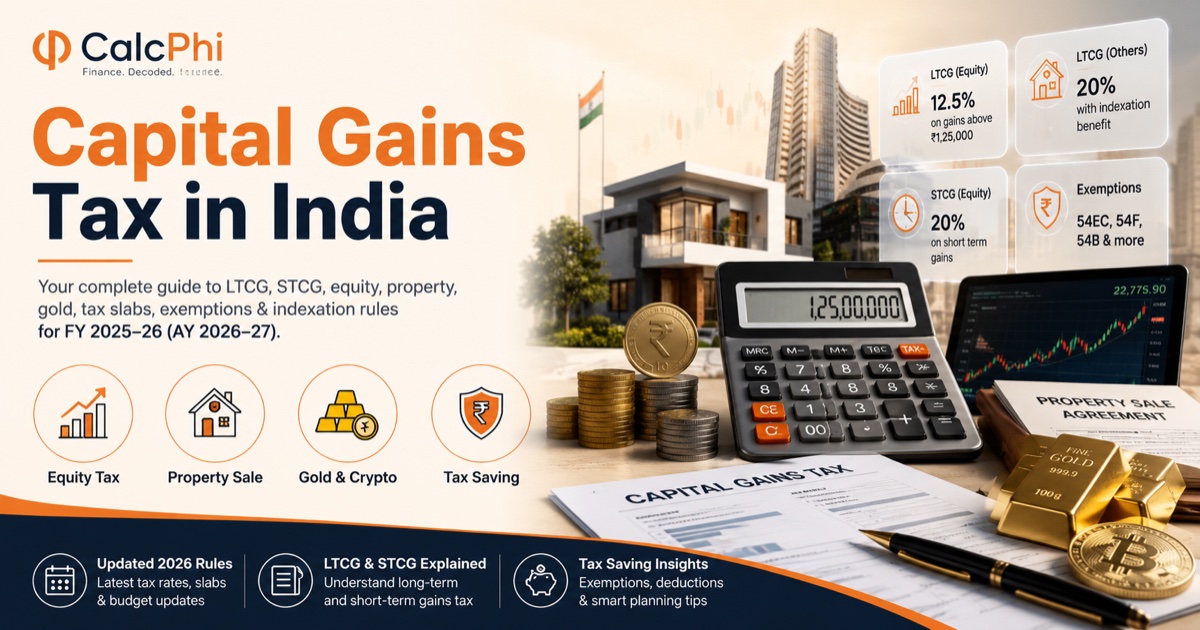

Capital Gains Tax in India 2026: STCG, LTCG, and What Changed in Budget 2024

If you have sold shares, mutual funds, property, or gold in the last year, there is a good chance your tax bill looks different from what you expected. That is because the Union Budget 2024 — through the Finance (No. 2) Act, 2024 — introduced some of the most significant changes to India's capital gains tax rules in decades. New rates, revised holding periods, and the removal of indexation benefits all kicked in from July 23, 2024. This guide breaks down everything you need to know about capital gains tax in India for FY 2025-26 (AY 2026-27).

What Is Capital Gains Tax in India?

When you sell a "capital asset" — such as stocks, real estate, mutual fund units, or gold — and earn a profit on that sale, the profit is called a capital gain. The Indian government taxes this gain under the Income Tax Act, 1961. Capital gains are split into two types based on how long you held the asset before selling it. If you sold after a short holding period, your gain is a Short-Term Capital Gain (STCG). If you held for longer, it qualifies as a Long-Term Capital Gain (LTCG). The holding period threshold — and the tax rate — depends on the type of asset.

Capital gains tax is separate from your regular income tax on salary or business income. Different rules, different rates, and in some cases, different exemptions apply.

How Holding Periods Changed After July 23, 2024

Before Budget 2024, India had three different holding period buckets: 12 months, 24 months, and 36 months, depending on the asset class. The Finance (No. 2) Act, 2024 simplified this significantly. From July 23, 2024 onwards, there are now just two holding period thresholds for most assets:

- Listed securities (equity shares, equity mutual funds, REITs, InvITs): An asset is considered long-term if held for more than 12 months.

- All other assets (property, gold, debt mutual funds, unlisted shares, etc.): An asset is considered long-term if held for more than 24 months.

Previously, unlisted shares and immovable property required a 36-month holding period to qualify for long-term status. That threshold was reduced to 24 months, which is good news for real estate investors.

STCG Tax Rates in India (AY 2026-27)

Short-Term Capital Gains are taxed depending on the type of asset sold.

Equity shares and equity-oriented mutual funds (where STT is paid): These fall under Section 111A of the Income Tax Act. The STCG tax rate was increased from 15% to 20% effective July 23, 2024. This applies to listed shares, equity mutual funds, equity ETFs, and units of business trusts where Securities Transaction Tax (STT) has been paid at the time of sale.

All other assets (property, gold, debt funds, unlisted shares): Short-term gains on non-equity assets do not have a fixed flat rate. Instead, they are added to your total taxable income and taxed at your applicable income tax slab rate. So if you are in the 30% bracket, your STCG on property sold within 24 months is also taxed at 30%.

LTCG Tax Rates in India (AY 2026-27)

Long-Term Capital Gains received a sweeping rationalisation in Budget 2024.

Equity shares and equity mutual funds — Section 112A: LTCG on listed equities and equity-oriented mutual funds where STT is paid is taxed at 12.5% on gains above ₹1.25 lakh per financial year. The earlier exemption limit was ₹1 lakh — Budget 2024 increased it to ₹1.25 lakh. Gains up to ₹1.25 lakh in a financial year are completely exempt from tax. Gains above that threshold are taxed at 12.5% without the benefit of indexation.

All other assets — Section 112: For property, gold, debt mutual funds, unlisted shares, and other non-equity capital assets, the LTCG rate is now a flat 12.5% without indexation. Before Budget 2024, this rate was 20% with indexation. The government reduced the rate but simultaneously removed the indexation benefit for most asset classes.

There is one important exception: for immovable property acquired before July 23, 2024, resident individuals and HUFs have the option to choose between 12.5% without indexation OR 20% with indexation — whichever results in lower tax. This grandfathering provision was introduced to protect property owners from a sudden jump in tax burden.

Calculate exactly how much LTCG or STCG tax you owe on your investments using CalcPhi's free Capital Gains Tax Calculator — no sign-up needed.

Capital Gains Tax Calculator →The Indexation Benefit: What It Was and Why It Matters

Indexation is a mechanism that adjusts the original purchase price of an asset for inflation, using a government-published index called the Cost Inflation Index (CII). By inflating your purchase cost, indexation reduces your taxable gain, which in turn reduces your tax liability.

For example: if you bought a property for ₹40 lakh in FY 2015-16 and sold it for ₹90 lakh in FY 2025-26, the indexed cost of acquisition — using CII values of 254 (FY 2015-16) and 376 (FY 2025-26) — would be approximately ₹59.2 lakh. This means the taxable LTCG would be ₹30.8 lakh instead of ₹50 lakh. That is a significant reduction.

Under the new regime, indexation is no longer available for most assets sold after July 23, 2024. For property bought before that date, you still have the choice between the two methods. For everything else — gold, debt funds, unlisted shares — indexation is gone, and only the flat 12.5% rate applies. The CBDT confirmed that the rate reduction from 20% to 12.5% is meant to compensate, and for many assets sold with high appreciation, the new regime does work out better. But for assets where the gain was modest relative to inflation, the removal of indexation can mean a higher actual tax bill.

Set-Off and Carry Forward of Capital Losses

One of the often-overlooked aspects of capital gains tax planning is the ability to set off losses against gains. The rules are specific:

- Short-term capital losses can be set off against both short-term and long-term capital gains.

- Long-term capital losses can only be set off against long-term capital gains — not against STCG.

- Any unabsorbed losses can be carried forward for up to eight assessment years, provided the ITR is filed on time.

This makes tax-loss harvesting a legitimate and useful strategy, particularly for equity investors towards the end of the financial year. If you have made gains on some stocks, selling underperforming ones to book a loss can reduce your net taxable gain.

Use CalcPhi's Income Tax Calculator to model how capital gains interact with your total taxable income under both the old and new regimes.

Income Tax Calculator →Section 54 and 54EC: How to Save on LTCG from Property

Budget 2024 made no changes to the rollover exemptions available under the Income Tax Act. You can still save on LTCG from the sale of a residential property in two ways:

- Section 54: Reinvest residential property LTCG into another residential property within 2 years (or construct within 3 years) and the gains are exempt up to the reinvestment amount. Maximum exemption: ₹10 crore.

- Section 54EC: Invest LTCG in specified bonds (NHAI or REC bonds) within 6 months of sale. Maximum: ₹50 lakh. Lock-in: 5 years.

These rollover benefits remain intact and continue to be among the most effective legal ways to reduce capital gains tax, particularly for real estate transactions.

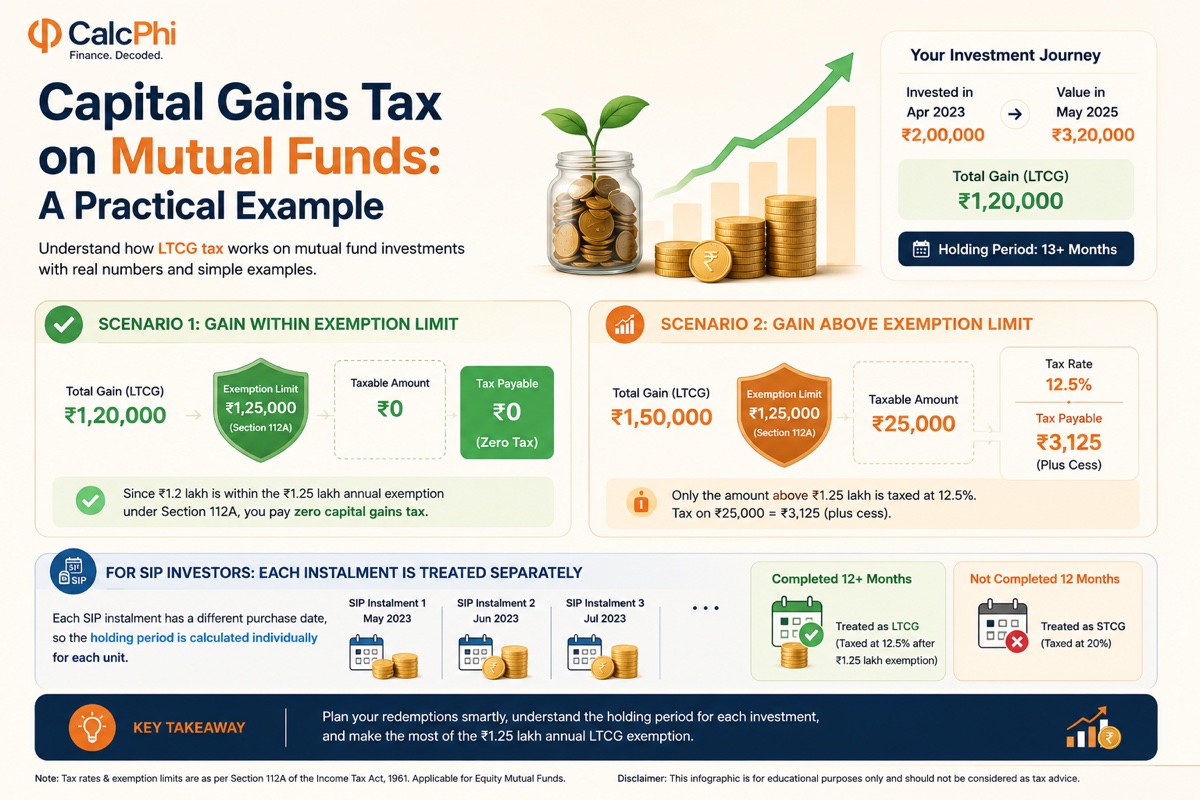

Capital Gains Tax on Mutual Funds: A Practical Example

Say you invested ₹2 lakh in an equity mutual fund in April 2023, and by May 2025 — after more than 12 months — the investment has grown to ₹3.2 lakh. Your total LTCG is ₹1.2 lakh.

Since ₹1.2 lakh is within the ₹1.25 lakh annual exemption under Section 112A, you pay zero capital gains tax on this redemption. If your gain had been ₹1.5 lakh instead, only the amount above ₹1.25 lakh — i.e., ₹25,000 — would be taxed at 12.5%, resulting in a tax of just ₹3,125 (plus cess).

For SIP investors, each instalment is treated as a separate purchase, so the holding period is calculated individually for each unit. Units that complete 12 months are taxed as LTCG; those that have not are taxed as STCG at 20%.

Planning a SIP or thinking about redemptions? Model your returns with CalcPhi's SIP Calculator and pair it with the Capital Gains Tax Calculator to understand your post-tax outcome.

SIP Calculator → Capital Gains Calculator →Summary: Capital Gains Tax Rates at a Glance (FY 2025-26)

| Asset Type | Holding Period | Tax Rate |

|---|---|---|

| Listed equity / equity MF (STT paid) | ≤ 12 months | 20% STCG (Section 111A) |

| Listed equity / equity MF (STT paid) | > 12 months | 12.5% above ₹1.25L (Section 112A) |

| Property, gold, debt MF | ≤ 24 months | Slab rate (STCG) |

| Property, gold, debt MF | > 24 months | 12.5% without indexation (Section 112) |

| Property acquired before 23 Jul 2024 | > 24 months | 12.5% (no indexation) OR 20% (with indexation) — whichever is lower |

Frequently Asked Questions

What is the LTCG tax rate in India for FY 2025-26?

For equity shares and equity mutual funds where STT is paid, LTCG above ₹1.25 lakh is taxed at 12.5% under Section 112A. For all other assets like property, gold, and debt funds, LTCG is taxed at 12.5% without the indexation benefit under Section 112. These rates apply to transfers made on or after July 23, 2024.

What changed in Budget 2024 for capital gains tax?

The Finance (No. 2) Act, 2024, effective from July 23, 2024, made five major changes: the holding period was simplified to just two buckets (12 months and 24 months); STCG on equity was raised from 15% to 20%; LTCG on equity was raised from 10% to 12.5%; the LTCG exemption on equity was raised from ₹1 lakh to ₹1.25 lakh; and indexation was removed for most non-equity assets, with the LTCG rate reduced from 20% to 12.5%.

Is indexation still available for property after Budget 2024?

Indexation was removed for property acquired on or after July 23, 2024. However, for property acquired before that date, resident individuals and HUFs can still choose between 20% with indexation or 12.5% without indexation, whichever results in a lower tax liability.

How are mutual fund gains taxed in 2026?

Equity-oriented mutual funds held for more than 12 months are subject to LTCG tax at 12.5% on gains exceeding ₹1.25 lakh. Gains from units held for 12 months or less are taxed at 20% as STCG. Debt mutual fund gains are taxed at the applicable slab rate for short-term gains, and at 12.5% without indexation for long-term gains (held over 24 months). For SIP investors, each monthly instalment is treated as a separate purchase for the purpose of calculating the holding period.

Can I carry forward capital losses to reduce future tax?

Yes. Short-term capital losses can be set off against both STCG and LTCG. Long-term capital losses can only be set off against LTCG. Unabsorbed losses can be carried forward for up to eight assessment years, but only if your ITR is filed on time. This makes tax-loss harvesting a legitimate and useful strategy for equity investors towards the end of the financial year.

What is the STCG rate for equity funds in India in 2026?

Short-term capital gains on equity mutual funds and listed shares where STT is paid are taxed at 20% under Section 111A. This rate was increased from 15% effective July 23, 2024 as part of the Budget 2024 capital gains rationalisation. For other assets — property, gold, unlisted shares — STCG is added to income and taxed at your applicable slab rate.

Disclaimer: The information in this article is for educational and informational purposes only. Tax rules are subject to change, and individual circumstances vary. All calculators on CalcPhi are estimation tools and do not constitute financial or tax advice. All figures are based on Income Tax Act provisions as amended by the Finance (No. 2) Act, 2024, applicable for AY 2026-27. Please consult a qualified Chartered Accountant or financial advisor before making investment or tax-related decisions.