Home Loan Balance Transfer in India 2026: When It's Worth It and When to Skip

Your current lender has you locked in at 9.25%. A competing bank flashes an 8.5% offer and suddenly a home loan balance transfer feels like a no-brainer. A 0.75% rate cut on a ₹50 lakh loan sounds like serious money left on the table. But here's what most people don't calculate upfront: processing fees, MOD charges, legal verification costs, MODT stamp duty, and the administrative effort of switching lenders. Depending on your outstanding loan and remaining tenure, these switching costs can wipe out one to three years of EMI savings — or more. This guide does the full math.

What Is a Home Loan Balance Transfer?

A home loan balance transfer — sometimes called a home loan refinance — is the process of moving your existing home loan from one lender to another, typically to take advantage of a lower interest rate. The new lender pays off your outstanding principal to the old lender, and you now owe the new lender the same amount at a lower rate. The loan amount does not change. The property being mortgaged does not change. What changes is who you are paying, at what interest rate, and what your monthly EMI and total interest outgo look like.

How the Break-Even Calculation Works

Before any decision, one number matters most: the break-even period — how many months it takes for your monthly EMI savings to recover the upfront cost of switching.

Break-Even (months) = Total Switching Cost ÷ Monthly EMI Saving

If your remaining loan tenure exceeds the break-even period by a comfortable margin, the transfer is worth it. If your tenure is close to the break-even point, you are barely breaking even and may not benefit.

A Real-World Example: ₹50 Lakh Outstanding, 15 Years Remaining

You have ₹50 lakh outstanding with 15 years (180 months) left. Your current rate is 9.25% and a new lender is offering 8.5%.

| Parameter | Current Loan | After Balance Transfer |

|---|---|---|

| Outstanding Principal | ₹50,00,000 | ₹50,00,000 |

| Interest Rate | 9.25% p.a. | 8.5% p.a. |

| Remaining Tenure | 180 months | 180 months |

| Monthly EMI | ₹51,357 | ₹49,213 |

| Monthly Saving | ₹2,144/month | |

| Total Interest Saving (15 years) | ₹3,85,920 | |

Now factor in typical switching costs:

| Switching Cost Component | Typical Range |

|---|---|

| Processing Fee (new lender, 0.25–0.5%) | ₹12,500 – ₹25,000 |

| MOD / MODT Registration Charges | ₹10,000 – ₹20,000 |

| Legal and Technical Verification | ₹5,000 – ₹10,000 |

| Stamp Duty on New Mortgage | ₹5,000 – ₹15,000 |

| Miscellaneous (notary, courier, etc.) | ₹2,000 – ₹5,000 |

| Total Switching Cost | ₹34,500 – ₹75,000 |

| Break-even at ₹2,144/month saving | 16 – 35 months (1.5 – 3 years) |

With 15 years remaining, a break-even of 1.5 to 3 years is easily justified. You save nearly ₹3.86 lakh over the full tenure against an upfront cost of ₹35,000–₹75,000.

Use CalcPhi's free Balance Transfer Calculator — enter your outstanding principal, current rate, new rate, and remaining tenure to instantly see your break-even period and total interest saved.

Balance Transfer Calculator →When a Home Loan Balance Transfer Is Worth It

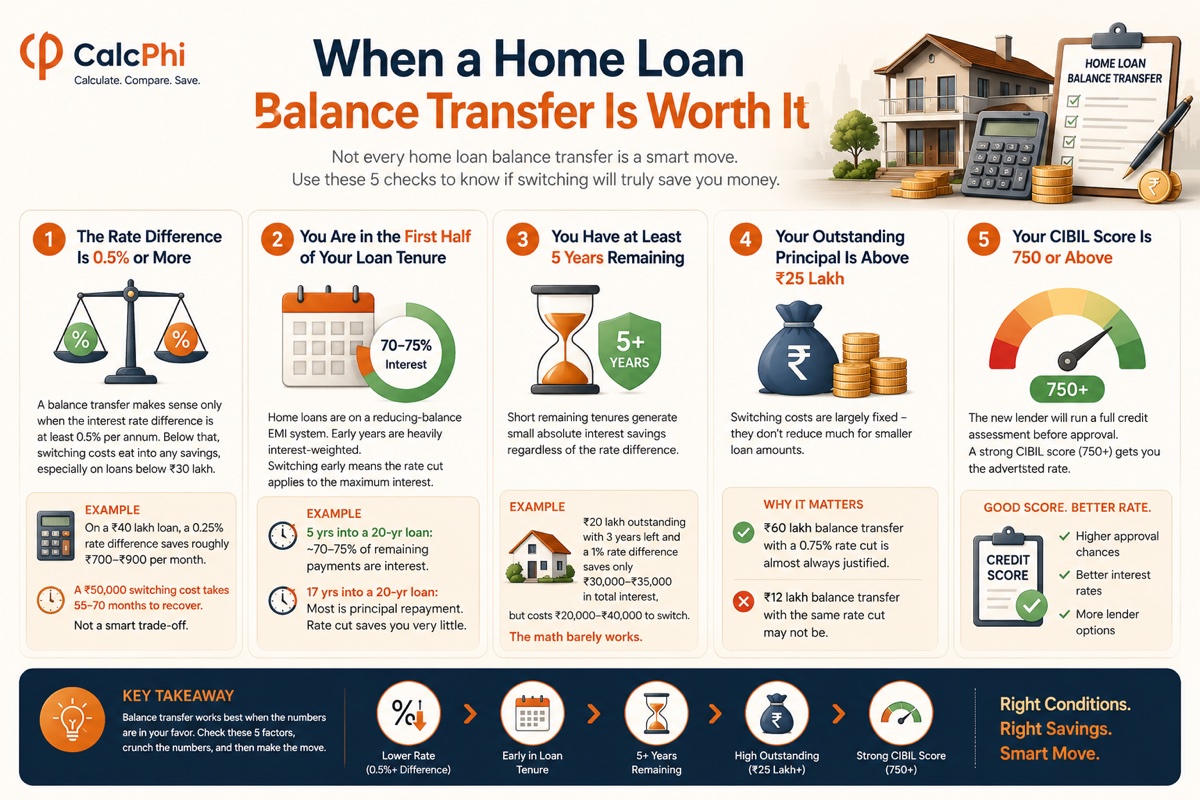

The Rate Difference Is 0.5% or More

A balance transfer makes financial sense only when the interest rate difference is at least 0.5% per annum. Below that threshold, the switching costs almost always eat into any savings — especially on loan amounts below ₹30 lakh. On a ₹40 lakh loan, a 0.25% rate difference saves roughly ₹700–₹900 per month, which means a ₹50,000 switching cost takes 55–70 months to recover. That is not a smart trade-off.

You Are in the First Half of Your Loan Tenure

Home loans in India are structured on a reducing-balance EMI system. The early years of your loan are heavily interest-weighted — if you are 5 years into a 20-year loan, roughly 70–75% of your remaining payments are still interest. Switching at this stage means the rate cut applies to the maximum possible interest amount. If you are 17 years into a 20-year loan, most of what's left is principal repayment. The interest component is tiny, and a rate cut saves you very little.

You Have at Least 5 Years Remaining

Short remaining tenures generate small absolute interest savings regardless of the rate difference. A ₹20 lakh outstanding with 3 years left and a 1% rate difference saves you roughly ₹30,000–₹35,000 in total interest, but costs ₹20,000–₹40,000 to switch. The math barely works.

Your Outstanding Principal Is Above ₹25 Lakh

Switching costs are largely fixed — they do not scale down much just because your loan amount is smaller. Legal fees, MOD charges, and MODT stamp duties are roughly the same whether you are transferring ₹15 lakh or ₹60 lakh. This means the switching cost as a percentage of savings is much higher for smaller loans. A ₹60 lakh balance transfer with a 0.75% rate cut is almost always justified. A ₹12 lakh balance transfer with the same rate cut may not be.

Your CIBIL Score Is 750 or Above

The new lender will run a full credit assessment before approving your balance transfer. If your credit score has dipped below 750 since you took your original loan, the new lender may offer you a rate that is only marginally better, or decline altogether. A strong CIBIL score (750+) is what actually gets you the advertised rate — check your score before applying.

When to Skip the Balance Transfer

Your Remaining Tenure Is Under 5 Years

If you have fewer than 60 months left on your loan, the total interest you will pay — even at your current rate — is limited. A rate reduction saves you proportionally less, and the switching costs are disproportionately high relative to the saving.

The Rate Difference Is Under 0.5%

A 0.25% rate cut on ₹40 lakh outstanding saves roughly ₹700–₹900/month. To recover ₹40,000 in switching costs, you would need nearly 45–57 months of savings. You have to stay in the new loan for almost 5 years just to break even — and that assumes no early foreclosure or resale of the property.

You Are Planning to Sell the Property Within 3 Years

If there is a reasonable chance you will sell the property in the next 2–3 years, a balance transfer almost certainly does not make sense. You will not be in the loan long enough to recover the switching cost. You may also have to deal with foreclosure charges on the new loan, adding another layer of cost.

Your Existing Lender Has No Foreclosure Penalty

RBI guidelines prohibit banks from charging foreclosure penalties on floating-rate home loans. If you can prepay your current loan aggressively using bonus income or savings instead of switching, you might save more than a balance transfer would — without any of the paperwork or switching costs.

The Negotiation Step Most Borrowers Skip

Before you spend weeks gathering documents and comparing lenders, try something much simpler first: call your existing lender and ask for a rate reduction. This is called a "rate reset" or "repricing request," and many banks — especially public sector banks — will honour it to retain a long-tenure customer with a clean repayment record. You will not get the full new-customer rate, but a 0.25% to 0.40% reduction with zero paperwork is often achievable.

If your lender reduces your rate even partially, recalculate whether the remaining gap still justifies a full balance transfer. Often it will not, and you have saved yourself considerable effort at no cost.

The Full Cost Breakdown: What You'll Actually Pay to Switch

- Processing Fee: The new lender charges this for evaluating and approving your transfer application. Typically 0.25% to 0.5% of the outstanding loan amount, subject to a maximum cap. Some lenders waive this during promotional periods — ask explicitly before assuming.

- MOD (Memorandum of Deposit) Charges: When your property documents move from your old lender to the new one, the new lender registers a fresh mortgage. This registration attracts stamp duty and notary fees, which vary by state. In Maharashtra, MODT stamp duty is 0.1% of the loan amount capped at ₹10 lakh. In Delhi, it is around ₹100 flat.

- Legal and Technical Verification Fees: The new lender will send its lawyer to verify your property documents and a technical expert to re-assess the property. This costs ₹5,000 to ₹10,000 typically and cannot be waived.

- NOC and Document Retrieval from Existing Lender: Your current lender must issue a No Objection Certificate (NOC) and hand over your original property documents. Some lenders charge a small administrative fee for this. Delays in getting the NOC are the most common source of frustration in the transfer process.

Use CalcPhi's Home Loan EMI Calculator to compare your current EMI against what your EMI would be at the new lender's rate — plug in both rates to instantly see the monthly difference.

Home Loan EMI Calculator →Tax Implications of a Home Loan Balance Transfer

A home loan balance transfer does not affect your income tax benefits. Under Section 24(b) of the Income Tax Act, you can still claim up to ₹2 lakh per year on home loan interest paid — regardless of which lender the loan sits with. Under Section 80C, your principal repayment (up to ₹1.5 lakh per year) continues to be deductible under the old tax regime.

The only thing that changes is who issues your interest certificate at year-end. You will likely have two certificates for the financial year in which the transfer happens — one from the old lender and one from the new lender. Make sure both are reflected correctly when filing your ITR.

Use CalcPhi's Home Loan Tax Benefit Calculator to estimate your Section 24(b) and 80C savings before and after the transfer.

Home Loan Tax Benefit Calculator →A Step-by-Step Balance Transfer Checklist

- Get the exact outstanding balance and foreclosure statement from your current lender. This is the number the new lender will base everything on.

- Apply to the new lender. Submit identity proof, income documents (salary slips or ITR), bank statements, property documents, and the foreclosure statement.

- New lender completes legal and technical verification. This takes 7–15 working days typically.

- New lender issues sanction letter. Review it carefully — confirm the interest rate, processing fee, and any special conditions.

- New lender pays off old lender via demand draft or RTGS transfer for the outstanding amount.

- Old lender releases property documents and issues NOC. This can take 2–4 weeks and is often the slowest step.

- New mortgage registration. The MODT is registered with the sub-registrar's office in your property's jurisdiction.

- New EMI begins. Your ECS mandate is updated and you start paying the new lender from the following month.

The full process typically takes 3 to 6 weeks.

Frequently Asked Questions

Does a home loan balance transfer affect my CIBIL score?

A balance transfer involves two credit events: closure of your old loan and opening of a new one. The new loan application triggers a hard inquiry, which causes a small, temporary dip in your score — typically 5 to 15 points. However, the old loan closure appears as "Settled — Paid in Full," which is positive. Most borrowers see their CIBIL score return to its previous level within 3 to 6 months. The net long-term impact is generally neutral to slightly positive.

Can I get a top-up loan along with a balance transfer?

Yes, most lenders allow a top-up loan over and above the balance transfer amount. The eligible top-up depends on your current property value and LTV (Loan-to-Value) ratio — typically up to 75–80% of the property's current market value, minus your outstanding principal. Top-up loans are useful for home renovation or any other purpose and typically carry the same or slightly higher rate than your home loan.

What is the minimum rate difference that justifies a balance transfer?

Industry practice suggests a minimum of 0.5% difference to justify the switch, but this also depends on your outstanding loan amount and remaining tenure. On a large loan (₹60–₹80 lakh) with many years remaining, even 0.4% may be worth it. On a smaller loan with fewer years left, you may need 0.75% or more to make the math work. Use CalcPhi's Balance Transfer Calculator to know your specific break-even.

Can my existing lender refuse to give a NOC?

No. Under RBI guidelines, your existing lender cannot refuse to issue a NOC or obstruct a balance transfer. They must provide the NOC and release original property documents once the outstanding amount is paid off. However, they can — and often do — delay the process. If delays persist beyond 30 days, you can escalate to the Banking Ombudsman.

Are balance transfers on fixed-rate home loans possible?

Yes, but fixed-rate home loans may come with a foreclosure or prepayment penalty — typically 2–4% of the outstanding amount — which significantly changes the cost calculation. RBI's ban on foreclosure penalties applies only to floating-rate home loans. If your loan is on a fixed rate, check your loan agreement carefully before initiating a transfer.

How many times can I transfer my home loan?

There is no regulatory limit on how many times you can transfer your home loan. Practically, however, doing it more than once every few years is rarely worth it — each transfer involves switching costs, documentation, and time. Some lenders may also look less favourably at applications from borrowers who have transferred loans multiple times.

Disclaimer: The figures, calculations, and examples in this article are for educational and estimation purposes only. Interest rates, fees, and regulatory guidelines are subject to change and vary by lender. Nothing in this article constitutes personalised financial advice. Always verify current rates directly with lenders and consult a qualified financial advisor or mortgage specialist before making any borrowing decision.