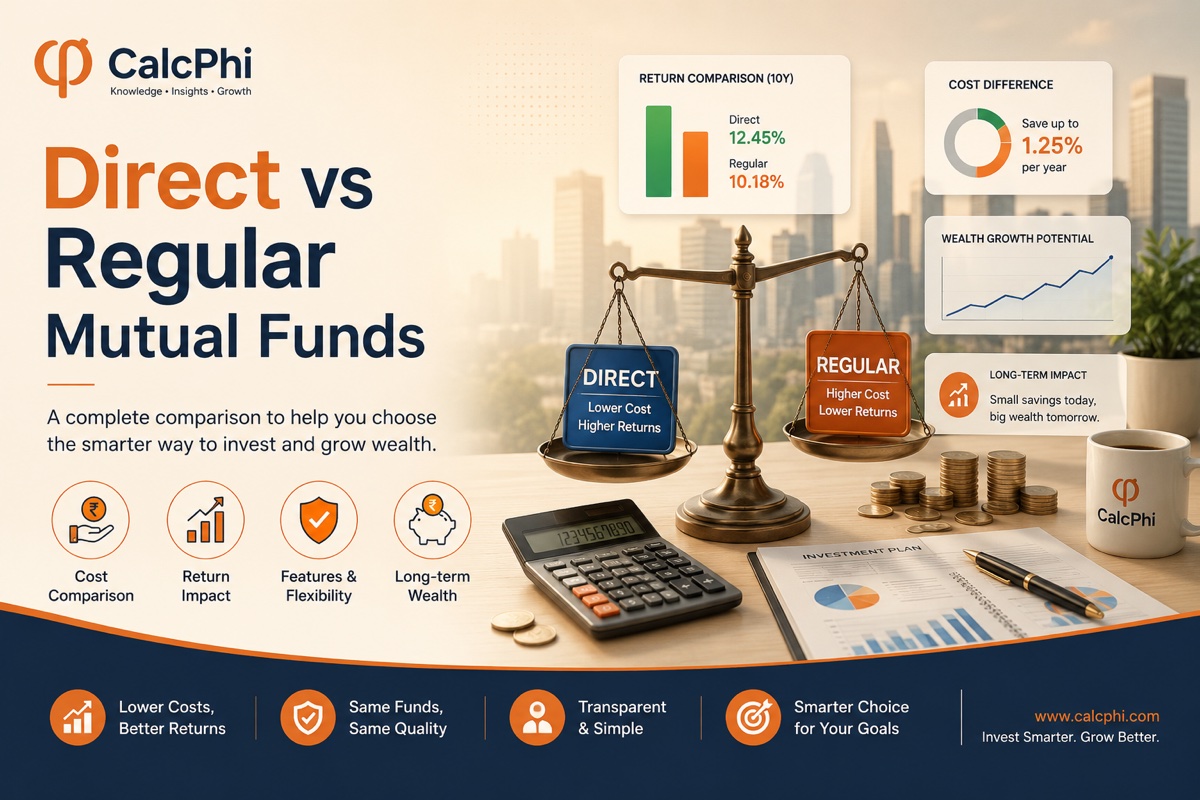

Direct vs Regular Mutual Funds: The Hidden Cost You're Paying Every Year

When you invest in a mutual fund in India, you almost always have two choices sitting right next to each other — a direct plan and a regular plan. They invest in the exact same stocks or bonds, managed by the exact same fund manager, following the exact same strategy. Yet one of them quietly takes more money from you every single year. That silent drain is the expense ratio gap between direct and regular mutual fund plans. And for millions of Indian investors, it adds up to lakhs of rupees lost over a 10-to-20-year investing journey — not because the market performed poorly, but simply because of which plan they chose at the start.

What Are Direct and Regular Mutual Fund Plans?

Every open-ended mutual fund in India is required by SEBI (Securities and Exchange Board of India) to offer two versions of the same scheme — a direct plan and a regular plan. This rule has been in place since January 2013.

A regular plan is what you typically buy when you invest through a distributor, broker, bank relationship manager, or a third-party financial app that earns a commission. The fund house pays that commission — called a "trail commission" — from the fund's assets every year. This cost is baked into the fund's expense ratio, which is the annual fee charged to manage your investment.

A direct plan cuts out the middleman entirely. You invest directly with the fund house or through SEBI-registered investment platforms, and no commission is paid to any distributor. The savings from this are passed on to you in the form of a lower expense ratio, which means a higher NAV (Net Asset Value) that grows faster over time.

The difference in expense ratios between a direct and a regular plan of the same fund typically ranges from 0.5% to 1.5% per year. In some actively managed equity funds, it can be as high as 2% annually. That might sound tiny — after all, it is just a fraction of a percent — but that is exactly where most investors make their mistake.

Why a 1% Difference in Expense Ratio Is a Really Big Deal

To understand why this matters so much, you need to understand how compounding works. Compounding means your returns generate their own returns over time. The longer you stay invested, the more powerfully it works in your favour. But compounding cuts both ways — costs compound too.

Let's say you invest ₹10 lakh as a lumpsum in an equity mutual fund for 20 years. The gross return of the fund (before expenses) is 12% per year.

- In the direct plan, the expense ratio is 0.5%, so your effective return is 11.5%. Your ₹10 lakh grows to approximately ₹88.1 lakh.

- In the regular plan, the expense ratio is 2%, so your effective return is 10%. Your ₹10 lakh grows to approximately ₹67.3 lakh.

The difference? ₹20.8 lakh — money that didn't go into bad investments or market crashes. It went to distributors and brokers as commissions, quietly, every single year, through a mechanism most investors never even look at. Use CalcPhi's free Direct vs Regular Mutual Fund Calculator to get the exact rupee difference for your own investment amount and tenure — no login, no sign-up needed.

The Expense Ratio, Explained Simply

The expense ratio is the annual fee a mutual fund charges to manage your money. It covers fund manager salaries, administrative costs, marketing, and — in the case of regular plans — distributor commissions. It is expressed as a percentage of your total investment and is deducted daily from the fund's NAV. You never see a separate invoice or deduction from your account. The fund simply grows slightly slower because the NAV is being reduced by this charge every trading day.

SEBI caps expense ratios in India based on the fund's Assets Under Management (AUM). For equity funds, the maximum expense ratio is 2.25% for the first ₹500 crore in AUM, going down in slabs as AUM grows. Direct plans must always have a lower expense ratio than regular plans of the same fund — that is a SEBI mandate.

As of AY 2026-27, a typical large-cap equity fund in India might charge: Direct plan 0.4% to 0.8%; Regular plan 1.5% to 2.0%. Index funds and ETFs have even lower expense ratios — often as little as 0.1% to 0.2% for direct plans — making the gap with regular index fund plans even more significant in proportional terms.

Real Numbers: What You're Actually Losing

Here is a comparison based on a ₹5,000 monthly SIP over 15 years at 12% gross annual return, with a 1.5% expense ratio difference between the two plans:

| Plan | Effective return | Total invested | Maturity value |

|---|---|---|---|

| Direct Plan | 11.5% | ₹9,00,000 | ₹27.8 lakh (approx.) |

| Regular Plan | 10.0% | ₹9,00,000 | ₹23.6 lakh (approx.) |

| Difference | — | — | ₹4.2 lakh |

Over ₹4 lakh lost — on a ₹5,000 monthly SIP. Increase that SIP to ₹15,000 per month and the gap triples to over ₹12 lakh. Extend the tenure to 20 years and the numbers become even more dramatic. Use CalcPhi's SIP Calculator to compare results at two different return rates and see the compounding impact of the expense ratio difference for your own numbers.

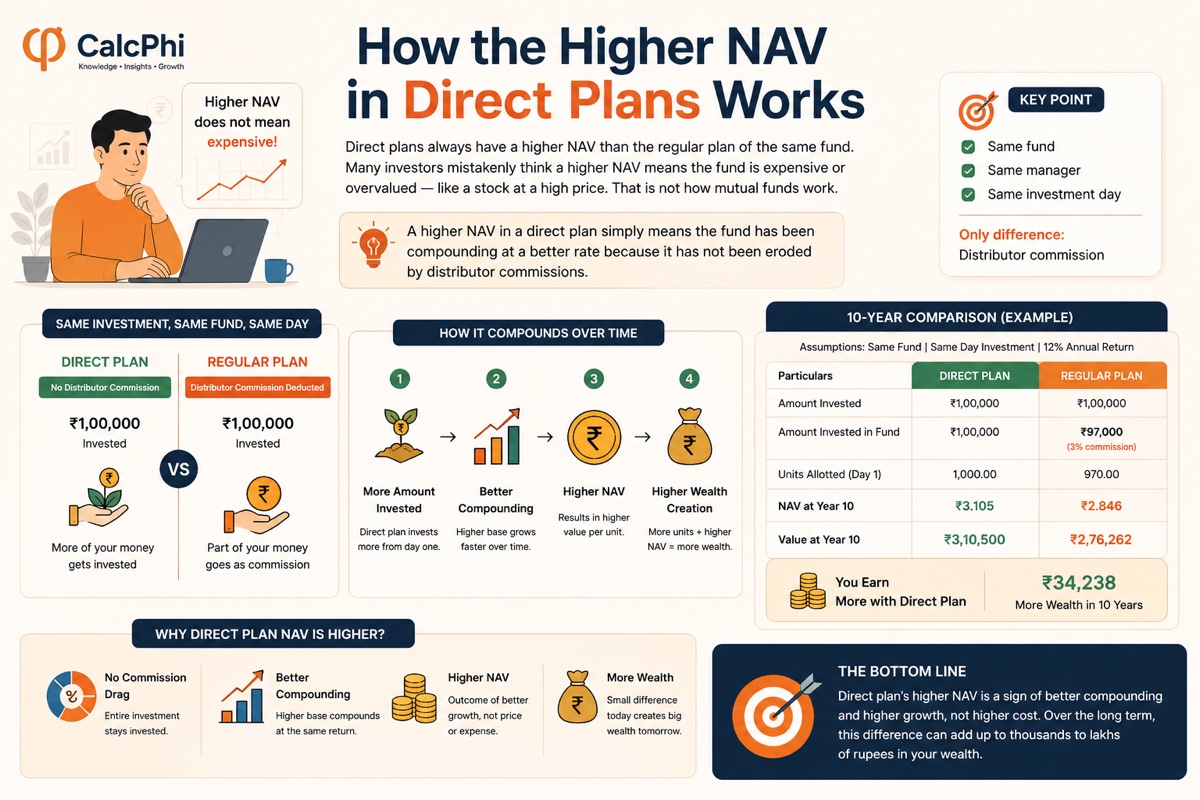

How the Higher NAV in Direct Plans Works

Direct plans always have a higher NAV than the regular plan of the same fund. Many investors mistakenly think a higher NAV means the fund is expensive or overvalued — like a stock at a high price. That is not how mutual funds work.

A higher NAV in a direct plan simply means the fund has been compounding at a better rate because it has not been eroded by distributor commissions. Two investors — one in direct, one in regular — put the same amount into the same fund on the same day. Over 10 years, the direct investor has more units worth more per unit. The regular investor has slightly fewer units worth slightly less per unit. The combined difference is thousands to lakhs of rupees.

When a Regular Plan Might Still Make Sense

This article is not arguing that all distributors and advisors are bad. A good SEBI-registered financial advisor genuinely earns their fee through personalised guidance — helping you pick suitable funds, avoid panic-selling during market downturns, review your portfolio annually, and stay aligned with your goals.

The real question is whether the value of that advice exceeds the cost of the regular plan's higher expense ratio. If you are the kind of investor who is likely to withdraw your SIP at the first sign of a market correction, exit at a loss, or park money in the wrong fund category altogether, a good advisor might actually help you earn more in a regular plan than you would have in a direct plan left to yourself.

But if you are a disciplined, informed investor who can manage your own portfolio — or use trusted, SEBI-compliant platforms — then direct plans are almost always the better financial choice. The data is unambiguous on this.

How to Switch From Regular to Direct Plans

Switching from a regular plan to a direct plan of the same fund is simpler than most people think. You can submit a switch request directly on the AMC (Asset Management Company) website, through CAMS or KFintech (the two main mutual fund registrars), or through SEBI-registered direct investment platforms like MFCentral.

Keep in mind that switching from a regular to a direct plan is treated as a redemption and fresh purchase for tax purposes. If your units have appreciated, you may trigger capital gains tax — either Short-Term Capital Gains (STCG) at 20% for units held less than 12 months, or Long-Term Capital Gains (LTCG) at 12.5% on gains above ₹1.25 lakh for equity funds held more than 12 months. Use CalcPhi's Capital Gains Tax Calculator to estimate your tax liability before switching.

For new investments, the decision is easy — always start in the direct plan unless you have a specific reason to use an advisor.

Direct vs Regular for Different Fund Categories

Actively managed equity funds see the largest difference, because both the gross expense ratio and the distributor commission are higher. A large-cap or flexi-cap fund can easily have a 1% to 1.5% gap between direct and regular plans.

Index funds and ETFs already have very low expense ratios. The gap between direct and regular index funds may be smaller in absolute percentage terms, but proportionally it is still significant. For example, a Nifty 50 index fund with a direct expense ratio of 0.1% and a regular expense ratio of 0.4% has a three-times higher cost in the regular version.

Debt funds sit somewhere in between. The gap is usually 0.5% to 1%, which matters more because debt fund returns are already modest — often 6% to 8% annually. A 0.75% expense ratio difference on a 7% gross return fund eats up over 10% of your annual return.

Track Your Expense Ratio Impact

Most investors look at their mutual fund returns in absolute terms — "my fund gave 15% last year" — without asking what it would have returned if they were in the direct plan instead. Checking your fund's expense ratio is simple: it is listed on every scheme's fund factsheet, available on the AMC website and on SEBI's mutual fund analytics portal (mfanalysis.sebi.gov.in).

Use CalcPhi's Expense Ratio Impact Calculator to plug in your fund's expense ratio and see exactly how much it costs you in real rupees over 10, 15, or 20 years.

Frequently Asked Questions

Is a direct mutual fund plan better than a regular plan for long-term investing?

In most cases, yes. For the same fund, the direct plan has a lower expense ratio because no distributor commission is paid. Over 10 to 20 years, this difference compounds into a significantly larger final corpus. However, if you genuinely need ongoing financial advice and your advisor adds measurable value to your investment decisions, the cost of a regular plan may be justified.

What is the typical expense ratio difference between direct and regular mutual fund plans in India?

The difference typically ranges from 0.5% to 1.5% per year for actively managed equity funds. For index funds, the gap is smaller in percentage terms but still proportionally meaningful. SEBI mandates that direct plans must always have a lower expense ratio than the corresponding regular plan.

Does switching from a regular plan to a direct plan trigger capital gains tax?

Yes. Switching is treated as a redemption of your regular plan units and a fresh purchase of direct plan units. Any gains made on your existing regular plan units will be subject to capital gains tax — STCG at 20% (if held under 12 months) or LTCG at 12.5% on gains exceeding ₹1.25 lakh (if held over 12 months) for equity funds. It is advisable to calculate your potential tax before making the switch.

Can I invest in direct plans without a financial advisor?

Yes. You can invest directly through the AMC's website, through CAMS or KFintech portals, or through SEBI-registered direct investment platforms. These require basic KYC compliance but no distributor involvement. Many Indian investors now manage their own direct plan portfolios successfully.

Why does the direct plan have a higher NAV than the regular plan of the same fund?

A higher NAV in the direct plan reflects better compounding over time due to the lower expense ratio. It does not mean the fund is expensive — in fact, it means more value has accumulated per unit for the investor. This is a sign of a healthier investment trajectory, not a reason to avoid the direct plan.

How do I check whether my current mutual fund investments are in a direct or regular plan?

Check your account statement from CAMS or KFintech, or log into your AMC account. The plan type (Direct or Regular) will be explicitly listed alongside the scheme name. If you see the word "Regular" in the scheme name or if you originally invested through a bank, broker, or distributor, you are almost certainly in a regular plan.

Disclaimer: The figures and calculations in this article are for educational and illustrative purposes only. Actual returns will vary depending on market performance, fund selection, expense ratios, and individual tax situations. Nothing in this article constitutes personalised financial advice. Please consult a SEBI-registered financial advisor before making investment decisions.