Best SIP Amount by Salary in India 2026 — A Goal-by-Goal Guide

Most articles on SIP investing give you a percentage and call it done. "Invest 20% of your salary" sounds clean, but it tells you nothing about what that money is actually building, how long you have, or whether you are even on track for the goals that matter to you — a house down payment, your child's college fees, or a retirement corpus large enough to outlast inflation.

This guide does things differently. Yes, it gives you a salary-wise SIP reference table. But it also maps specific monthly SIP amounts to real financial goals — so you know exactly what your ₹10,000 a month is doing and whether you need to be doing more.

Why Your Salary Is the Starting Point, Not the Whole Story

A Systematic Investment Plan, or SIP, is simply a way to invest a fixed amount into a mutual fund every month. The fund manager pools your money with thousands of other investors and deploys it into stocks, bonds, or a mix of both, depending on the fund type. Over time, your money grows through a combination of market returns and compounding — which means your returns also start earning returns.

The reason salary matters is straightforward: you can only invest what you actually take home after deductions. Your CTC (Cost to Company) figure on your offer letter is not what lands in your bank account. After EPF contributions, professional tax, TDS, and other deductions, most employees take home 65–75% of their CTC. A ₹12 LPA package typically translates to roughly ₹75,000–₹82,000 in-hand per month — not ₹1 lakh.

Before you decide your SIP amount, use CalcPhi's CTC to In-Hand Salary Calculator to find your actual monthly take-home. That number is your true starting point.

SIP Amount by Salary — The 2026 Reference Table

The table below uses monthly in-hand salary (not CTC) and applies the commonly recommended 20–30% savings rate. The corpus projections assume 12% CAGR, which is broadly in line with long-term returns from diversified Indian equity mutual funds — though actual returns will vary.

| Monthly In-Hand | Minimum SIP (20%) | Recommended SIP (30%) | Corpus in 15 Years | Corpus in 25 Years |

|---|---|---|---|---|

| ₹20,000 | ₹4,000 | ₹6,000 | ₹20L – ₹30L | ₹76L – ₹1.14 Cr |

| ₹30,000 | ₹6,000 | ₹9,000 | ₹30L – ₹45L | ₹1.14 Cr – ₹1.71 Cr |

| ₹50,000 | ₹10,000 | ₹15,000 | ₹50L – ₹75L | ₹1.90 Cr – ₹2.85 Cr |

| ₹75,000 | ₹15,000 | ₹22,500 | ₹75L – ₹1.13 Cr | ₹2.85 Cr – ₹4.27 Cr |

| ₹1,00,000 | ₹20,000 | ₹30,000 | ₹1.00 Cr – ₹1.51 Cr | ₹3.80 Cr – ₹5.70 Cr |

| ₹1,50,000 | ₹30,000 | ₹45,000 | ₹1.51 Cr – ₹2.26 Cr | ₹5.70 Cr – ₹8.55 Cr |

| ₹2,00,000 | ₹40,000 | ₹60,000 | ₹2.01 Cr – ₹3.01 Cr | ₹7.60 Cr – ₹11.40 Cr |

Projections at 12% CAGR are illustrative only. Use the SIP Calculator to model your exact figures. One important caveat: the 20% rule is a floor, not a ceiling. If you are in your 20s with no home loan, no dependants, and modest rent, you should be aiming for 30–40%. These early years — when your income is growing faster than your obligations — are the highest-leverage period of your financial life.

What "Enough" Actually Looks Like: Goal-Based SIP Planning

The reason a blanket percentage often fails is that different goals require different timelines and different risk profiles. Here is how to think about your SIP in goal-specific terms.

Retirement — The Biggest Goal You Are Probably Underfunding

A 30-year-old who wants to retire at 60 has a 30-year SIP horizon — which is excellent. But the question is: how much corpus do you actually need? A modest retirement in a Tier 2 Indian city in 2026 costs roughly ₹50,000–₹60,000 per month. Accounting for 6% annual inflation, that same lifestyle will cost approximately ₹2.9 lakh per month by 2056. To sustain that withdrawal for 25 years post-retirement, you need a corpus of roughly ₹5–6 crore in today's terms — significantly more in nominal terms.

For a 30-year-old earning ₹75,000 per month, hitting a ₹5 crore retirement corpus requires approximately ₹9,000–₹11,000 per month in SIP at 12% CAGR over 30 years. That is well within the 20% rule — but only if you start now. Waiting 5 years increases the required monthly SIP by nearly 80%. Use CalcPhi's Retirement Corpus Calculator to find your personalised number.

Child's Higher Education — A Deadline You Cannot Miss

If your child is 3 years old today and you want ₹50 lakhs available when they turn 18 (for college fees, which are rising faster than general inflation), you have a 15-year window. At 12% CAGR, you need approximately ₹10,500 per month. At a more conservative 10%, the required SIP rises to around ₹13,500. This is a fixed deadline — unlike retirement, you cannot extend it.

The fund selection matters here too. A 15-year horizon supports an equity-heavy approach for the first 10 years, gradually shifting to hybrid or debt funds in the final 5 years as the deadline approaches.

House Down Payment — A Medium-Term Goal That Needs a Different Fund Type

If you are saving for a 20% down payment on a ₹80 lakh flat in the next 5 years, you need ₹16 lakhs. At 10% CAGR (using hybrid or short-term debt funds — not equity — because a 5-year horizon carries significant equity risk), you need approximately ₹20,000 per month.

This is a case where many investors make a critical mistake: they put short-term savings into equity SIPs chasing higher returns, only to find the market in a downturn exactly when they need the money. Medium-term goals (3–7 years) belong in hybrid or debt-oriented funds, not pure equity.

City-Wise Lens: The Same Salary Goes Very Differently

A ₹60,000 monthly in-hand salary means very different things in Coimbatore versus Mumbai. The investable surplus — and therefore the realistic SIP amount — changes dramatically based on where you live.

In Mumbai or Delhi, rent alone for a 2BHK in a decent neighbourhood can cost ₹25,000–₹40,000, eating up 40–65% of a ₹60,000 salary before groceries, transport, or lifestyle spending. In Pune, Hyderabad, or Bengaluru's outer zones, the same setup might cost ₹15,000–₹22,000. In Tier 2 cities like Jaipur, Lucknow, or Nagpur, ₹12,000–₹15,000 covers comfortable living.

This means someone earning ₹60,000 in Nagpur might realistically invest ₹18,000–₹20,000 per month, while someone earning the same in central Mumbai might struggle to consistently invest more than ₹8,000. Neither person is doing it wrong — they are dealing with different cost structures. The framework is the same: subtract fixed expenses honestly, then direct 70% of the remaining surplus into SIP.

The Tax-Saving SIP You Might Be Missing: ELSS

If you are in the old tax regime and investing in SIP anyway, a portion of your investment can also save you income tax under Section 80C of the Income Tax Act. ELSS — Equity Linked Savings Scheme — is a category of mutual fund that qualifies for up to ₹1.5 lakh in 80C deduction per year. That means if you invest ₹12,500 per month in an ELSS fund, you get the full ₹1.5 lakh deduction, which can save you ₹46,800 in tax if you are in the 30% bracket.

ELSS has the shortest lock-in of any 80C instrument — just 3 years — and has historically delivered returns comparable to diversified equity funds. The tax saving is an additional return on top of the fund's market performance. Use the ELSS Calculator to see how much tax you save alongside your corpus growth.

One note: if you have switched to the new tax regime (which became the default from FY 2024-25), the 80C deduction is not available, making ELSS less distinctively advantageous — though it still operates as a normal equity mutual fund with the 3-year lock-in.

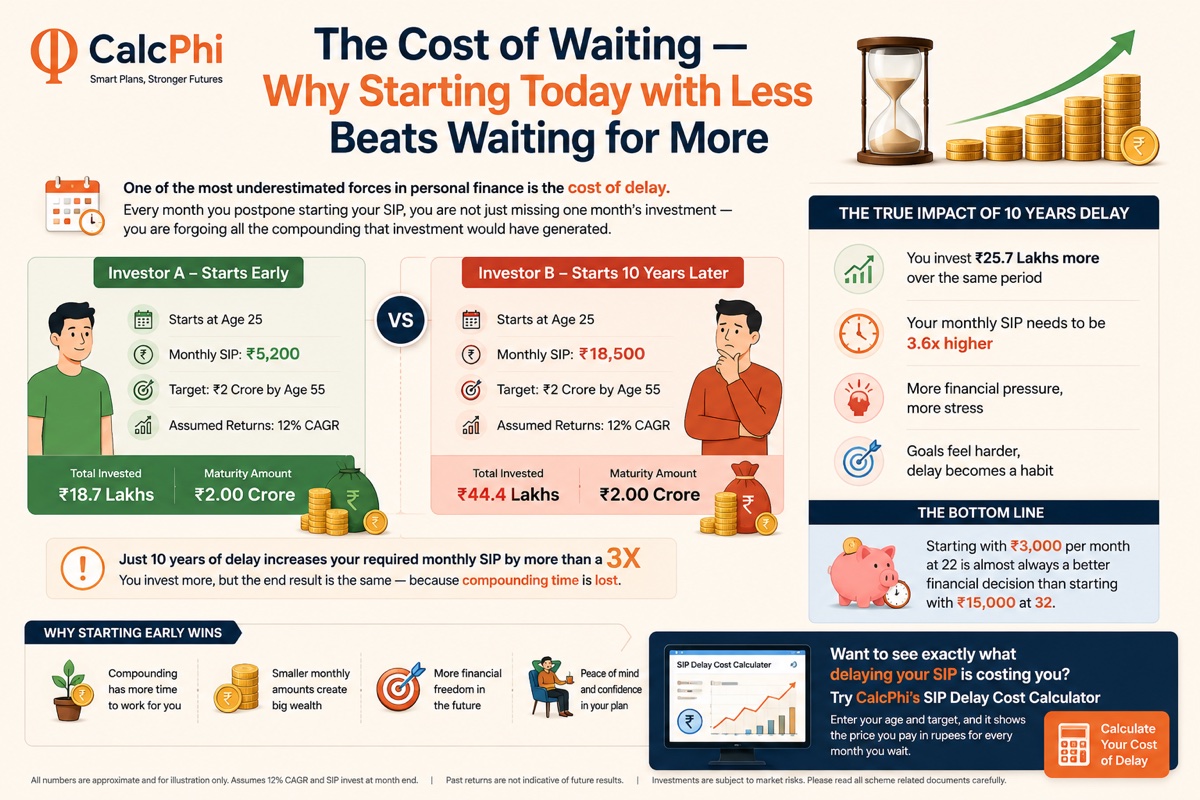

The Cost of Waiting — Why Starting Today with Less Beats Waiting for More

One of the most underestimated forces in personal finance is the cost of delay. Every month you postpone starting your SIP, you are not just missing one month's investment — you are forgoing all the compounding that investment would have generated.

Consider two investors, both targeting ₹2 crore by age 55. Investor A starts a SIP at age 25. At 12% CAGR, they need approximately ₹5,200 per month. Investor B starts at age 35. For the same ₹2 crore target at 55, they now need approximately ₹18,500 per month — more than three times as much — because they lost 10 years of compounding.

The cost of that 10-year delay is not just higher monthly investment. It is also the psychological pressure of needing to invest a much larger sum, which often makes the goal feel out of reach and leads to further delay. Starting with ₹3,000 per month at 22 is almost always a better financial decision than starting with ₹15,000 at 32.

Want to see exactly what delaying your SIP is costing you? Try CalcPhi's SIP Delay Cost Calculator — enter your age and target, and it shows the price you pay in rupees for every month you wait.

How to Actually Increase Your SIP Over Time: The Step-Up Approach

The step-up SIP — also called a top-up SIP — is a feature most mutual fund platforms offer that lets you automatically increase your SIP amount by a fixed percentage each year. A 10% annual step-up aligns your investment growth roughly with salary growth, meaning your SIP absorbs a portion of every increment without requiring active decision-making.

The numbers are compelling. A ₹10,000 SIP with a 10% annual step-up over 20 years at 12% CAGR builds approximately ₹2.30 crore. A flat ₹10,000 SIP with no step-up builds ₹99 lakh over the same period. The step-up investor ends up with 2.3x the corpus despite starting at the same amount, purely because the investment amount grew with income.

Set up a standing instruction on your mutual fund platform to step up your SIP every April — right after your annual increment. Use the Step-Up SIP Calculator to project what your current SIP grows into with a 10% or 15% annual step-up.

Putting It Together: A Practical SIP Allocation Framework

Here is a framework to split your total monthly SIP across multiple goals if you have enough surplus to do so. Start by deciding how much you can consistently invest each month. Then allocate it across goals in order of urgency and timeline.

A sample allocation for someone with ₹20,000 available monthly for investment might look like this: ₹8,000 into a retirement-focused equity fund (long horizon, high equity tilt), ₹6,000 into an ELSS fund that serves both as equity investment and 80C tax saving, ₹4,000 into a balanced hybrid fund for a medium-term goal like a car or renovation, and ₹2,000 into a liquid fund or short-duration fund as a complement to an emergency fund.

This is not a prescription — it is a structure. Your allocations will shift as goals are achieved, as salaries grow, and as life circumstances change. The important principle is that each rupee in your investment portfolio should have a job and a timeline.

Frequently Asked Questions

How much SIP should I do on a ₹25,000 monthly salary?

On ₹25,000 take-home, aim for ₹5,000 per month as your starting SIP — which is the 20% floor. Before pushing this higher, ensure you have built an emergency fund of at least ₹50,000–₹75,000 (three months of expenses). Once the emergency fund is in place, work toward ₹7,500 per month. Even ₹5,000 per month at 25, stepped up 10% annually, builds approximately ₹1.5 crore by age 55 — meaningful wealth on a modest income.

Is 30% of salary too much to invest in SIP?

Not if your expenses allow it. 30% of in-hand salary is a healthy target for anyone in their 20s with no home loan and no dependants. The key is that the remaining 70% must genuinely cover your living costs, emergency reserves, and insurance premiums without creating financial stress. If investing 30% means skipping health insurance or going into credit card debt, dial it back to 20% and build up gradually.

Should I do SIP in one fund or multiple funds?

Two to three funds is the sweet spot for most investors. A single large-cap index fund (tracking the Nifty 50 or Sensex) combined with one flexi-cap or mid-cap fund covers a wide range of the Indian equity market without excessive overlap. Adding a third fund — perhaps an international equity fund for global diversification — makes sense once your SIP exceeds ₹15,000–₹20,000 per month. More than four funds usually adds administrative complexity without meaningfully improving diversification.

What is the minimum SIP amount to start in India in 2026?

Most fund houses allow SIPs starting at ₹100 to ₹500 per month. While these amounts are too small to build significant wealth in isolation, they serve a critical purpose: they build the habit and familiarise you with how mutual fund investing works. Treat ₹500 as a starting point, not a permanent number. Increase it by ₹1,000–₹2,000 every 6 months.

Does SIP give better returns than FD in India?

Over long periods (10 years or more), diversified equity SIPs have historically delivered significantly higher returns than Fixed Deposits. FDs currently offer 6.5–7.5% per annum (taxable), while diversified equity funds have delivered 11–14% CAGR over 15–20 year periods. However, SIPs carry market risk — in any given year or even 3-year period, equity returns can be negative. FDs are guaranteed. For goals more than 7 years away, SIPs have a strong track record of outperforming FDs after tax and inflation.

How do I know if my SIP is on track for retirement?

A simple check: your current SIP corpus plus future contributions at your expected return rate should meet your inflation-adjusted retirement corpus target. The Retirement Corpus Calculator does this math for you — enter your current age, retirement age, monthly expenses, and existing savings, and it shows whether your current SIP is sufficient or how much you need to add.

Disclaimer: All calculations and projections in this article are for educational and estimation purposes only. Past returns of mutual funds are not indicative of future performance. Nothing in this article constitutes financial advice. Please consult a SEBI-registered investment advisor before making investment decisions.