Advance Tax in India 2026: Who Needs to Pay, When, and How to Calculate

Most salaried employees go through an entire financial year without ever thinking about advance tax. Their employer deducts TDS every month, the tax gets deposited with the government automatically, and by March the obligation is mostly settled. But the moment you earn even one rupee outside your salary — freelance income, rental income, capital gains, dividend income, or business profits — the advance tax rules kick in. Ignore them, and you face interest penalties under Sections 234B and 234C that silently inflate your tax bill.

This guide covers everything you need to know about advance tax for FY 2026-27: who must pay, the four due dates, how to calculate your liability step by step, the penalty rules, and how to pay online via Challan 280.

What Is Advance Tax and Why Does It Exist?

Advance tax is exactly what the name suggests — tax paid in advance, before the financial year ends, rather than in one lump sum at the time of filing your Income Tax Return (ITR). The Income Tax Act, 1961 requires taxpayers with a significant tax liability to spread their payments across four instalments through the year.

The government cannot wait until July of the following year to collect taxes on income earned between April and March. By collecting in instalments, the government ensures a steady cash flow, and taxpayers avoid the shock of a large one-time payment.

If your total tax liability for the year — after accounting for all TDS deductions — exceeds ₹10,000, advance tax applies to you. It is not about your total income crossing ₹10,000. It is about your net tax payable after TDS credits crossing ₹10,000.

Who Must Pay Advance Tax in FY 2026-27?

Individuals who must pay advance tax include salaried employees with any additional income source — rental income, capital gains from selling shares or mutual funds, freelance or consulting income, dividend income exceeding ₹5,000 in a year, or FD interest not fully covered by Form 15G/15H. Self-employed professionals (doctors, lawyers, architects, CAs), business owners, traders, and anyone with F&O (Futures and Options) income must also pay.

Who is exempt? Senior citizens aged 60 years or above who do not have any income from a business or profession are fully exempt. They can settle their entire tax liability as self-assessment tax when filing their ITR without attracting any interest under Section 234B or 234C — a significant relief that is often overlooked.

If you are a salaried employee with no income other than salary and your employer is correctly deducting TDS every month, you likely have no advance tax obligation. The key question is always: after all TDS credits, is there still more than ₹10,000 in tax left to pay?

Advance Tax Due Dates for FY 2026-27

| Instalment | Due Date | Cumulative % of Total Tax |

|---|---|---|

| 1st instalment | 15 June 2026 | At least 15% |

| 2nd instalment | 15 September 2026 | At least 45% |

| 3rd instalment | 15 December 2026 | At least 75% |

| 4th instalment | 15 March 2027 | 100% |

Taxpayers opting for presumptive taxation under Section 44AD (small businesses, turnover up to ₹3 crore) or Section 44ADA (professionals, gross receipts up to ₹75 lakh) are not required to pay in four instalments. They can pay their entire advance tax liability in a single payment by 15 March 2027 without any 234C interest penalty for skipping earlier instalments.

How to Calculate Your Advance Tax — Step by Step

Step 1 — Estimate your total income from all sources. Add salary (gross, before TDS), rental income (after 30% standard deduction), capital gains from equity or property, freelance income, FD/savings interest, and dividend income.

Step 2 — Calculate your gross tax liability. Apply the applicable slab rates to your estimated total income. For FY 2026-27, the new tax regime is the default. Under it, income up to ₹3 lakh is nil; ₹3–7 lakh at 5%; ₹7–10 lakh at 10%; ₹10–12 lakh at 15%; ₹12–15 lakh at 20%; above ₹15 lakh at 30%. The Section 87A rebate makes income up to ₹12 lakh effectively tax-free under the new regime. Add 4% Health and Education Cess on the tax amount. Use CalcPhi's Income Tax Calculator to get your exact figure under both regimes in seconds.

Step 3 — Subtract TDS already deducted. Deduct employer TDS from salary, TDS on FD interest, TDS on rent received, and any other TDS credits verifiable in your Form 26AS or AIS.

Step 4 — Check the threshold. If the remaining liability after TDS credits exceeds ₹10,000, you must pay advance tax.

Step 5 — Divide into instalments. Pay 15% by June 15, a cumulative 45% by September 15, 75% by December 15, and 100% by March 15.

A Practical Example

Rahul is a software engineer earning ₹20 lakh annually from his employer (employer TDS: ₹1.8 lakh already deducted). He also earns ₹2.4 lakh per year from a rented flat, and realised ₹1.5 lakh in long-term capital gains from mutual funds in July.

His estimated total income is approximately ₹23.9 lakh (₹20L salary + ₹1.68L net rental after 30% deduction + ₹1.5L LTCG + adjustments). Under the new regime, his gross tax comes to approximately ₹3.9 lakh; adding 4% cess brings it to roughly ₹4.06 lakh. After crediting the employer TDS of ₹1.8 lakh, his net liability is about ₹2.26 lakh — comfortably above the ₹10,000 threshold.

Rahul must pay: ₹33,900 by June 15 (15%); ₹1,01,700 cumulative by September 15 (45%); ₹1,69,500 cumulative by December 15 (75%); and the balance by March 15, 2027. Use CalcPhi's free Advance Tax Calculator to generate your own instalment schedule instantly.

Advance Tax on Capital Gains — A Special Case

Capital gains require extra attention because they are event-driven income — you cannot always predict when you will sell an asset. The Income Tax rules account for this with a quarter-wise attribution rule:

- Capital gains arising before June 15: include in the first instalment estimate.

- Gains arising between June 16 and September 15: include in the September instalment.

- Gains arising between September 16 and December 15: include in the December instalment.

- Gains arising between December 16 and March 15: can be included fully in the March 15 payment without Section 234C interest on the prior instalments.

If you realise large capital gains late in the financial year (say in February), you will not be penalised for not having included them in the June or September instalments, as long as you cover them in the March payment. Use CalcPhi's Capital Gains Tax Calculator to calculate the exact STCG or LTCG tax before arriving at your advance tax figure.

Penalties for Missing Advance Tax: Sections 234B and 234C

Section 234C — Instalment default: If you pay less than the required cumulative percentage by a due date, you are charged simple interest at 1% per month (or part of a month) on the shortfall, calculated for 3 months per instalment. For the final March instalment, interest is charged for 1 month on the shortfall.

Section 234B — Overall default: If you have paid less than 90% of your total tax liability by 31 March, Section 234B applies. Interest is charged at 1% per month from April 1 until you actually pay the tax — whether at the time of filing your ITR in July or later.

On a ₹2 lakh shortfall, Section 234B interest running for 4 months comes to ₹8,000. Not ruinous — but entirely avoidable with timely payments. Both interest charges are not tax-deductible and do not reduce your tax liability; they are a pure cost of delay.

New vs Old Tax Regime: Does It Affect Your Advance Tax Calculation?

Yes — the regime you choose directly affects your advance tax calculation because the two regimes produce different tax liabilities on the same income. Under the old regime, you can claim deductions like 80C (up to ₹1.5 lakh), 80D (health insurance premiums), HRA exemption, LTA, and home loan interest under Section 24B — these reduce your taxable income and therefore your advance tax.

Under the new regime (the default for FY 2026-27), most deductions are not available, but slab rates are lower and the ₹75,000 standard deduction applies to salaried employees. The Section 87A rebate makes income up to ₹12 lakh effectively tax-free.

The regime that results in a lower tax liability should logically be chosen, and your advance tax instalments must be calculated based on that choice. Use CalcPhi's New vs Old Tax Regime Calculator for a side-by-side comparison at your income level.

How to Pay Advance Tax Online — Challan 280

Go to the Income Tax e-filing portal at incometax.gov.in and log in with your PAN. Navigate to e-Pay Tax → New Payment and select Challan 280. Under "Type of Assessment," select Income Tax (other than companies). For Assessment Year, select AY 2027-28 — this corresponds to FY 2026-27. Under "Type of Payment," choose 100 — Advance Tax.

Enter the tax amount and pay via net banking, UPI, debit card, or RTGS/NEFT. Once confirmed, download and save the challan receipt. The Challan Identification Number (CIN) on this receipt is what you will enter when filing your ITR to claim credit for the advance tax paid. Your payment typically reflects in Form 26AS and the AIS within two to three working days.

Common error to avoid: Always select AY 2027-28 when paying advance tax for FY 2026-27. Selecting AY 2026-27 by mistake creates a mismatch that requires a correction application to resolve.

Advance Tax for Freelancers and Professionals Under 44ADA

Freelancers, consultants, and professionals (doctors, engineers, architects, interior designers) can opt for presumptive taxation under Section 44ADA if their gross professional receipts do not exceed ₹75 lakh in the year (with at least 95% of receipts received via banking channels). Under 44ADA, 50% of gross receipts is treated as net income — no separate expense records required.

The advance tax benefit under 44ADA is that all advance tax can be paid in a single instalment on or before 15 March 2027. No quarterly payments are needed, making tax planning significantly simpler for independent professionals who find it hard to estimate income quarter by quarter.

However, opting for 44ADA means you cannot claim business expense deductions above 50% of gross receipts. If your actual expenses exceed 50%, the regular taxation route with quarterly advance tax might result in lower overall tax — worth calculating both ways before deciding.

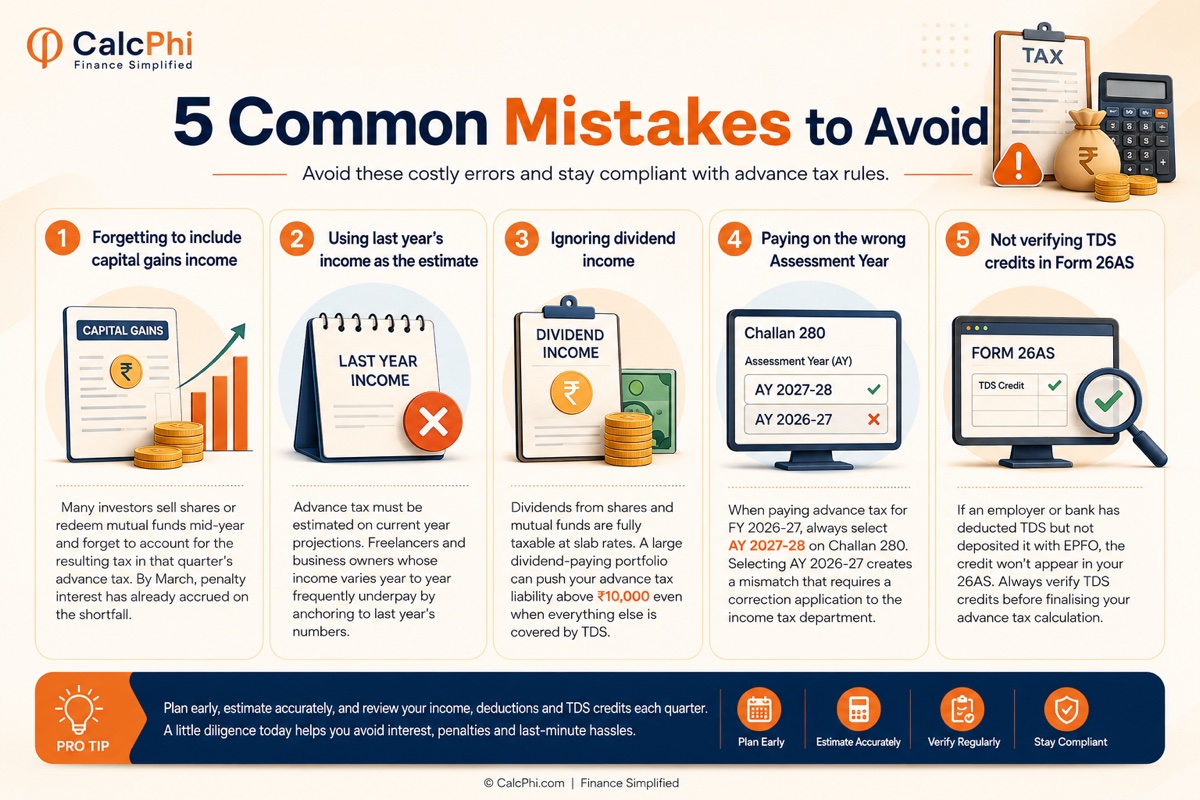

Common Mistakes to Avoid

Forgetting to include capital gains income: Many investors sell shares or redeem mutual funds mid-year and forget to account for the resulting tax in that quarter's advance tax. By March, penalty interest has already accrued on the shortfall.

Using last year's income as the estimate: Advance tax must be estimated on current year projections. Freelancers and business owners whose income varies year to year frequently underpay by anchoring to last year's numbers.

Ignoring dividend income: Dividends from shares and mutual funds are fully taxable at slab rates. A large dividend-paying portfolio can push your advance tax liability above ₹10,000 even when everything else is covered by TDS.

Paying on the wrong Assessment Year: When paying advance tax for FY 2026-27, always select AY 2027-28 on Challan 280. Selecting AY 2026-27 creates a mismatch that requires a correction application to the income tax department.

Not verifying TDS credits in Form 26AS: If an employer or bank has deducted TDS but not deposited it with EPFO, the credit won't appear in your 26AS. Always verify TDS credits before finalising your advance tax calculation.

Frequently Asked Questions

Does advance tax apply to me if I am salaried with a side income from freelancing?

Yes, it does. If your employer's TDS covers most of your salary tax but your freelance income creates an additional liability of more than ₹10,000, you must pay advance tax on that freelance income. Estimate your freelance earnings for the full year, calculate the tax on total income, subtract employer TDS, and if the balance exceeds ₹10,000, pay advance tax in the four instalments.

What happens if I do not pay advance tax and just pay everything when I file my ITR?

You will owe interest under Section 234B at 1% per month on the unpaid amount from April 1 to the date of payment. If you also missed quarterly instalments, Section 234C interest applies additionally. The combined interest on a ₹1.5 lakh shortfall paid in July — three months after March 31 — would be ₹4,500 under 234B alone. While not catastrophic, this is entirely avoidable with timely payments.

Is there any advance tax on salary income that has TDS deducted by the employer?

No. If your employer is correctly deducting TDS each month and that TDS covers more than 90% of your total tax liability, you do not owe advance tax on salary. The obligation only arises when TDS-covered tax falls short of 90% of the total liability — which typically happens when you have untaxed income outside salary like freelance earnings, capital gains, or rental income.

Can I revise my advance tax payment if my income estimate changes during the year?

Yes, and you should. Advance tax is based on estimated income, and estimates change. If your income in the second half of the year turns out to be significantly higher than you estimated in June, simply pay a higher amount in the December or March instalment. There is no formal revision process — just pay the correct cumulative amount by the relevant due date to avoid Section 234C interest.

How do I check how much advance tax I have already paid?

Log in to the Income Tax e-filing portal at incometax.gov.in, go to "My Account" and then "Tax Credit Statement (Form 26AS)," or check the Annual Information Statement (AIS). All advance tax payments made via Challan 280 reflecting your PAN will appear here, typically within two to three working days of payment.

Is advance tax applicable under both the old and new tax regimes?

Yes, the obligation to pay advance tax exists regardless of which regime you choose. What changes between regimes is the actual amount of advance tax you owe, because the two regimes calculate taxable income and tax differently. Calculate your liability under both regimes, choose the lower one, and base your advance tax instalments on that figure.

Disclaimer: The information in this article is for educational and estimation purposes only and does not constitute financial or tax advice. Tax laws are subject to change, and individual circumstances vary. All figures are based on publicly available data for FY 2026-27 (AY 2027-28). Please consult a qualified Chartered Accountant or tax advisor for personalised guidance on your advance tax obligations.