Best Savings Account Interest Rates in India 2026: Which Bank Pays the Most?

Most Indians open a savings account at whichever bank their employer uses for salary credit — SBI, HDFC, ICICI, or Axis. That's convenient, but it's quietly costing you money every single month. These large banks currently offer 2.50% to 3.50% per annum on savings balances, while small finance banks and progressive private banks are paying 6% to 7.50% on the same money. On a ₹3 lakh emergency fund, that difference alone adds up to over ₹14,000 extra per year — without taking a single rupee of investment risk.

In this guide, we break down which banks are paying the most on savings accounts in 2026, what the real after-tax numbers look like, and the smart strategies you can use to make your idle money work harder — all while keeping it fully accessible.

Why Savings Account Interest Rates Vary So Much

Before diving into the numbers, it helps to understand why one bank offers 2.50% while another offers 7%. It is not random.

Large public sector banks like SBI and Bank of Baroda have massive deposit bases built over decades. They do not need to compete aggressively for deposits — people park money there out of habit and trust. Their cost of funds is low, and that low cost is passed on as a low savings rate to depositors.

Small finance banks (SFBs) — institutions like AU Small Finance Bank, Ujjivan SFB, and IDFC FIRST Bank — are a different story. They are RBI-licensed banks, but they are newer and typically cater to underserved segments. To build a deposit base quickly and attract customers, they offer significantly higher savings rates. Crucially, all SFBs are regulated by the Reserve Bank of India and your deposits up to ₹5 lakh per bank are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC). So within that ₹5 lakh limit, the safety profile is comparable to any other scheduled bank.

One more important detail: most banks use a tiered or slab-based interest structure. The headline "up to 7.50%" often applies only to balances above a certain threshold, such as ₹10 lakh or ₹25 lakh. For smaller balances, the effective rate may be lower. We have flagged where this matters in the breakdowns below.

Savings Account Interest Rates: Major Banks in 2026

Here is a consolidated comparison of savings account interest rates as of May 2026. Rates are subject to change — always verify on the bank's official website before switching.

| Bank | Rate (lower slab) | Rate (higher slab) | Category |

|---|---|---|---|

| State Bank of India | 2.50% | 2.50% (flat) | PSB |

| Bank of Baroda | 2.75% | 2.75% (flat) | PSB |

| HDFC Bank | 3.00% | 3.50% (above ₹50L) | Private |

| ICICI Bank | 3.00% | 3.50% (above ₹50L) | Private |

| Axis Bank | 2.50% | 3.50% (higher tiers) | Private |

| Kotak Mahindra Bank | 3.50% | 4.00% (above ₹50L) | Private |

| IndusInd Bank | 4.00% | 5.00% (higher balances) | Private |

| RBL Bank | 4.75% | 6.00% (above threshold) | Private |

| IDFC FIRST Bank | 3.00% | 6.50% (above ₹3L) | Private |

| AU Small Finance Bank | 3.50% | 6.75% (above ₹1L) | SFB |

| Ujjivan Small Finance Bank | 4.00% | 7.10% (above ₹10L) | SFB |

| ESAF Small Finance Bank | 6.00% | 7.00% (higher slab) | SFB |

| Fi Money (Federal Bank) | 3.00% | 6.00% (higher balances) | Digital |

| Jupiter (Federal Bank) | 3.50% | 6.00% (higher balances) | Digital |

The Real Numbers: What You Earn on ₹3 Lakh

Let us put actual rupees to the rate differences. Suppose you hold ₹3 lakh as your emergency fund.

At SBI's 2.50%, you earn ₹7,500 per year in gross interest. After factoring in the Section 80TTA deduction (₹10,000 of savings account interest is exempt from tax for individuals below 60), most of this falls within the exemption window.

At HDFC Bank's 3.50%, you earn ₹10,500 gross. At IDFC FIRST Bank's 6.50%, you earn ₹19,500 gross. At AU Small Finance Bank's 6.75%, you earn ₹20,250 gross.

The difference between SBI and AU SFB on this single account is ₹12,750 per year. Over five years at the same rates, that gap grows to over ₹63,000 — with zero investment risk and full liquidity.

| Bank | Rate | Annual Interest | 5-Year Total |

|---|---|---|---|

| SBI | 2.50% | ₹7,500 | ₹37,500 |

| HDFC Bank | 3.50% | ₹10,500 | ₹52,500 |

| IDFC FIRST Bank | 6.50% | ₹19,500 | ₹97,500 |

| AU Small Finance Bank | 6.75% | ₹20,250 | ₹1,01,250 |

Want to see exactly what your savings account balance earns at current rates? Use CalcPhi's free Savings Account Calculator to model your balance at any interest rate and get the annual interest figure in seconds — no sign-up needed.

How Savings Account Interest Is Taxed in India

Understanding the tax treatment is essential before you decide where to park money. Savings account interest in India is taxable as income from other sources and is added to your total income and taxed at your applicable slab rate.

However, there is a meaningful relief. Under Section 80TTA of the Income Tax Act, individuals below 60 years of age can deduct up to ₹10,000 of savings account interest per financial year. This exemption covers interest from savings accounts held at banks, cooperative banks, and post offices — but not from fixed deposits or recurring deposits.

Senior citizens (aged 60 and above) get an even better deal under Section 80TTB. They can claim a deduction of up to ₹50,000 per year on interest from any bank deposit — including savings accounts, FDs, and RDs — making the net return on savings deposits significantly more attractive for retirees.

For most salaried individuals in the 20% or 30% tax bracket, a portion of savings interest above ₹10,000 will be taxable. At a 7% rate on ₹3 lakh, you earn ₹21,000 in interest. After the ₹10,000 exemption, ₹11,000 is taxable. At the 20% slab, the tax on that excess is ₹2,200 — still leaving you with substantially more than what SBI pays gross.

Note that TDS is generally not deducted on savings account interest the way it is on FD interest. The responsibility to declare it in your ITR lies with you. If you are unsure how this affects your tax liability, use CalcPhi's Income Tax Calculator to estimate your overall tax for FY 2026-27 including other sources of income.

The Sweep-In FD Strategy: Best of Both Worlds

If you are not ready to switch banks but want to earn more than the standard savings rate, the sweep-in FD is one of the most underused features in Indian banking.

Here is how it works. You set a threshold — say ₹25,000 — and any amount above that in your savings account is automatically "swept" into a short-term fixed deposit, typically for 1–3 months, earning FD rates (currently 6.50–7.50% from most banks). When you need the money, the FD is liquidated and swept back into your savings account without penalty. The funds are available almost like a regular savings balance.

For anyone who consistently holds more than ₹25,000–₹50,000 in their savings account as a buffer, enabling sweep-in FD can effectively double or triple the interest you earn on those idle funds. Check whether your current bank supports this feature — most large banks including HDFC, ICICI, and SBI do. You can calculate the FD component of your return using CalcPhi's FD Calculator to model different tenure and rate combinations.

Should You Split Your Emergency Fund Across Multiple Accounts?

The DICGC insurance limit is ₹5 lakh per depositor per bank. If your total emergency fund is under ₹5 lakh and you hold it at one bank, you are fully covered. If you hold ₹8–10 lakh as an emergency corpus (not unusual for a family with a high monthly expense base), splitting across two banks makes sense — both to maximise interest and to stay within the insurance window.

A common approach is to maintain your primary salary account at a large PSB or established private bank for day-to-day convenience, ATM access, and eligibility for home or car loans, while keeping a separate high-yield savings account at an SFB or IDFC FIRST Bank for your emergency fund and short-term parking money. Two accounts, both DICGC-protected, no conflict between them.

When a Savings Account Is Not Enough: Alternatives for Short-Term Parking

For money you do not need immediately but will need within 6–12 months, a savings account may not always be the optimal vehicle.

A fixed deposit locks your money for a defined period — 7 days to 10 years — but typically earns 6.50–7.50% from most banks. The trade-off is liquidity: premature withdrawal attracts a penalty of 0.50–1%. If your timeline is well-defined, an FD often outperforms even the best savings account rates. Use CalcPhi's FD Calculator to compare maturity values across banks and tenures.

A recurring deposit (RD) is suitable for disciplined monthly savers who want to earn FD-like returns while depositing a fixed amount every month. Current RD rates are broadly in line with FD rates from the same bank. CalcPhi's RD Calculator lets you model the maturity value based on your monthly deposit amount and tenure.

Liquid mutual funds are worth considering for money you plan to hold for more than a month. These funds invest in short-term government securities and corporate debt instruments and have historically delivered 6–7% per annum post-expense. They are not guaranteed like bank deposits, but they are generally low-risk and can be redeemed within 24 hours on business days. For emergency funds beyond 3 months' expenses, many financial planners recommend splitting between a high-yield savings account (for immediate access) and a liquid fund (for the rest).

What to Look for Beyond the Interest Rate

When choosing a high-yield savings account, the interest rate is important — but it is not the only thing that matters.

Minimum balance requirements can vary significantly. Some accounts require a minimum average monthly balance of ₹10,000 to ₹25,000, with penalty charges for falling short. If your salary lands and is spent by the 25th, you may end up paying non-maintenance charges that wipe out any rate advantage.

Interest crediting frequency matters for compounding. Monthly interest crediting (as offered by AU SFB and IDFC FIRST Bank) means your balance compounds faster than quarterly crediting. On a ₹5 lakh balance, the difference over a year is modest but real.

Check the slab structure carefully before switching. The headline rate may apply only to balances above ₹10 lakh or higher. If your balance is ₹2 lakh, the effective rate on your money at a bank advertising 7% may actually be 5% or lower on that slab.

Digital banking quality also matters. If the mobile app is clunky or the UPI transaction limits are low, the operational friction of managing money at a less-mainstream bank may not be worth the rate difference — especially for your primary account.

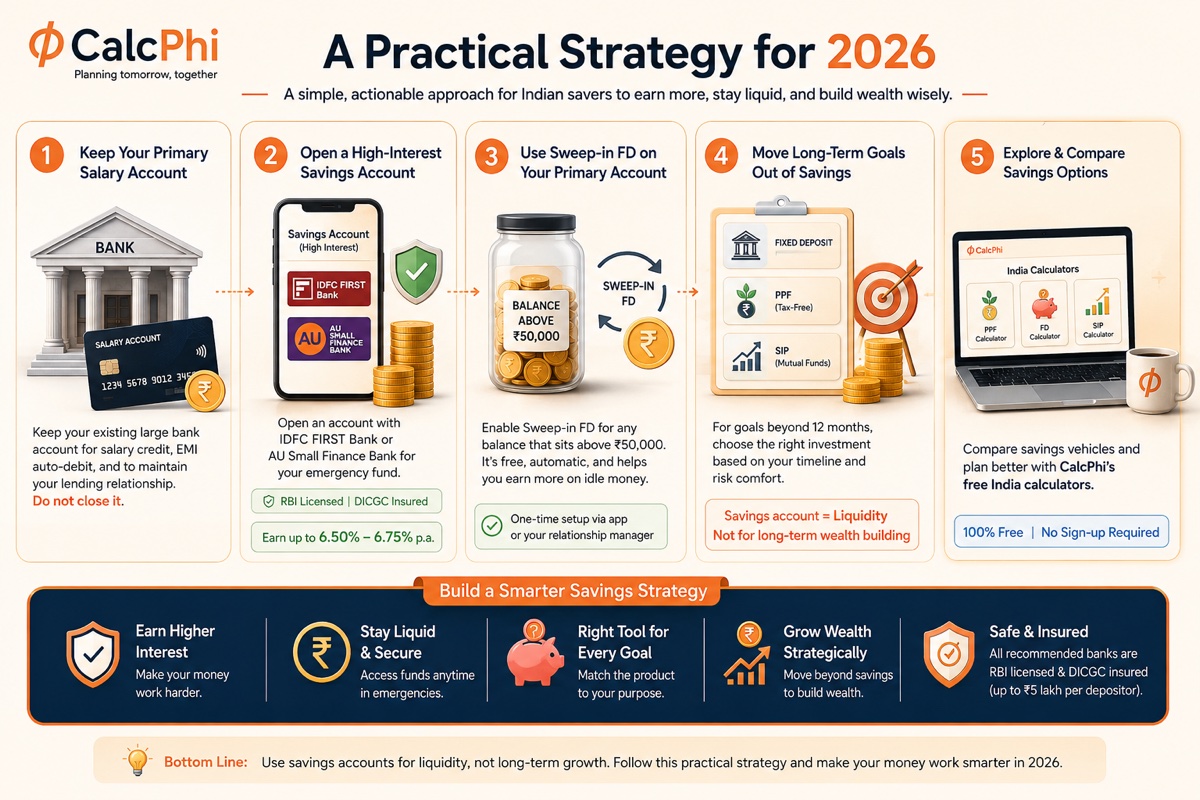

A Practical Strategy for 2026

Based on current rates and the considerations above, here is a simple, actionable approach most Indian savers can implement today.

Keep your primary salary account at your existing large bank. Do not close it — you need it for EMI auto-debit, salary credit, and to maintain a lending relationship.

Open a separate savings account at IDFC FIRST Bank or AU Small Finance Bank for your emergency fund. Both are RBI-licensed, DICGC-insured, and offer strong digital banking. Park 3–6 months of your monthly expenses here and let it earn 6.50–6.75%.

Enable sweep-in FD on your primary account for any balance that consistently sits above ₹50,000. This is free and takes one instruction to your bank's relationship manager or can be set up in the app.

For any savings goal beyond 12 months, move money out of savings accounts entirely and into a fixed deposit, PPF, or SIP — depending on the timeline and your risk comfort. A savings account is the right place for liquid emergency funds, not for long-term wealth building.

Explore how different savings vehicles stack up by visiting CalcPhi's India calculators — from the PPF Calculator for long-term tax-free returns to the FD Calculator for fixed-income comparisons, all the tools you need are free and require no sign-up.

Frequently Asked Questions

Which bank gives the highest savings account interest rate in India in 2026?

Small finance banks currently offer the highest rates. Ujjivan Small Finance Bank offers up to 7.10% on certain high balance slabs, while AU Small Finance Bank offers up to 6.75% and IDFC FIRST Bank offers up to 6.50% on balances above ₹3 lakh. These are RBI-regulated banks and deposits up to ₹5 lakh are DICGC-insured, which means the safety level is broadly equivalent to a large private or public sector bank within that limit.

Is savings account interest taxable in India?

Yes. Savings account interest is added to your total income and taxed at your applicable slab rate. However, individuals below 60 can deduct up to ₹10,000 per year under Section 80TTA, and senior citizens can deduct up to ₹50,000 per year under Section 80TTB (covering all bank deposit interest). TDS is not typically deducted on savings account interest, so you must self-declare it when filing your ITR.

Is it safe to keep money in a small finance bank?

Yes, within limits. All small finance banks in India are licensed and regulated by the Reserve Bank of India. Deposits of up to ₹5 lakh per depositor per bank are insured by DICGC — the same guarantee that applies to SBI, HDFC, and ICICI. For amounts above ₹5 lakh, concentration risk exists, which is why splitting large sums across multiple banks is advisable.

Can I have savings accounts in more than one bank?

Yes, there is no restriction under Indian banking regulations on the number of savings accounts a person can hold. Many financially aware individuals maintain a primary salary account at a large bank for day-to-day use and a separate high-yield account at a small finance bank or IDFC FIRST Bank to earn higher interest on their emergency fund.

What is a sweep-in FD and how does it help?

A sweep-in FD is a feature where any balance in your savings account above a set threshold is automatically transferred into a short-term fixed deposit, earning FD rates instead of savings account rates. When you spend money and the balance falls below the threshold, the FD is partially liquidated to restore the balance. It lets you earn higher returns without compromising liquidity, and is available at most large banks including HDFC, ICICI, and SBI.

How often is savings account interest credited in India?

Most banks credit savings account interest quarterly, but some — including AU Small Finance Bank and IDFC FIRST Bank — credit it monthly. Monthly crediting is slightly better for the depositor because the interest is added to the principal more frequently, which compounds the balance slightly faster over time.

Disclaimer: The interest rates, tax rules, and bank-specific details in this article are based on publicly available information as of May 2026 and are subject to change without notice. CalcPhi calculators are for educational and estimation purposes only. Nothing in this article constitutes financial advice. Please verify current rates directly with the bank before making any financial decision, and consult a SEBI-registered financial advisor or qualified CA for personalised guidance.