Car Loan vs Paying Outright: When Does Taking a Car Loan Actually Make Sense in India?

Buying a car is a milestone moment for most Indian families. And right after you pick the model, you face a decision that will follow you for the next three to seven years — should you take a car loan and pay in EMIs, or should you pay the full amount upfront in cash? Both options have real merit. Neither is universally right. But by looking at the numbers clearly, you can figure out which one saves you more money — or gives you more financial flexibility — based on your specific situation.

What Is a Car Loan EMI and What Does It Actually Cost You?

EMI stands for Equated Monthly Instalment. When you take a car loan, the bank or NBFC (Non-Banking Financial Company) lends you a portion of the car's on-road price, and you repay that amount plus interest in fixed monthly payments over an agreed tenure — typically 12 to 84 months (1 to 7 years).

The interest rate on car loans in India currently ranges from about 8.5% to 13% per annum, depending on your lender, credit score (CIBIL score), the type of vehicle (new or used), and whether you are a salaried or self-employed borrower. Major banks like SBI, HDFC Bank, ICICI Bank, and Axis Bank typically offer new car loan rates starting around 8.5% to 9.5% p.a. for borrowers with a good CIBIL score (750 and above). Used car loans are more expensive, often ranging from 11% to 15% p.a.

Consider a real example. You want to buy a car with an on-road price of ₹10 lakhs. You pay ₹2 lakhs as a down payment and take a loan of ₹8 lakhs at 9% p.a. for 5 years (60 months). Your monthly EMI works out to approximately ₹16,607. By the end of the 5-year tenure, you will have paid back roughly ₹9,96,420 — meaning ₹1,96,420 goes purely towards interest. That is nearly 25% extra on top of the amount you borrowed. Use CalcPhi's free Car Loan EMI Calculator to check these numbers with your own loan amount and tenure — it shows your exact EMI, total interest, and a year-by-year repayment breakdown with no sign-up needed.

The Case for Paying Outright in Cash

If you have the full amount available, paying cash for a car keeps things simple and saves you a significant sum. Sticking with the ₹10 lakh example: pay in full upfront and your total cost is exactly ₹10 lakhs. Take the loan and the same car costs you ₹11.96 lakhs over five years. That ₹1.96 lakh difference is real money you keep in your pocket by not borrowing.

Beyond the interest saving, paying cash gives you stronger negotiating power at the dealership. Car dealers often earn a commission when they arrange financing through their tie-up lenders — this is called a dealer subvention. When you walk in as a cash buyer, that incentive disappears. Dealers are often willing to offer better discounts, free accessories, or reduced on-road costs to close a cash sale quickly.

There is also the peace of mind factor. You own the car outright from day one. There is no bank lien on your vehicle's RC book, no EMI to worry about if your income dips for a month, and no risk of the bank repossessing the vehicle if you miss payments during a rough patch.

The obvious constraint: you need to have the entire amount available — not just saved, but comfortably available without wiping out your emergency fund or stopping your investments entirely.

The Case for Taking a Car Loan

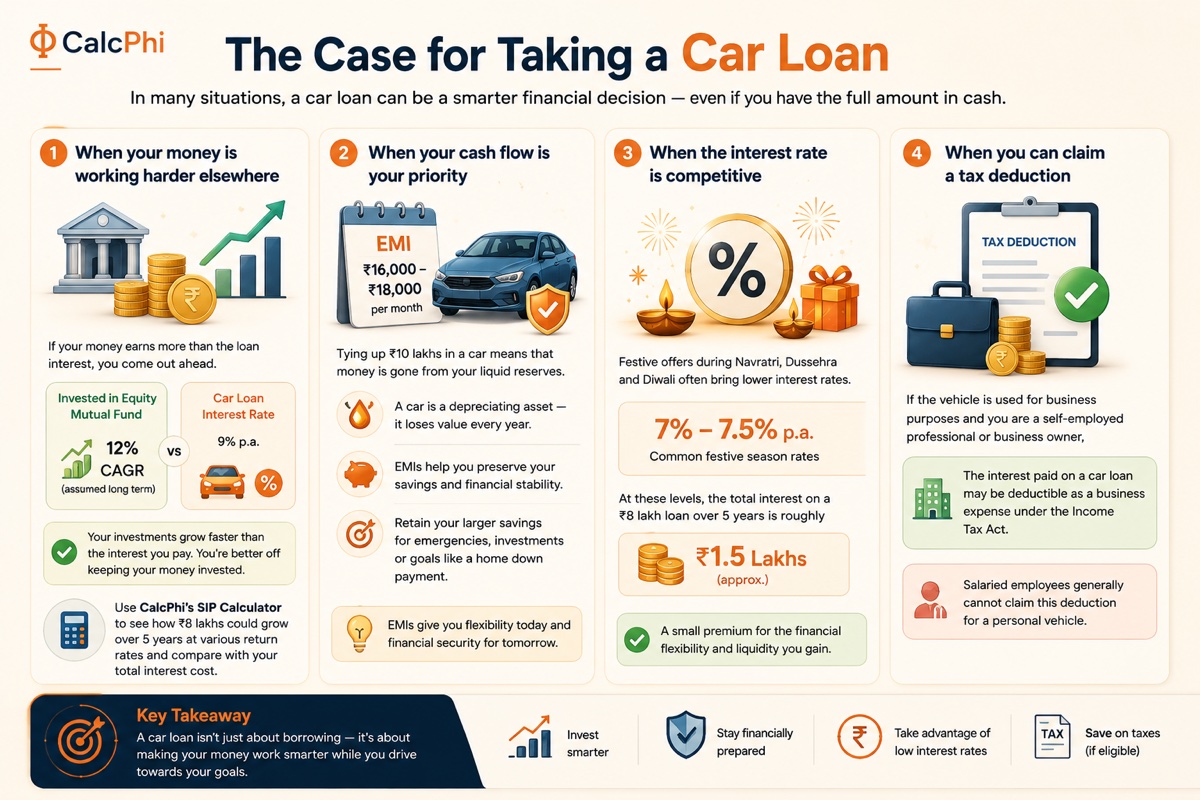

Here is the part many people miss: in certain situations, taking a car loan is the smarter financial move — even if you have the full amount in cash.

When your money is working harder elsewhere. If you have ₹8 lakhs sitting in a fixed deposit earning 7% p.a. and you take a car loan at 9% p.a., the net cost of borrowing is 2% per year. But if that same ₹8 lakhs is invested in an equity mutual fund that has historically delivered 12% CAGR over the long term, the calculation changes completely. Your investments grow faster than the interest you pay, meaning you are effectively better off by keeping the money invested and taking the loan. Use CalcPhi's SIP Calculator to see exactly how ₹8 lakhs could grow over 5 years at various return rates and compare that to your total interest cost.

When your cash flow is your priority. Even if you can pay outright, tying up ₹10 lakhs in a car means that money is gone from your liquid reserves. A car is a depreciating asset — it loses value every year. Breaking the cost into an EMI of ₹16,000 to ₹18,000 per month lets you retain your larger savings for emergencies, investments, or goals like a home down payment.

When the interest rate is competitive. Festive season offers — particularly during Navratri, Dussehra, and Diwali — often come with manufacturer-subsidised interest rates. Rates of 7% to 7.5% p.a. are not unusual during these periods. At those levels, the total interest on a ₹8 lakh loan over 5 years drops to roughly ₹1.5 lakhs — a much smaller premium for the financial flexibility you gain.

When you can claim a tax deduction. If the vehicle is used for business purposes and you are a self-employed professional or business owner, the interest paid on a car loan may be deductible as a business expense under the Income Tax Act. This can meaningfully reduce the effective cost of borrowing. Salaried employees generally cannot claim this deduction for a personal vehicle.

A Real Numbers Comparison: Cash vs EMI in India

Let us walk through both scenarios side by side for a ₹10 lakh car purchase.

Scenario A — Pay the full ₹10 lakhs in cash. Total cost: ₹10 lakhs. No interest. Car is yours immediately. ₹10 lakhs is gone from your savings.

Scenario B — Pay ₹2 lakhs down, take a ₹8 lakh loan at 9% for 5 years. EMI: ₹16,607/month. Total repaid: ₹11.96 lakhs. Total interest paid: ₹1.96 lakhs. Meanwhile, the ₹8 lakhs you did not spend upfront stays invested in an equity mutual fund. At 12% CAGR over 5 years, that ₹8 lakhs grows to approximately ₹14.1 lakhs.

Net position in Scenario B: ₹14.1 lakhs in investments minus ₹1.96 lakhs in interest paid — you are meaningfully ahead because your money compounded in the background. This assumes your investments genuinely earn 12% CAGR, which is not guaranteed, but it illustrates why the "always pay cash" rule is too simple. Use CalcPhi's Lumpsum Calculator to model how your money grows if you invest instead of spending it outright.

| Factor | Pay Cash | Take Loan |

|---|---|---|

| Upfront outflow | ₹10,00,000 | ₹2,00,000 (down payment) |

| Monthly EMI | — | ₹16,607 |

| Total interest paid | ₹0 | ₹1,96,420 |

| Total cost of car | ₹10,00,000 | ₹11,96,420 |

| ₹8L invested at 12% CAGR (5 yr) | ₹0 | ₹14,10,000 (approx.) |

| Net financial position | Car owned, no savings | Car owned + ~₹12.1L net gain |

When a Car Loan Is a Bad Idea

Despite the scenarios above, there are clear situations where borrowing for a car will hurt you.

Stretching to a car that is beyond your means because the EMI looks manageable is one of the most common financial mistakes. A ₹20 lakh car on a 7-year loan at 10% p.a. means an EMI of around ₹33,000 per month and total interest of approximately ₹7.7 lakhs. If your take-home salary is ₹60,000 per month, that EMI represents over 55% of your income — leaving almost no room for rent, groceries, savings, or emergencies. As a general rule, your total EMIs (all loans combined) should not exceed 40–50% of your net monthly income.

Taking a high-interest personal loan to buy a car because you do not qualify for a car loan is another trap. Personal loan rates in India range from 11% to 24% p.a. — far more expensive than a standard car loan.

Finally, buying a car on loan without having an emergency fund is risky. If you lose your job or face a medical emergency, you will still owe the bank that EMI every month. Build your emergency fund (at least 3 to 6 months of expenses) before you take on any new loan obligation.

New Car vs Used Car: Does It Change the Loan Decision?

Yes, significantly. Used car loans in India attract higher interest rates — typically 11% to 15% p.a. — because lenders consider the collateral less reliable as it ages. Lenders also typically finance only 70% to 80% of a used car's valuation, meaning you need a larger down payment.

If you are buying a used car in the ₹3 lakh to ₹6 lakh range, it is often smarter to save up and pay cash, given the higher borrowing cost and smaller loan amount. For a new car above ₹8 to ₹10 lakhs, the EMI route becomes worth analysing properly.

Tips to Reduce Your Car Loan Cost in India

If you decide a car loan is right for you, a few smart habits can reduce what you pay. Negotiate the on-road price before discussing the loan. Once the deal is done, approach your bank directly for financing rather than relying solely on the dealer's arrangement. A CIBIL score above 750 typically unlocks the lowest available rates. Make a larger down payment if you can — reducing the principal by even ₹1 to ₹2 lakhs can save tens of thousands in interest. And if your loan allows prepayment without penalty, use any annual bonus or windfall to pay it down early.

Use CalcPhi's EMI Calculator to compare how different tenures and interest rates affect your total outgo — running three or four scenarios takes less than two minutes and can save you a meaningful amount over the life of your loan.

Frequently Asked Questions

-

Is it better to take a car loan or pay cash in India?

There is no single right answer — it depends on what your cash would otherwise do. If you have investments earning returns higher than your loan interest rate, keeping money invested and taking a loan can make financial sense. If you have no investments and the cash is sitting idle in a savings account, paying outright saves you the interest cost and keeps things simple.

-

What is the current car loan interest rate in India in 2026?

New car loan rates from major banks like SBI, HDFC Bank, and ICICI Bank currently range from approximately 8.5% to 9.5% p.a. for borrowers with a good CIBIL score. Used car loan rates are higher, typically 11% to 15% p.a. Rates can vary based on your income, credit score, and loan tenure.

-

How much down payment should I make on a car loan in India?

Most banks in India finance up to 85% to 90% of a new car's on-road price. However, making a larger down payment — ideally 20% to 30% — reduces your loan principal, your EMI, and your total interest paid. It also reduces the risk of being in a situation where you owe more than the car's current resale value.

-

Can I get a tax benefit on a car loan in India?

Salaried individuals generally cannot claim a tax deduction on car loan interest for a personal vehicle. However, if you are self-employed, a freelancer, or a business owner and the car is used for business purposes, the interest component of the EMI may be deductible as a business expense. Consult a chartered accountant (CA) to understand what applies to your specific situation.

-

How does a car loan affect my CIBIL score?

Taking a car loan and repaying it on time each month can actually improve your CIBIL score over time, as it demonstrates disciplined credit behaviour. However, missing EMI payments will negatively impact your score. Before taking a loan, ensure that the EMI comfortably fits your monthly budget so you never have to miss a payment.

-

Is it worth foreclosing a car loan early in India?

Foreclosing (paying off) your car loan before the end of the tenure saves you the remaining interest. However, many lenders charge a foreclosure fee of 2% to 5% on the outstanding principal. Check your loan agreement before foreclosing — if the fee is low and you have surplus cash, early closure can be worth it.

Disclaimer: The information in this article is for educational and general informational purposes only. CalcPhi calculators are estimation tools and do not constitute financial advice. Car loan interest rates, tax rules, and lender policies change periodically and vary by lender and borrower profile. Please consult a qualified financial adviser or chartered accountant before making any borrowing or investment decisions.