Australian Shares vs Property: Which Investment Wins Long-Term?

Australians are famously obsessed with property. At every barbecue, in every family WhatsApp group, and in every finance podcast, the question comes up: should I invest in shares or buy an investment property? It is one of the most debated personal finance topics in the country — and also one of the most misunderstood.

The honest answer is that neither asset class is universally superior. What determines which investment "wins" for you is a combination of how much capital you have, your tax situation, your appetite for risk, your need for income versus growth, and how hands-on you want to be. This article breaks down the real comparison: the data, the tax treatment, the leverage, the costs, the risks, and what the smartest Australian investors actually do.

Long-Term Performance: What 30 Years of Data Actually Shows

Starting with raw returns is the right place, but raw returns alone are deeply misleading.

The ASX 200 has delivered total returns (capital growth plus reinvested dividends) of approximately 9 to 10 percent per annum over the past three decades. Capital growth alone has averaged around 6 to 6.5 percent, with dividends adding another 4 to 4.5 percent — and that dividend figure rises to 5.5 to 6 percent when you factor in the value of franking credits.

Residential property in Australia has delivered national average capital growth of around 5.5 to 6.5 percent per annum over the same period. Sydney and Melbourne have outperformed that national average, with Sydney's median dwelling price growing at roughly 7 to 7.5 percent annually. Adding gross rental yields of 2.5 to 3.5 percent gives a total return in the range of 8 to 10 percent — broadly comparable to shares on a raw basis.

| Asset Class | Total Return (incl. income) | Capital Growth Only | Income Yield |

|---|---|---|---|

| ASX 200 (30-year average) | ~9–10% p.a. | ~6–6.5% p.a. | 4–4.5% (inc. franking) |

| Sydney residential (30-year) | ~8–10% p.a. | ~7–7.5% p.a. | 2.5–3.5% gross |

| Melbourne residential (30-year) | ~7.5–9% p.a. | ~6.5–7% p.a. | 2.5–3% gross |

| Australian residential (national avg) | ~7–8.5% p.a. | ~5.5–6.5% p.a. | 2.5–3.5% gross |

At the highest level, Australian property and Australian shares have delivered similar total returns over long periods. The difference lies not in the headline number but in how those returns are structured, taxed, levered, and accessed.

The Leverage Advantage: Why Property Feels Like It Wins

When you buy an investment property, you typically use a 20 percent deposit and borrow the remaining 80 percent at residential mortgage rates — approximately 6 to 6.5 percent per annum in 2026. This leverage dramatically amplifies your returns on the capital you actually contribute.

Consider this example: you invest a $200,000 deposit to purchase a $1,000,000 investment property. If that property grows at 7 percent in the first year, its value increases by $70,000. Your return on your actual $200,000 contribution is 35 percent — before accounting for rental income, negative gearing tax benefits, and the cost of interest payments.

The same leverage is theoretically available for shares through margin loans. But margin loan rates are materially higher than residential mortgage rates — typically 8 to 10 percent — and margin loans come with margin calls. If the market falls and your loan-to-value ratio breaches the lender's threshold, you may be forced to sell at exactly the wrong moment. Property loans do not have margin calls. You can hold a property through a 20 percent price correction without your bank forcing a sale, as long as you continue to service the mortgage.

This is why property has created so much wealth for Australian investors — not because property outperforms shares on a raw return basis, but because ordinary Australians can access large amounts of low-cost leverage against property in a way that is psychologically and structurally far more manageable than leveraged share investing.

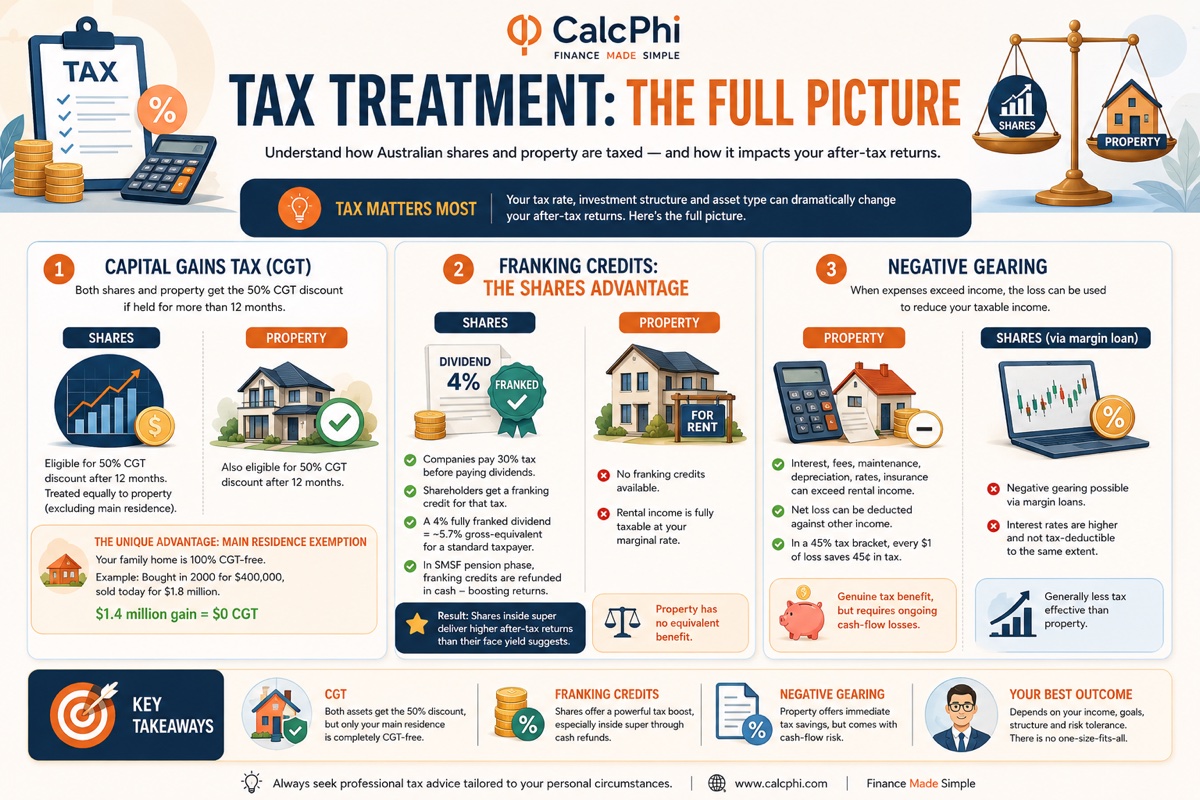

Tax Treatment: The Full Picture

Tax treatment is arguably the most important factor in determining which investment wins for a specific investor — and it varies enormously depending on your income, your structure, and the asset class.

Capital Gains Tax

Both Australian shares and investment property qualify for the 50 percent CGT discount if held for more than 12 months. So at the CGT level, both assets are treated equally. However, property has one unique concession that shares will never have: the main residence exemption. Your family home is entirely exempt from CGT — every dollar of growth in your primary residence is completely tax-free when you sell. A Sydney homeowner who bought a home in 2000 for $400,000 and sells it today for $1.8 million pays zero CGT on the $1.4 million gain. No other asset class in Australia offers this.

Franking Credits: The Shares Advantage

Australian listed companies pay company tax of 30 percent before distributing dividends. The ATO allows shareholders to claim a credit for that tax already paid — this is called a franking credit. A 4 percent fully franked dividend is worth approximately 5.7 percent gross-equivalent to a standard taxpayer. Inside a self-managed superannuation fund (SMSF) in pension phase, those franking credits are refunded in cash — meaning shares inside super generate a materially higher after-tax return than their face yield suggests. Property earns no franking credits; rental income is fully taxable at marginal rates.

Negative Gearing

When an investment property's expenses — interest, management fees, maintenance, depreciation, council rates, insurance — exceed its rental income, the resulting loss can be deducted against other income. For a high-income earner in the 45 percent marginal tax bracket, every dollar of net rental loss saves 45 cents in income tax. This is a genuine tax benefit — but it requires accepting ongoing cash-flow losses and betting on capital growth to compensate. Shares can be negatively geared through margin loans, but the interest rate differential makes this considerably less attractive.

The Cost Comparison Nobody Talks About Enough

Transaction costs are the silent killer of property investment returns, and most comparisons dramatically understate them.

When you buy an investment property in Australia, you face stamp duty (ranging from 3 to 5.5 percent of purchase price depending on the state, with no first home buyer concessions for investors), conveyancing fees, building and pest inspections, and mortgage establishment fees. On a $1,000,000 property purchase in New South Wales, stamp duty alone is approximately $40,000 to $42,000. Total acquisition costs commonly reach 5 to 6 percent of the purchase price before you have earned a single dollar of return.

When you sell, real estate agent commissions add another 2 to 3 percent of the sale price. These round-trip transaction costs — from purchase to sale — commonly total 8 to 10 percent of the property's value.

Shares, by contrast, can be bought and sold for 0.1 to 0.5 percent through a discount broker. Exchange-traded funds (ETFs) tracking the ASX 200 can be purchased for brokerage of $10 to $20 per trade. This means property requires a significantly longer holding period just to break even on transaction costs — an investor who buys and sells within five years is very likely to have underperformed a comparable share investment, even if headline capital growth was identical.

Cash Flow, Liquidity, and the Practical Reality

Australian residential property in major capital cities currently yields 2 to 3 percent gross on purchase price. After property management fees (7 to 10 percent of rent), council rates, water rates, insurance, maintenance, and mortgage interest at 6 to 6.5 percent, almost every investment property in Sydney and Melbourne is cash-flow negative. For a $1,000,000 property with an 80 percent mortgage, the net annual cash deficit can easily be $20,000 to $35,000 per year.

Shares provide far more flexible cash flow. A diversified ASX ETF yields 3.5 to 4.5 percent per year in dividends, paid directly to your bank account. You can reinvest automatically or take them as income — no maintenance bills, no difficult tenants, no emergency plumbing on a Saturday night.

The liquidity difference is equally stark. If you need $60,000 from your investment portfolio, you can sell exactly $60,000 worth of shares within seconds during market hours. From a property portfolio, your options are: sell the entire property (six to twelve weeks minimum), refinance (time and fees), or take out a personal loan. Property is inherently illiquid, and that illiquidity is a real and ongoing cost.

Superannuation: The Underrated Third Option

Any serious discussion of shares versus property in Australia must address superannuation. Inside super in accumulation phase, earnings are taxed at just 15 percent instead of your marginal rate. In pension phase (after age 60), all earnings are tax-free. The combination of concessional tax treatment and franking credit refunds makes ASX shares held inside super one of the most tax-efficient investments available to Australians.

Investment property cannot be held inside a retail super fund — only an SMSF can hold direct property, and SMSF property comes with strict rules: you cannot purchase from a related party, cannot live in it, and cannot use it personally in any way. For most Australians, super invested in diversified ASX-exposed index funds is a more tax-efficient vehicle than a personal brokerage account — the 15 percent earnings tax rate versus your marginal rate of 32.5, 37, or 45 percent makes a profound long-term difference.

Which Investor Profile Suits Which Asset?

Shares are likely better suited to your circumstances if you have a smaller amount of capital and cannot raise a 20 percent deposit on a viable investment property, you are investing inside superannuation, you want liquidity and cannot afford to lock capital up for 10-plus years, you are already heavily leveraged through a home mortgage, or you prefer diversification across sectors and geographies.

Investment property is likely better suited if you can comfortably raise a 20 percent deposit on a property with genuine rental demand, you have stable employment income to service a mortgage through market cycles, you are in a high marginal tax bracket where negative gearing deductions meaningfully reduce your tax bill, you are comfortable with the administrative reality of being a landlord, and you have a holding horizon of at least 10 years.

The most financially successful Australians typically end up holding both. A common structure is: a fully owned or near-paid-off primary residence (CGT-free main residence exemption), one or two investment properties (leveraged capital growth, negative gearing), and a diversified share portfolio inside super and individually (franking credits, liquidity, compounding returns). The question is not "either/or" — it is "in what proportion, and in what order, for my stage of life."

Frequently Asked Questions

Have Australian shares or property performed better over the last 20 years?

Over the 20 years to 2025, the performance comparison varies significantly by measurement period and city. Sydney and Melbourne property outperformed the ASX in pure capital growth terms from 2012 to 2017 — but the ASX has outperformed on total return (including reinvested dividends and franking credits) in most longer measurement windows. When leverage is applied to property and costs are excluded, property investors in major cities have often achieved superior equity returns — but that comparison is sensitive to entry and exit points, the interest rate environment, and whether negative gearing benefits are included.

Is negative gearing worth it in 2026?

Negative gearing remains a legal and genuine tax benefit in Australia in 2026. For a high-income earner in the 37 or 45 percent marginal tax bracket, the ability to deduct net rental losses against ordinary income creates a meaningful tax reduction. However, negative gearing should not be treated as an investment strategy in itself — you are still making a cash loss. It only makes sense if your capital growth expectation is strong enough to more than offset the ongoing cash outflows. In a flat or declining property market, negative gearing alone does not save you from a poor investment.

Can I use my superannuation to invest in property?

You can hold direct residential property inside a self-managed superannuation fund (SMSF), but the rules are strict. The property cannot be purchased from a related party, it cannot be used by any SMSF member or related party personally, and it must meet the "sole purpose test" of providing retirement benefits. SMSF property investing involves significant compliance obligations and costs. For most Australians not already operating an SMSF, investing in ASX shares or property ETFs inside a standard super fund is simpler and often more tax-efficient.

What is the minimum amount needed to start investing in shares versus property?

Shares have essentially no minimum — you can start investing in an ASX ETF with as little as $500 through most discount brokers. Property requires a deposit (typically 20 percent of the purchase price to avoid LMI), plus stamp duty, conveyancing, and inspection costs. In Sydney, that means $200,000 to $250,000 in cash to enter the investment property market for a median-priced dwelling. The low barrier to entry for shares makes them accessible to a much broader range of investors.

Do shares carry more risk than property?

Shares are more volatile in the short term — the ASX can fall 30 to 40 percent during a severe downturn (as in 2008–2009 and early 2020) and recover to new highs within a few years. Property falls are smaller in percentage terms but, because investors are typically highly leveraged, a 15 percent property price decline can wipe out 75 percent or more of the equity in an 80 percent LVR investment. Both asset classes carry meaningful risk; the nature and visibility of that risk differs. Property volatility is less visible because it is not priced daily on a screen.

Should I pay off my mortgage or invest in shares?

Mathematically, if the expected after-tax return on shares exceeds the after-tax interest rate on your mortgage, investing wins. With home loan rates at 6 to 6.5 percent and ASX historical returns at 9 to 10 percent annually, the mathematics slightly favours investing — but only if you can tolerate the short-term volatility of shares while making mortgage repayments simultaneously. For most people, a balanced approach — making minimum mortgage repayments, using an offset account to reduce interest, and investing surplus cash in a low-cost index fund — provides both wealth building and psychological security.

Disclaimer: The information in this article is intended for general educational purposes only. All figures, including historical returns, tax rates, and cost estimates, are based on publicly available data and are not tailored to individual circumstances. Past performance is not a reliable indicator of future performance. Nothing in this article constitutes financial advice. Australians should consult a qualified financial adviser, tax agent, or accountant before making any investment decision. CalcPhi's calculators are estimation tools only and do not replace professional financial guidance.

Written & verified by James O'Brien

Chartered Tax Adviser & CPA

James is a CPA and registered tax agent based in Melbourne with 14 years of experience in Australian tax law, CGT, PAYG withholding, and HECS-HELP repayment rules for salaried professionals and investors.