Credit Score India 2026 — Complete Guide to CIBIL Score, Ranges, and How to Improve

Most Indians discover their credit score the same way — sitting in front of a bank officer, having just applied for a home loan or a car loan, and being told the application cannot move forward. Your credit score is a three-digit number between 300 and 900 that tells lenders how reliably you repay money. A difference of just 100 points on your CIBIL score can translate to a lower interest rate that saves you ₹5–10 lakh over the life of a home loan. This guide covers what the score means, how it is calculated, what each range means for your borrowing life, and a step-by-step plan to improve it.

What Is a Credit Score and Who Calculates It in India?

A credit score is a numerical summary of your credit behaviour, computed by licensed credit bureaus using data reported by banks and lenders. In India, four bureaus are licensed by the RBI to issue credit scores.

TransUnion CIBIL is the oldest and most widely used bureau, operating since 2000. When lenders say "your CIBIL score," they mean this bureau's score — it is the benchmark used by SBI, HDFC, ICICI, Axis, and most major banks. CIBIL scores range from 300 to 900. Experian is the second most commonly referenced bureau (scores 300–850) and is often used by NBFCs and fintech lenders. Equifax and CRIF High Mark are the other two RBI-licensed bureaus; CRIF is particularly prominent in microfinance and rural credit.

For most practical purposes, your CIBIL score is the number that matters most. But if you are ever rejected by one lender, it is worth checking all four bureau reports — errors in one bureau's data do not automatically appear in others.

CIBIL Score Ranges — What Each Band Actually Means

750 to 900 — Excellent. The sweet spot that most major banks treat as prime. You typically receive the bank's lowest available interest rates, faster approval timelines, and higher loan amounts relative to your income. Credit card issuers will offer higher limits and premium cards. Getting here and staying here should be the goal for anyone who expects to borrow in the next three to five years.

700 to 749 — Good. You will get approved by most lenders, but may not qualify for the lowest promotional rates. Banks may add a 0.25–0.50% spread over their best rates. On a ₹50 lakh home loan, that extra 0.50% translates to roughly ₹880 more per month in EMI and nearly ₹2.1 lakh more in total interest over 20 years.

650 to 699 — Fair. Approvals are possible but conditional. Most PSU banks will ask for additional collateral or a co-applicant. Private banks and NBFCs may approve at rates 1–1.5% higher than their prime rates. Unsecured personal loans become expensive in this range — expect interest rates north of 14–16%.

600 to 649 — Poor. Mainstream banks typically decline home loan applications in this range. Approvals are available from co-operative banks, housing finance companies, or NBFCs — but at rates of 11–14% and lower LTV ratios, meaning a larger down payment is required.

300 to 599 — Very Poor. Most formal lenders will not extend credit. If credit is available, it comes through informal NBFCs or microfinance institutions at 18–30%. This range usually reflects a history of missed EMIs, defaults, or accounts sent to collections.

-1 or NH — No History. Not a low score. It means you have never borrowed from a formal lender or held a credit card. Banks cannot assess your risk because there is no data. The fix is straightforward: build a credit history deliberately.

How Your CIBIL Score Is Calculated — The Five Factors

| Factor | Weight | What Hurts Most |

|---|---|---|

| Payment history (EMIs, credit card dues) | 35% | Even one 30-day late payment can drop score 50–80 points |

| Credit utilisation ratio | 30% | Using above 30% of combined credit limit signals stress |

| Credit history length | 15% | Closing your oldest card reduces average account age |

| Credit mix (secured + unsecured) | 10% | Only credit cards, no loans — limited profile diversity |

| New credit enquiries | 10% | Multiple loan applications in short period — 5–10 pts per enquiry |

How a 100-Point Score Difference Costs You Lakhs on a Home Loan

The financial impact of your credit score is not abstract. Here is how a score difference plays out on a ₹50 lakh home loan over 20 years.

| CIBIL Score | Approximate Rate | Monthly EMI | Total Interest Paid |

|---|---|---|---|

| 750 and above | 8.50% | ₹43,391 | ₹54.1 lakh |

| 700 to 749 | 8.75% | ₹44,168 | ₹56.0 lakh |

| 650 to 699 | 9.25% | ₹45,742 | ₹59.8 lakh |

| Below 650 | 10.00%+ | ₹47,951+ | ₹65.1 lakh+ |

The difference between a 750 score and a 650 score on the same ₹50 lakh home loan is approximately ₹5.7 lakh in additional interest over 20 years — money that leaves your pocket purely because of a three-digit number. Use CalcPhi's Home Loan EMI Calculator to compare different rates side by side.

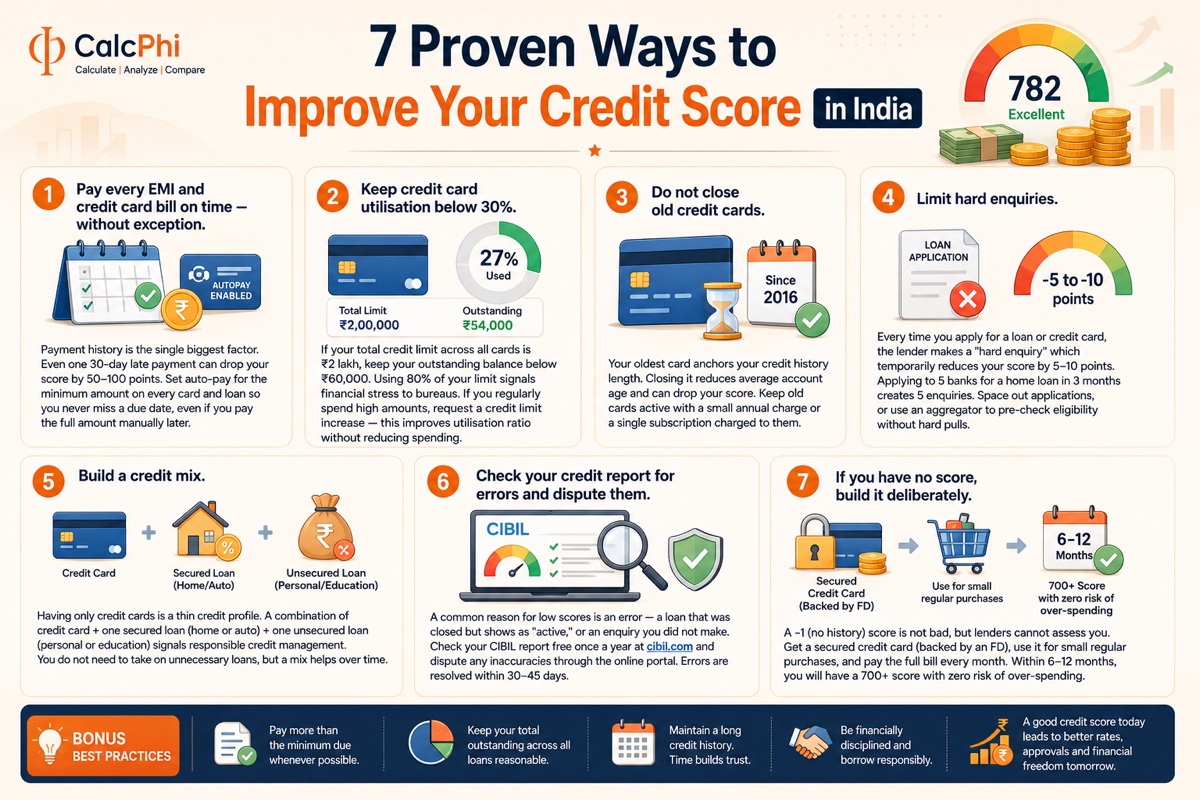

7 Proven Steps to Improve Your CIBIL Score in 2026

1. Pay Every Bill on Time — Every Single Time

Set up auto-pay for the minimum amount due on every credit card and every loan EMI. Even if you intend to pay the full amount manually, the auto-pay acts as a safety net so you never accidentally miss a due date. One missed payment that goes 30 days overdue can undo months of careful credit building. If you have an old overdue amount — called a "settled" or "written off" account — contact the lender to negotiate payment, get a No Objection Certificate (NOC), and confirm the status is updated in bureau records.

2. Bring Your Credit Utilisation Below 30%

If you are currently using more than 30% of your combined credit card limits, this is costing you points every month. Pay down card balances, or call your bank and request a credit limit increase — both achieve the same mathematical result. One nuance: utilisation is typically measured at the statement generation date, not the payment due date. Paying your balance a few days before statement date — rather than on the due date — can significantly improve your reported utilisation ratio.

3. Never Close Your Oldest Credit Card

Your oldest card is the anchor of your credit history length. Even if you no longer use it regularly, keep it alive. Charge one small recurring expense to it — a streaming subscription, a utility bill — and pay it off automatically each month. This keeps the account active, prevents the bank from closing it due to inactivity, and maintains your credit history length without any active effort.

4. Limit Hard Enquiries Before a Major Loan Application

If you are planning to apply for a home loan or car loan in the next six months, stop applying for new credit cards or personal loans. Every new application triggers a hard enquiry. Give your score a clean window of at least three to six months before your major loan application. Use eligibility checkers on platforms like Paisabazaar or BankBazaar, which use soft enquiries that do not affect your score.

5. Build a Balanced Credit Mix Over Time

If your entire credit profile consists only of credit cards, consider taking a small secured loan — a gold loan or a two-wheeler loan — and repaying it on schedule. Conversely, if you have only one home loan and no credit card, getting a card and using it responsibly adds diversity. You do not need to take on unnecessary debt, but a mix of secured and unsecured credit improves your score over 12–24 months.

6. Check Your Credit Report for Errors and Dispute Them

One of the most under-appreciated reasons for a low score is data errors — a closed loan still showing as active, an EMI marked as missed when it was paid, or a loan account belonging to someone with a similar name. Every Indian is entitled to one free credit report per year from each of the four bureaus. Check your CIBIL report at cibil.com and your Experian report at experian.in. If you find an error, raise a dispute through the bureau's online portal — CIBIL disputes are typically resolved in 30–45 days. If an error is validated and removed, your score can improve significantly within one or two billing cycles.

7. Build Credit Deliberately If You Have No History

A -1 or NH score is not a penalty — it is simply a blank slate. The fastest way to build from scratch is a secured credit card, backed by a fixed deposit. Deposit ₹10,000–₹25,000 with the bank and they issue a card with a credit limit equal to 80–100% of your deposit. Use it for small, regular purchases — groceries, fuel, utility payments — and pay the full outstanding amount every month before the due date. Within six months you will have an active account and on-time payment history. Within 12 months, most people reach a score above 700.

How Long Does It Take to Improve Your Score?

| Current Situation | Target | Realistic Timeline |

|---|---|---|

| No history (score -1 or NH) | 700+ | 6 to 12 months using a secured credit card |

| Score 600–650 with a few late payments | 700+ | 12 to 18 months of clean repayment |

| Score 550–600 with multiple missed EMIs | 700+ | 18 to 24 months after clearing all overdues |

| Score 700–750, want to reach 800+ | 800+ | 12 to 18 months of perfect payment + low utilisation |

There are no shortcuts. Products that claim to "fix" your credit score in 30 days are at best useless and at worst fraudulent. The only thing that improves a credit score is time plus positive credit behaviour.

Common Credit Score Myths — Debunked

Myth: Checking my own score will reduce it. False. Checking your own score is a soft enquiry and has zero impact. Only hard enquiries — made by lenders when you apply for credit — reduce your score. Check your score as often as you want.

Myth: A high income means a high credit score. Your income does not appear in your credit score calculation. A person earning ₹5 lakh a year with a perfect repayment record will have a higher score than someone earning ₹50 lakh who misses EMIs. Score reflects repayment behaviour, not wealth.

Myth: Closing a loan early always helps your score. Prepaying a loan is financially smart, but it does not boost your credit score — and closing the account removes a positive active account from your profile. What helps your score is having accounts that are currently active and in good standing.

Myth: A "settled" account is as good as a fully paid account. A settlement — where the lender agrees to accept less than the full outstanding amount — is reported to bureaus as "settled," not "closed." This negative tag stays on your report for seven years and signals to future lenders that you did not fully repay your debt.

Your Credit Score and Loan Eligibility in 2026

For home loans, most PSU banks (SBI, Bank of Baroda, PNB) prefer a minimum score of 700, with best rates starting at 750. Housing finance companies like LIC Housing Finance and PNB Housing may approve at 650 but with stricter LTV caps — meaning a larger down payment. Use CalcPhi's Home Loan EMI Calculator to see exactly how your rate affects monthly payments.

For personal loans, the bar is higher because there is no collateral involved. Most banks want 720 or above for an unsecured personal loan at reasonable rates. Below 700, personal loans from NBFCs carry 15–24% interest. Use CalcPhi's Personal Loan EMI Calculator to understand what those higher rates mean for your monthly outgo before committing.

For car loans, banks typically approve at 680 and above because the vehicle serves as collateral. Use CalcPhi's Car Loan EMI Calculator to compare EMIs across different rate scenarios. For credit cards, premium cards typically require 750 and above; entry-level cards are available at 650 and sometimes lower.

Check your EMI affordability before applying for any loan:

Loan Eligibility Calculator → EMI Calculator →Frequently Asked Questions

-

What is a good CIBIL score in India in 2026?

A score of 750 or above is considered excellent and opens access to the best interest rates from most major banks. Scores between 700 and 749 are good and will receive standard approvals. Anything below 650 makes loan approval more difficult and significantly more expensive. Aim for 750 as your minimum target if you plan to take a home loan in the next two to three years.

-

How can I check my CIBIL score for free?

You are entitled to one free credit report per year from each bureau. Get your CIBIL report at cibil.com, your Experian report at experian.in, and your CRIF report at crifhighmark.com. Paisabazaar, BankBazaar, and OneScore also offer free score checks with no impact on your score. Many major banks — HDFC, Axis, SBI — also display your CIBIL score within their mobile banking apps.

-

Does checking my own credit score reduce it?

No. When you check your own credit score, it counts as a soft enquiry and has absolutely no effect on your score. Only hard enquiries — made by lenders when you formally apply for credit — reduce your score, and only by 5–10 points per enquiry. Check your score at least once every three to four months to catch errors early.

-

Why did my credit score drop suddenly when I did nothing wrong?

Several things can cause an unexpected drop without missing a payment. Your credit utilisation may have spiked because you had a large balance on the statement date. A new hard enquiry from a credit card application may have registered. An old card may have been closed by the issuer due to inactivity. Or there may be a data error in your report. Check your full CIBIL report immediately — it will show all recent changes and any negative flags.

-

What credit score is needed for a home loan in India?

Most major banks prefer a minimum CIBIL score of 700 for home loan approval. A score of 750 or above qualifies you for the lowest available rates, which translates to significant savings over a 20-year tenure. If your score is below 700, consider spending 12–18 months improving it before applying — the interest rate savings will far outweigh the wait.

-

Can I get a loan with a CIBIL score of 600?

Yes, but with limitations. NBFCs and housing finance companies may approve loans at a score of 600–649, but at interest rates 1.5–3% higher than the prime rate. On a ₹40 lakh home loan over 20 years, a 2% higher rate adds approximately ₹10–12 lakh to your total repayment. It is almost always better to spend 12–18 months improving your score first, unless the loan is genuinely urgent.

Disclaimer: The information in this article is for educational and general awareness purposes only. Credit score ranges, interest rates, and lender policies are subject to change. Nothing in this article constitutes financial advice or a guarantee of loan approval at any interest rate. Loan eligibility and interest rates are determined by individual lenders based on multiple factors beyond credit score alone. Please consult a qualified financial advisor or credit counsellor for personalised guidance.