit is a combined ceiling across all eligible instruments. You can split your ₹1.5 lakh investment in any proportion — ₹1 lakh in ELSS and ₹50,000 in PPF, for example — and the total deduction will still be capped at ₹1.5 lakh. There is no rule that restricts you to a single instrument.

Is ELSS actually risky for the 3-year minimum holding period?

Yes — equity markets can be negative over any 3-year window. If you invest in March 2026 at a market peak and are forced to redeem in March 2029 during a downturn, you could receive less than you invested, even after the tax saving. Financial planners generally recommend treating ELSS with a 5–7 year horizon, not the bare minimum 3-year lock-in. Use ELSS for long-term goals, not for money you may need in 3–4 years.

What is the current PPF interest rate for FY 2026-27?

The PPF interest rate is 7.1% per annum, compounded annually, as declared by the Ministry of Finance. It is reviewed quarterly and has been unchanged since April 2020. Interest is credited on 31 March each year and calculated on the lowest balance between the 5th and last day of each month — so always invest before the 5th of the month for that month's interest.

Does ELSS qualify for 80C deduction under the new tax regime?

No. The new tax regime (which is the default for AY 2026-27 under Finance Act 2023) does not allow deductions under Chapter VI-A, including Section 80C. If you are on the new regime, investing in ELSS still makes sense as an equity investment, but you will not get any tax deduction for it. PPF contributions also do not qualify for 80C under the new regime, though PPF interest remains tax-free regardless of which regime you're on.

Can I do SIP in ELSS, or must I invest a lump sum?

You can absolutely invest via SIP in ELSS. Many investors prefer it because it spreads market risk over the year through rupee cost averaging. The important thing to remember is that with SIP, each monthly instalment has its own 3-year lock-in from the date of that specific investment — so if you start in April 2026, your April instalment is locked until April 2029, your May instalment until May 2029, and so on.

Is LTCG on ELSS really significant enough to change my decision?

For most investors investing ₹1.5 lakh per year, the LTCG impact at redemption is moderate — typically ₹3–6 lakh on a 15-year ELSS corpus, spread over a few redemption years. Using the ₹1.25 lakh annual LTCG exemption wisely (by redeeming in tranches) can reduce this further. Even after LTCG, ELSS significantly outperforms PPF over 10+ year periods at reasonable return assumptions. The tax is a cost, not a dealbreaker — but it should be factored into your planning.

Disclaimer: CalcPhi calculators — including the ELSS Calculator, PPF Calculator, Section 80C Calculator, and Capital Gains Tax Calculator — are for educational and estimation purposes only. The projections shown are based on assumed rates of return and current tax rules, and do not constitute financial advice or a guarantee of future returns. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully and consult a SEBI-registered investment advisor or qualified Chartered Accountant before making investment decisions.