Catch-Up Super Contributions Australia: How to Use Your Unused Concessional Caps in 2026

Most Australians leave thousands of dollars in tax savings on the table every year — simply because they don't know the carry-forward concessional contribution rule exists. If your total super balance is under $500,000, you can stack up to five years of unused concessional caps and make one large, tax-deductible contribution in a single financial year. For some people, that's a legal tax deduction of $80,000, $100,000, or more — in a single year.

This guide explains exactly how catch-up super contributions work, who qualifies, how to check your available cap space, and which situations make this strategy most powerful. All figures are current for the 2025-26 and 2026-27 financial years.

What Are Concessional Contributions?

Before diving into the catch-up rule, it's worth understanding what "concessional" actually means. Concessional contributions are super contributions made from pre-tax money — meaning they attract a tax deduction. The three main types are:

- Employer Super Guarantee (SG) payments — currently 12% of your ordinary time earnings for 2025-26

- Salary sacrifice contributions

- Personal contributions for which you lodge a Notice of Intent to claim a tax deduction

When a concessional contribution enters your super fund, the fund pays 15% contributions tax on it. For most Australians on a marginal tax rate of 32.5% or higher, this is significantly cheaper than paying income tax on that money — which is why contributing more to super is often one of the most effective legal tax reduction strategies available.

The Annual Concessional Cap — and What Happens When You Don't Use It

The general concessional contributions cap for 2025-26 is $30,000. This applies to the combined total of all concessional contributions across all your super funds — your employer's SG payments count toward this limit too. From 1 July 2026, the cap rises to $32,500 due to indexation in line with average weekly ordinary time earnings (AWOTE), as confirmed by the ATO.

In previous years, any unused cap space simply disappeared at year-end. But since 1 July 2018, the ATO introduced the carry-forward rule: if you don't use your full concessional cap in a financial year, the unused portion rolls forward and can be used in a future year — for up to five years.

Here's a quick reference for historical caps that feed into your carry-forward pool:

- 2019-20 to 2020-21: $25,000 per year

- 2021-22 to 2023-24: $27,500 per year

- 2024-25 and 2025-26: $30,000 per year

- 2026-27 onwards: $32,500 per year (indexed)

If you contributed less than the cap in any of these years — and your super balance was under $500,000 at the relevant 30 June — that unused amount is still sitting there, waiting to be claimed.

Eligibility: Who Can Use Carry-Forward Contributions?

The rules are straightforward, but two conditions must both be met:

Your total superannuation balance (TSB) at 30 June of the previous financial year must be less than $500,000. The TSB includes accumulation and pension phase balances across every super fund you hold — not just your primary fund. You can check this figure in myGov linked to the ATO under Super → Information → Total super balance.

You must have unused concessional cap amounts from at least one of the five previous financial years. The ATO tracks this automatically. If you contributed less than the annual cap in any of those years, the unused amounts are banked under your tax file number.

One important nuance: even if your TSB tips above $500,000, your unused cap amounts don't disappear — they remain on record. If your balance later drops back below $500,000 at a future 30 June snapshot, you regain access to whatever unused amounts haven't yet expired.

Age consideration: If you are between 67 and 74 and want to claim a tax deduction on a personal concessional contribution, you must meet the work test — that is, be gainfully employed for at least 40 hours within a period of 30 consecutive days during the financial year. The work test does not apply to employer SG or salary sacrifice contributions.

Want to see exactly how much your super balance could grow if you make a large catch-up contribution now? Use CalcPhi's free Super Balance Calculator to model different contribution scenarios and see your projected balance at retirement.

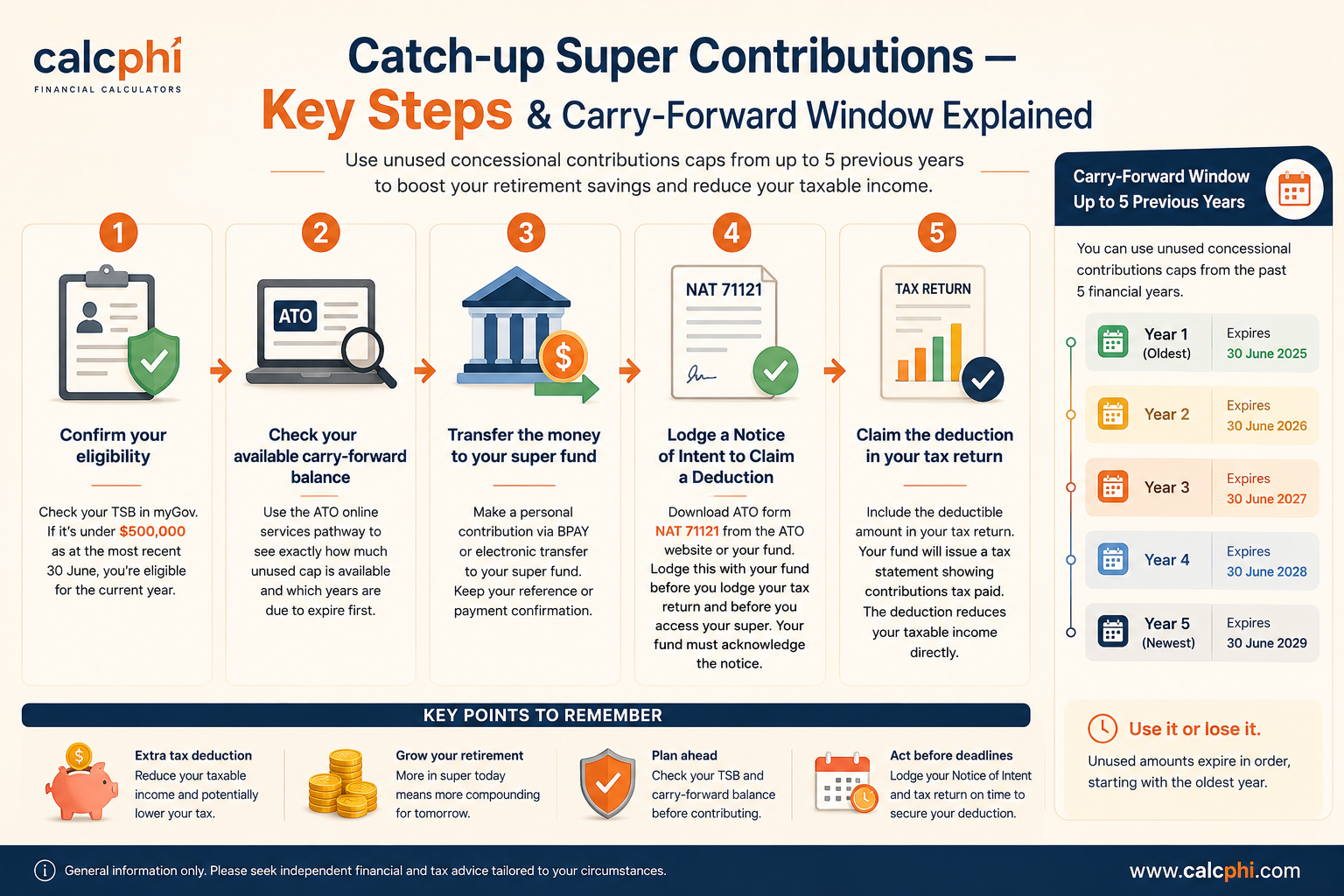

How the Five-Year Carry-Forward Window Works

The carry-forward rule operates on a strict rolling five-year basis. Unused cap amounts expire permanently after five years if not used. The ATO always applies the oldest available year's unused amount first — so when you exceed the current-year cap, it draws on 2020-21 before 2021-22, and so on.

This expiry rule matters enormously. Unused amounts from the 2020-21 financial year will expire at the end of 2025-26 if not used. After 30 June 2026, those amounts are gone permanently. If you've been accumulating carry-forward space since 2020 and haven't acted, this financial year is effectively your last chance to use the oldest slice of that pool.

| In financial year | Oldest available unused cap year | Oldest year expires |

|---|---|---|

| 2024-25 | 2019-20 | End of 2024-25 |

| 2025-26 | 2020-21 | End of 2025-26 |

| 2026-27 | 2021-22 | End of 2026-27 |

Worked Example: Returning from a Career Break

Consider Priya, 38, who took three years off work for parental leave and then worked part-time before returning to full-time employment at $120,000 per year. Her employer pays the 12% SG rate, meaning $14,400 in employer contributions annually. Her total super balance at 30 June 2025 was $295,000 — well under $500,000.

| Financial Year | Annual Cap | Total Contributed | Unused Cap |

|---|---|---|---|

| 2020-21 | $25,000 | $6,000 | $19,000 |

| 2021-22 | $27,500 | $8,000 | $19,500 |

| 2022-23 | $27,500 | $14,400 | $13,100 |

| 2023-24 | $27,500 | $14,400 | $13,100 |

| 2024-25 | $30,000 | $14,400 | $15,600 |

| Total carry-forward available | — | — | $80,300 |

In 2025-26, Priya can contribute up to $30,000 (current-year cap) + $80,300 (carry-forward) = $110,300 in concessional contributions. Her employer has already contributed $14,400, leaving $95,900 of room for personal concessional contributions.

She decides to contribute $70,000 as a personal deductible contribution, bringing her total concessional contributions for the year to $84,400 — safely within her extended cap.

Tax result: Priya's marginal rate is 32.5% (plus 2% Medicare levy). The fund pays 15% contributions tax on the $70,000 personal contribution ($10,500). Priya claims a $70,000 tax deduction, saving approximately $24,150 in income tax (34.5% effective rate on that income vs 15%). Net tax benefit: around $13,650 on the $70,000 personal contribution alone.

Her super also grows by $59,500 (the $70,000 minus 15% contributions tax) — compounding inside a low-tax environment for the next 25+ years.

How to Check Your Available Carry-Forward Amount

The ATO maintains real-time records of your unused concessional cap balances. Here's how to access them:

- Log in to myGov at my.gov.au

- Link your myGov account to the ATO (if not already linked)

- Navigate to: Super → Information → Carry-forward concessional contributions

- Your unused amounts are listed by financial year, including the year each portion expires

Note that the ATO's figures reflect contributions reported by your fund. Super funds don't always report in real time — allow two to three months after year-end for figures to fully update. If your SMSF annual return is outstanding, your carry-forward balance may appear incomplete until it's lodged and processed.

Making the Contribution: Step-by-Step

- Confirm your eligibility. Check your TSB in myGov. If it's under $500,000 as at the most recent 30 June, you're eligible for the current year.

- Check your available carry-forward balance. Use the ATO online services pathway described above to see exactly how much unused cap is available and which years are due to expire first.

- Transfer the money to your super fund. Make a personal contribution via BPAY or electronic transfer to your super fund. Keep your reference or payment confirmation.

- Lodge a Notice of Intent to Claim a Deduction. Download ATO form NAT 71121 from the ATO website or your fund. Lodge this with your fund before you lodge your tax return for that year and before you access your super. Your fund must acknowledge the notice.

- Claim the deduction in your tax return. Include the deductible amount in your tax return. Your fund will issue a tax statement showing contributions tax paid. The deduction reduces your taxable income directly.

To understand how salary sacrifice compares to a lump personal deductible contribution for your situation, try CalcPhi's Salary Sacrifice Calculator — it models the real after-tax impact of different contribution strategies.

Who Benefits Most From This Strategy?

Returning parents and career-breakers are typically the biggest beneficiaries. Years of reduced or zero employer contributions leave a large carry-forward balance ready to use as soon as income returns. A catch-up contribution in the year of return to full-time work can recover years of missed compounding almost immediately.

Business owners and contractors with uneven income have often had low-contribution years during lean periods. A strong revenue year is the ideal time to deploy accumulated carry-forward space and reduce taxable income significantly.

Pre-retirees aged 50–65 with super under $500,000 can use catch-up contributions to aggressively boost their super balance in the final working years, taking full advantage of compound growth before preservation age. For someone with $350,000 at 55 and a 10-year runway, an extra $80,000 catch-up contribution could add well over $130,000 to their retirement balance at 8% annual growth.

Workers who received a windfall — an inheritance, bonus, property sale, or redundancy payment — can use the carry-forward rule to shift a portion of that lump sum into super at a much lower effective tax rate, reducing the income tax impact in a high-income year.

Note on Division 293 tax: If your income plus concessional contributions exceeds $250,000, an additional 15% tax (known as Division 293) applies to the concessional contributions above that threshold — or the amount above $250,000, whichever is less. This doesn't eliminate the benefit of catch-up contributions, but it does reduce the tax arbitrage. At the 47% top marginal rate (45% + 2% Medicare), even with Division 293, concessional contributions still save you 17 cents per dollar compared to paying income tax. Use CalcPhi's Income Tax Calculator to model your total tax position before making a large concessional contribution.

Common Mistakes to Avoid

Contributing more than your available cap will trigger excess concessional contributions. The ATO will add the excess to your assessable income, tax it at your marginal rate (with a 15% tax offset for contributions tax already paid), and issue an excess concessional contributions determination. Always confirm your exact available space in myGov before contributing.

Forgetting to lodge the Notice of Intent before filing your tax return is the most costly procedural error. Without it, you cannot claim the deduction — and once your return is lodged, it's too late to retrospectively lodge the notice for that contribution. Set a calendar reminder.

Assuming the ATO figure is final before contributions are fully reported. In the first two to three months of a new financial year, previous-year figures may not yet reflect all your fund's reported contributions. Cross-check against your super fund statements before acting.

Model your catch-up contribution impact with CalcPhi's free Australian calculators:

Super Balance Calculator → Salary Sacrifice Calculator → Income Tax Calculator → Capital Gains Tax Calculator →Frequently Asked Questions

What is the maximum catch-up concessional contribution I can make in 2025-26?

The maximum is your current-year cap ($30,000 for 2025-26) plus all unused cap amounts from the previous five financial years that haven't yet expired, provided your total super balance at 30 June 2025 was under $500,000. Depending on your contribution history, the combined total could theoretically reach up to $142,500 (if you had minimal contributions since 2020-21) — though individual amounts vary. Check your actual available balance in myGov under ATO online services.

Does my employer's Super Guarantee count toward the carry-forward cap?

Yes. All concessional contributions — employer SG, salary sacrifice, and personal deductible contributions — count toward both the current-year cap and your carry-forward calculation. If your employer contributes $14,400 in SG for the year, that amount is deducted from your available concessional room for that year.

What happens if my super balance goes over $500,000 before I use my carry-forward?

Your unused cap amounts don't disappear — they stay on record. However, you cannot access them in any year where your TSB at the prior 30 June was $500,000 or more. If your balance drops back below $500,000 in a later year, you regain access to whatever unused amounts haven't yet expired (based on the five-year rolling window). Cap amounts that expire during this locked-out period are permanently lost.

Do I need to tell the ATO I want to use carry-forward, or does it happen automatically?

You don't need to notify the ATO separately. Once your total concessional contributions for the year exceed the standard annual cap, the ATO automatically applies your oldest available unused cap amounts. However, you do need to lodge a Notice of Intent with your super fund if you're making a personal contribution and want to claim a tax deduction — that step is not automatic.

Can I use catch-up super contributions to reduce capital gains tax in the same year?

Yes — and this is one of the most powerful applications. A large concessional contribution reduces your taxable income in the year it's claimed. Since capital gains are added to your taxable income (with the 50% discount for assets held over 12 months), a catch-up contribution can partially offset the tax impact of a major asset sale. Use CalcPhi's Capital Gains Tax Calculator to estimate your CGT liability first.

Is there an age limit for catch-up concessional contributions?

There is no upper age limit per se, but if you are between 67 and 74, you must satisfy the work test (gainfully employed for at least 40 hours in a 30-consecutive-day period during the financial year) to claim a tax deduction on personal contributions. Employer SG and salary sacrifice contributions do not require the work test. From age 75, you generally cannot make voluntary concessional contributions at all.

Disclaimer: The information in this article is for general educational purposes only and does not constitute financial or tax advice. Catch-up concessional contributions involve rules that depend on your individual super balance, contribution history, income, and tax circumstances. Always consult a qualified financial adviser or registered tax agent before making large super contributions. CalcPhi's calculators are estimation tools only — they do not replace personalised professional advice.